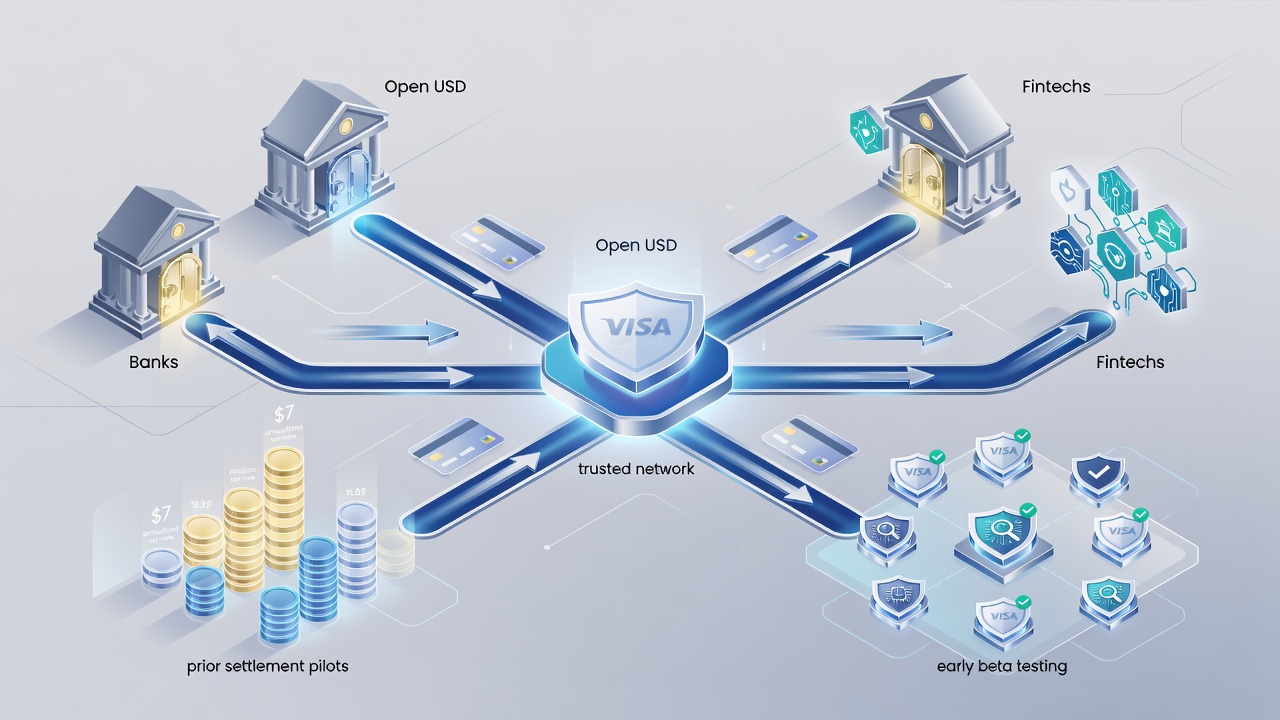

Visa just handed banks, fintech outfits and crypto firms a single dashboard to create, shift and control dollar-pegged tokens. The payments giant rolled out its Visa Stablecoin Platform on Wednesday, a managed service that bundles minting, wallet technology and compliance tools inside the same environment that already powers its global card network.

The launch arrives at a moment when stablecoin market value sits near $390 billion and regulators on both sides of the Atlantic tighten rules around digital assets. Yet institutions still face a tangle of separate vendors, security headaches and settlement delays. Visa aims to cut through that knot.

Jack Forestell, Visa’s chief product and strategy officer, put it plainly. “Stablecoins are opening up a new layer of programmable money, but for most institutions the hard part isn’t the concept, it’s the operational reality.” He added that the new platform gives clients “a single place to mint, move and manage stablecoin operations with the controls, security and network reach they already expect from Visa.”

