Warren Buffett stepped back from daily command at Berkshire Hathaway months ago. Yet his shadow stretches longer than ever across markets in mid-2026. The conglomerate’s cash reserves swelled to $397 billion in the first quarter, a figure that dwarfs many nations’ economies and signals deep caution from the team now led by Greg Abel. Short sentences hit hard here. This isn’t hesitation born of fear alone. It reflects decades of pattern recognition that few on Wall Street have matched.

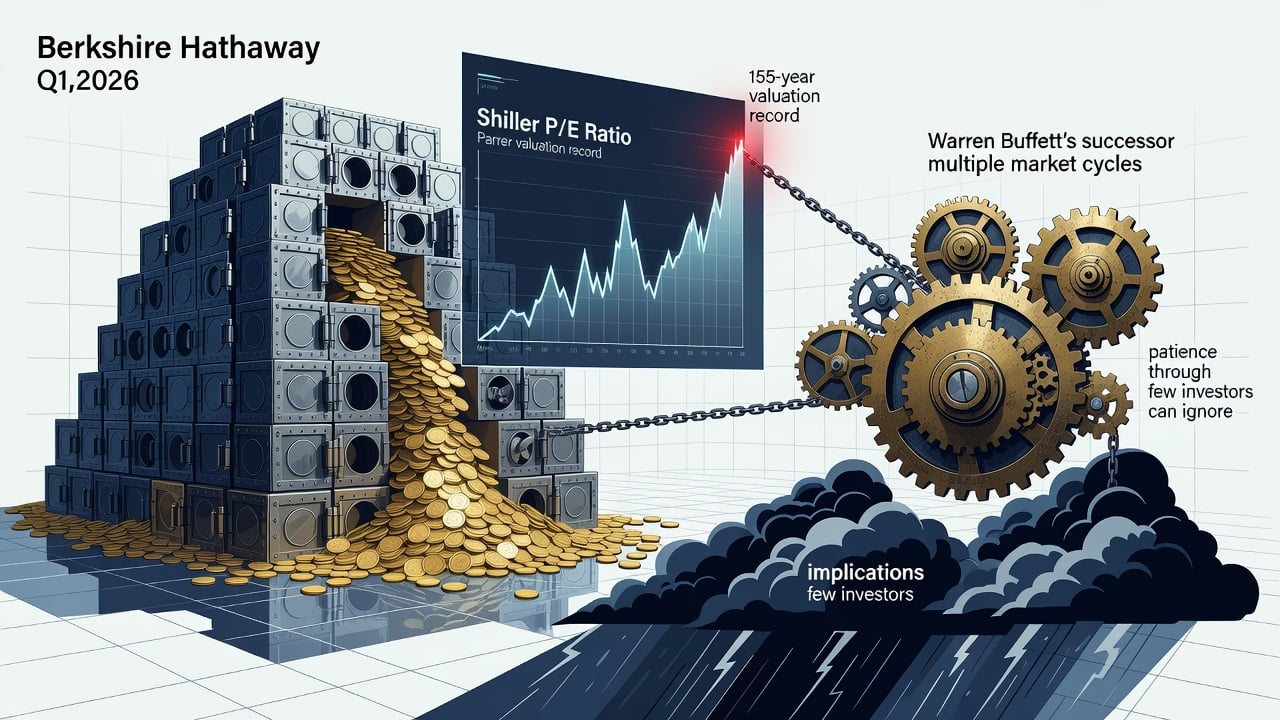

The S&P 500 has climbed to fresh highs this year, fueled by artificial intelligence optimism, aggressive corporate buybacks and better-than-expected profits. The Dow, the Nasdaq and the broad index all touched record closes in early June. Yet one valuation measure tied to 155 years of market history stands on the edge of breaking. A Motley Fool analysis lays out the stakes plainly. The Shiller price-to-earnings ratio, which smooths earnings over a decade to avoid recession distortions, hovers near levels last seen before major drawdowns. Should it eclipse prior peaks, history suggests painful consequences ahead.

Buffett never chased every trend. He built Berkshire from a failing textile mill into a fortress through insurance float, disciplined acquisitions and an aversion to overpaying. From 1965 through recent years that record produced compounded annual returns near 20 percent, crushing the S&P 500’s roughly 10 percent average. But the man himself has long warned that size becomes an anchor. Today Berkshire’s scale demands opportunities measured in tens of billions. Few appear at current prices.

And so the cash pile grows. It reached $397.4 billion by March 31, according to earnings reports covered by CNN and later confirmed in filings. That’s up from $373 billion at year-end 2025. Much of it sits in short-term Treasury bills yielding around 5 percent, generating roughly $17 billion in annual risk-free income. The hoard now represents nearly 32 percent of Berkshire’s total assets, the highest proportion on record. Observers note this isn’t idle money. It is dry powder accumulated through 14 straight quarters of net stock selling.

