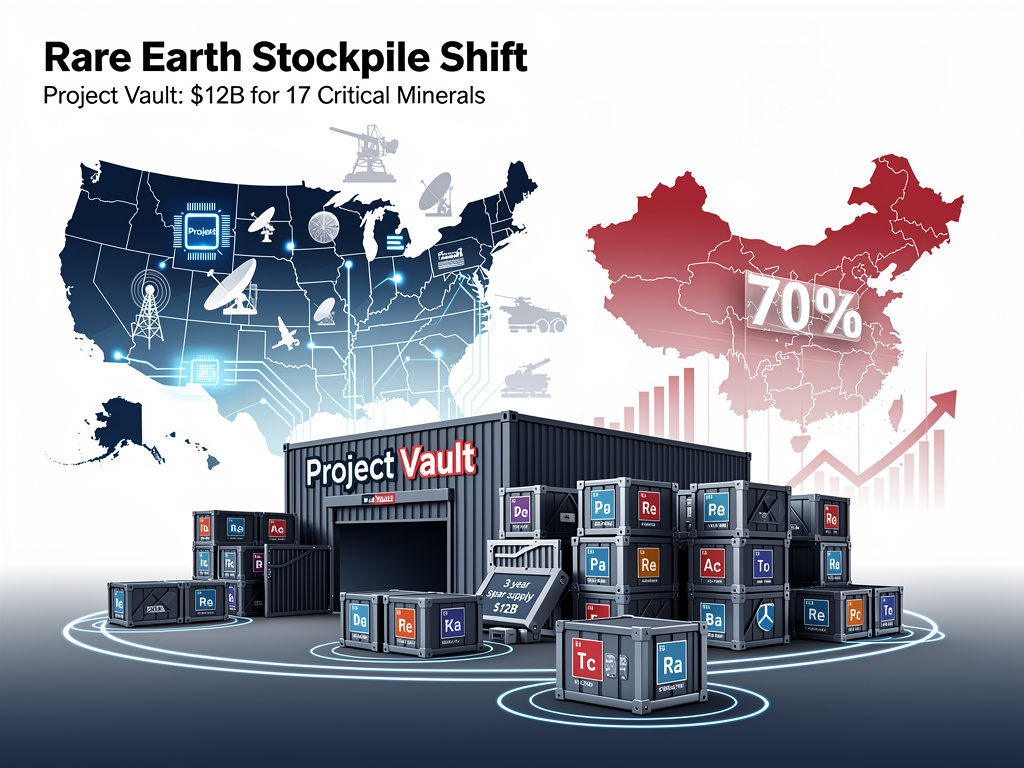

The Trump administration is preparing to launch an unprecedented $12 billion strategic initiative designed to fundamentally reshape America’s dependence on Chinese rare earth elements and critical minerals. Dubbed “Project Vault,” the ambitious stockpiling program represents the most significant federal intervention in mineral supply chains since World War II, signaling a dramatic escalation in the economic competition between Washington and Beijing.

According to the New York Post, the initiative will establish a massive national reserve of rare earth elements essential to everything from fighter jets and smartphones to electric vehicles and wind turbines. The program aims to secure a minimum three-year supply of 17 critical minerals, effectively insulating American manufacturers from potential supply disruptions orchestrated by Beijing, which currently controls approximately 70% of global rare earth production and 90% of processing capacity.

The strategic stockpile will focus on elements including neodymium, praseodymium, dysprosium, and terbium—materials that have become the sinews of modern technological civilization yet remain concentrated in Chinese hands. Industry analysts suggest the move could trigger a fundamental recalibration of global supply chains, potentially spurring billions in additional private investment in domestic mining and processing operations that have languished for decades under Chinese price competition.

A Decades-Long Vulnerability Finally Addressed

America’s rare earth dependency didn’t emerge overnight. The United States once dominated global production, with California’s Mountain Pass mine serving as the world’s primary source throughout the Cold War era. However, environmental concerns, regulatory costs, and aggressive Chinese pricing strategies gradually hollowed out the domestic industry. By the early 2000s, Beijing had effectively cornered the market, creating what defense strategists now characterize as a critical national security vulnerability.