Start with Open USD. The platform kicks off support for this freshly minted dollar token created by the Open Standard consortium, which counts Visa, Mastercard, Coinbase and more than 140 other firms among its backers. Yahoo Finance reported last month that the group wants Open USD to serve as a common rail for faster, cheaper cross-border payments and settlement.

Institutions using the Visa Stablecoin Platform can spin up tokens, burn them, hold balances, transfer funds and redeem for dollars. They gain access to Wallet-as-a-Service technology so they don’t have to build blockchain interfaces from scratch. Or they can plug in their own wallet systems. Bank-account linkages, approval workflows and transaction rules sit on top.

Security features feel familiar to any treasury chief. Dual-control approvals. Full audit logs. Passkeys instead of passwords. Allow lists that restrict transfers to approved addresses only. All of it runs inside Visa’s existing risk and fraud engines.

That last point matters. The new offering does not sit apart from Visa’s older stablecoin experiments. It talks directly to settlement services already live in the United States, to cards that spend stablecoin balances, and to cross-border rails that have moved billions of dollars in tokenized value. Early pilots showed promise. By March 2026 Visa reported an annualized run rate of roughly $7 billion across its stablecoin settlement flows, according to its own investor updates.

Go back further and the trajectory sharpens. In late 2025 Visa opened USDC settlement on Solana for U.S. issuers and acquirers. Initial partners included Cross River Bank and Lead Bank. The company expanded supported blockchains and tokens in the months that followed. Visa’s investor site noted the move cut settlement windows, allowed weekend transfers and lowered collateral needs.

Now the company pushes one step deeper. Instead of simply letting partners settle obligations in stablecoins, Visa lets them issue the coins themselves under tight controls. The difference sounds small. Operationally it proves enormous. Banks no longer need to stitch together a blockchain node, a custodian, a compliance engine and a banking partner. They flip a switch inside a Visa portal.

Beta testers get first crack. Visa invited a handful of clients to kick the tires. Feedback from those tests will shape the broader rollout. No hard date for full availability has surfaced. But the direction looks clear. The payments network wants stablecoins treated like any other funding source on its rails.

Competitors watch closely. Mastercard joined the same Open Standard group and runs its own stablecoin pilots. Traditional banks experiment with deposit tokens on private ledgers. Yet Visa’s reach gives it an edge few can match. Four hundred million merchants already accept its cards. Its fraud models process trillions in volume each year. That infrastructure now wraps around programmable money.

Regulatory tailwinds help too. Europe’s MiCA framework reaches full effect this month, forcing stablecoin issuers to meet strict reserve and transparency standards. In the U.S. lawmakers debate stablecoin legislation that could clarify which tokens qualify as payment instruments. Both developments lower perceived risk for the banks Visa courts.

Still, questions linger. Can the platform handle the compliance burden when a client wants to mint tokens for clients in twenty jurisdictions? How quickly will Visa add support for other major stablecoins such as USDC or Tether? The company declined to detail the roadmap beyond saying interoperability remains a priority.

Forestell’s quote reveals the bet. Interest in stablecoins already exists. The missing piece was plumbing that institutions trust. Visa believes it just installed that plumbing.

Shares of Visa traded near $362 Wednesday afternoon, little changed after the announcement. Investors have grown used to the company’s steady march into digital assets. The real test will come when the first bank announces a customer-facing product built on the new platform. That moment could arrive before year-end.

And the implications stretch beyond payments. Programmable money lets contracts auto-execute when conditions hit. Treasury teams can move funds across borders in seconds rather than days. Liquidity sits where it’s needed instead of trapped in correspondent accounts. If Visa’s platform delivers on those promises, the gap between traditional finance and blockchain narrows once more.

But delivery is everything. The history of fintech is littered with elegant demos that never scaled. Visa has scaled before. Its card network proved that a common set of rules and rails can turn fragmented markets into a global system. The company now applies the same logic to tokens that live on public blockchains.

Whether banks and fintechs embrace the offering will decide the next chapter. For now they have a new button to push. One that says mint. One that says move. One that says manage. All inside an environment they already know.