Recent portfolio moves tell their own story. Berkshire trimmed holdings in Apple and Bank of America before Buffett’s formal retirement on January 1, 2026. It exited smaller stakes including Amazon, Domino’s and UnitedHealth in the first quarter, reducing the equity portfolio from 40 names to 26 and shrinking its value to about $263 billion, per a Seeking Alpha review of the 13F filing. Top positions still cluster around Apple, American Express, Coca-Cola, Bank of America and Chevron. They account for roughly two-thirds of listed equities. Yet the message rings clear. At today’s multiples, few assets meet the threshold for permanent capital.

Insurance operations remain the engine. Float from policies written at GEICO, Berkshire’s crown jewel in auto coverage, and other units provides low-cost leverage. Underwriting discipline has produced profits rather than losses in most recent years, adding to the capital base instead of draining it. BNSF Railway and utility holdings deliver steady earnings less tied to market swings. These businesses generate the cash that Abel and his deputies can deploy when fear creates bargains. But those moments have been rare lately.

History offers uncomfortable parallels. The Shiller CAPE has preceded every notable S&P 500 decline over the past quarter-century when it reached current territory. Some pullbacks proved short. Others lasted years. The ratio’s construction, averaging ten years of real earnings, prevents temporary earnings collapses from distorting the picture. Its current reading suggests stocks price in growth rates that may prove optimistic once AI spending cycles mature or interest rates refuse to fall further. The original Yahoo Finance piece that prompted wider discussion highlighted the record’s durability across generations of investors. Breaking it would mark a shift whose full effects remain unknown.

Buffett’s own words from earlier this year still resonate. He described the 2026 market dip as minor compared with three 50-percent-plus drops he navigated at Berkshire since 1965. “This is nothing,” he said in an interview cited across multiple reports. The comment wasn’t bravado. It reflected lived experience through the 1970s bear market, the dot-com bust and the financial crisis. Each time Berkshire emerged stronger because it had liquidity when others scrambled.

Greg Abel faces different pressures. Sworn in as a U.S. citizen recently in a ceremonial moment at a baseball game, the new CEO has begun reshaping parts of the portfolio. CNBC reported that Abel dumped a slate of smaller stocks in the months after taking full operational control. Succession planning that once seemed theoretical now operates in real time. Buffett remains chairman. His annual letters and meeting appearances shaped culture for six decades. The question investors quietly debate is whether Berkshire’s edge survives without his singular temperament.

Yet the structure he designed may prove more durable than any individual. No stock splits on the Class A shares. Voting power stays concentrated to discourage short-term activism. Buybacks occur only when shares trade below intrinsic value, a policy that has retired shares opportunistically. In the first quarter Berkshire repurchased some of its own stock even as it let the cash balance climb. That tension captures the current environment. Opportunities exist but not at the scale or margin of safety the team demands.

Market participants watch the cash level as a contrary indicator. When it swells this large, future returns for the broad index have often moderated. A Motley Fool follow-up published this month noted the pile approached $400 billion and quoted Buffett downplaying the year’s volatility. The piece reinforced that Berkshire’s patience has paid off across multiple cycles. Critics sometimes call the approach old-fashioned. Results argue otherwise.

Corporate earnings growth, quantum computing breakthroughs and SpaceX-driven IPO enthusiasm have all lifted sentiment in 2026. Record share repurchases by S&P 500 companies added further fuel. Still, valuation expansion explains more of the gains than underlying profit acceleration in many sectors. The Shiller ratio accounts for that distinction. It stands as one of the few metrics with predictive power across eras because it normalizes for economic cycles.

Berkshire’s insurance float continues to expand. Premiums written have grown steadily. Claims paid out lag in good years, creating investable capital at negative cost. This advantage helped Buffett compound capital at rates that turned an initial stake worth tens of thousands into billions for long-term holders. Today’s $734,000 Class A share price reflects that compounding, though recent six-month performance has lagged the broader market by a few percentage points. Zacks Investment Research noted the Class B shares slipped nearly 3 percent over six months amid the cash buildup.

But don’t mistake temporary underperformance for weakness. The company’s diversified operations, from railroads to candy makers to power generation, provide ballast. Its balance sheet carries virtually no net debt relative to its fortress-like equity. That stability allowed Berkshire to deploy capital during the March 2020 crash when others sold in panic. Similar windows may open again. The cash signals preparation, not prediction.

Wall Street analysts remain divided. Some see the elevated Shiller reading as justification for caution. Others point to productivity gains from technology that could justify higher multiples for years. History has rhymed often enough to command respect. The last time valuations stretched this far, subsequent returns over the following decade proved disappointing. Berkshire’s approach has always prioritized avoidance of permanent capital loss over chasing near-term upside.

So the cash sits. It earns. It waits. And in the process it reinforces the very reputation that made Berkshire one of the few truly durable institutions on Wall Street. The 155-year record on valuations may fall. The lessons Buffett embedded in his company probably won’t. Markets will fluctuate. Opportunities will reappear. When they do, Berkshire intends to be ready. That readiness, built over six decades, remains its most formidable advantage.