The wake-up call came in 2010 when China temporarily restricted rare earth exports to Japan during a territorial dispute, sending prices skyrocketing and exposing the fragility of global supply chains. Despite repeated warnings from Pentagon officials and industry groups, successive administrations failed to mount a comprehensive response. The Trump administration’s Project Vault represents the first systematic attempt to address this strategic weakness, committing federal resources on a scale not seen since the Strategic Petroleum Reserve’s establishment in the 1970s.

Beyond Stockpiling: Catalyzing Domestic Production

While the $12 billion stockpile forms the initiative’s centerpiece, administration officials indicate Project Vault encompasses a broader strategy to revitalize American rare earth mining and processing. The program will reportedly include loan guarantees for domestic producers, streamlined permitting for new mining operations, and research funding for alternative extraction and recycling technologies. These complementary measures aim to address the chicken-and-egg problem that has plagued the industry: investors hesitate to fund new projects without guaranteed demand, while manufacturers resist shifting supply chains without reliable domestic sources.

Several American companies stand to benefit substantially from the initiative. MP Materials, which reopened the Mountain Pass mine in California, has been working to establish domestic processing capabilities that would allow it to produce finished rare earth magnets rather than shipping concentrates to China for refinement. Lynas Rare Earths, an Australian company with U.S. operations, has been developing a heavy rare earths separation facility in Texas. Energy Fuels has been extracting rare earths as byproducts from uranium processing. These firms have struggled with the economics of competing against subsidized Chinese production; federal stockpile purchases could provide the revenue stability needed to justify major capital investments.

The Processing Problem: America’s Achilles Heel

Mining rare earth ores represents only the first step in a complex, environmentally challenging process. Refining these minerals into usable forms requires sophisticated chemical processing that generates substantial waste streams, including radioactive materials. China’s willingness to accept the environmental costs of processing—coupled with decades of accumulated expertise—has made it nearly impossible for Western facilities to compete on cost. Even mines operating on American soil typically ship their concentrates to China for processing, negating much of the security benefit.

Project Vault’s architects recognize that true supply chain independence requires domestic processing capacity, not merely domestic mining. The initiative reportedly includes specific provisions to incentivize construction of separation and refining facilities, potentially through purchase guarantees for domestically processed materials at premium prices. This approach mirrors strategies employed by the Defense Production Act, which has historically been used to ensure domestic capacity for materials deemed essential to national security. The challenge lies in structuring incentives that attract private capital while avoiding the creation of permanently subsidized industries unable to compete without government support.

Geopolitical Ramifications and Chinese Countermoves

Beijing has already demonstrated its willingness to weaponize rare earth dominance. In 2019, amid escalating trade tensions, Chinese state media explicitly threatened to cut off rare earth supplies to the United States, noting that American F-35 fighters require approximately 920 pounds of rare earth materials per aircraft. More recently, China has imposed export controls on rare earth processing technologies and has been consolidating its industry under state control, suggesting preparations for potential supply restrictions.

Project Vault will likely prompt Chinese retaliation, potentially including accelerated restrictions on rare earth exports or processing services. However, administration officials appear to be calculating that short-term disruptions represent an acceptable cost for long-term security. The stockpile itself provides a buffer during the transition period, while domestic production ramps up. Some analysts suggest China may actually accelerate restrictions in response to Project Vault, paradoxically validating the initiative’s necessity while creating immediate market disruptions that could benefit early-stage American producers.

Environmental and Regulatory Hurdles

The rare earth industry’s environmental record presents significant obstacles to rapid domestic expansion. Rare earth mining and processing generate radioactive waste, acid mine drainage, and toxic chemical byproducts. The Mountain Pass mine’s previous closure resulted partly from environmental violations, and communities near proposed new facilities have mounted fierce opposition. Streamlining permitting processes, as Project Vault reportedly intends, will likely trigger legal challenges from environmental groups concerned about weakened protections.

Balancing national security imperatives against environmental stewardship represents one of the initiative’s central tensions. Modern processing technologies can significantly reduce environmental impacts compared to legacy methods, but they require substantial capital investment and still generate waste requiring long-term management. Some advocates argue that transparent, regulated domestic production under American environmental standards represents a more responsible approach than continuing to outsource environmental damage to China, where oversight remains opaque. This argument may prove crucial in navigating the regulatory and political challenges ahead.

Economic Implications for Defense and Technology Sectors

The defense industry has been particularly vocal about rare earth vulnerabilities. Modern weapon systems rely heavily on rare earth permanent magnets for precision-guided munitions, radar systems, and electric motors. The F-35 program alone has faced concerns about supply chain security, with some components requiring Chinese-processed materials. Project Vault’s establishment of a secure supply could accelerate defense procurement programs that have faced delays due to material sourcing concerns.

The technology sector faces similar dependencies. Rare earth elements are essential for smartphone speakers and vibration motors, computer hard drives, and display screens. The renewable energy transition has intensified demand, with wind turbines requiring up to 600 pounds of rare earth permanent magnets per megawatt of capacity, and electric vehicle motors relying on neodymium-based magnets for efficiency. A secure domestic supply could provide American manufacturers with competitive advantages while reducing exposure to geopolitically motivated supply disruptions.

International Partnerships and Allied Coordination

Project Vault exists within a broader international context of efforts to diversify rare earth supply chains away from Chinese dominance. The United States has been coordinating with allies including Australia, Canada, and Japan to develop alternative supply networks. Australia possesses significant rare earth deposits and has been developing processing capabilities, while Canada has been advancing several mining projects. Japan, having experienced Chinese supply restrictions firsthand, has been investing heavily in rare earth recycling technologies and alternative sources.

The initiative may include provisions for allied participation in the strategic stockpile, potentially through bilateral agreements that allow friendly nations to access reserves during emergencies in exchange for contributing to supply diversification efforts. Such arrangements would parallel existing strategic petroleum reserve sharing agreements among International Energy Agency members. Coordinated stockpiling and production incentives across allied nations could create sufficient scale to challenge Chinese market dominance more effectively than any single country acting alone.

Technological Innovation and Alternative Materials

While Project Vault focuses on securing traditional rare earth supplies, parallel efforts aim to reduce dependence through technological innovation. Researchers have been developing alternative magnet technologies that reduce or eliminate rare earth requirements, including iron nitride magnets and manganese-based compounds. Recycling technologies that recover rare earths from electronic waste represent another promising avenue, potentially providing a significant domestic source of materials from discarded devices.

The initiative reportedly includes research funding for these alternative approaches, recognizing that the ultimate solution to rare earth dependency may involve reducing demand rather than merely diversifying supply. However, developing and commercializing alternative technologies requires years of research and capital investment. The stockpile provides breathing room for these longer-term solutions to mature while ensuring immediate supply security. Some industry observers suggest that Chinese awareness of advancing alternatives may actually moderate Beijing’s willingness to restrict exports, as overly aggressive tactics could accelerate the development of technologies that permanently erode China’s market position.

Market Dynamics and Price Implications

Project Vault’s $12 billion commitment represents a substantial new source of demand that will inevitably affect rare earth markets. Prices for key elements have been volatile, with neodymium oxide fluctuating between $40 and $140 per kilogram over the past decade depending on Chinese production decisions and global demand cycles. Large-scale government purchases could stabilize prices at levels sufficient to justify new production investments, though critics warn of potential market distortions if government buying creates artificial price floors.

The initiative’s structure will prove crucial in determining market impacts. If purchases occur through competitive bidding processes that include both domestic and international suppliers, price effects may be modest. However, if preferences or premiums favor American producers, global market dynamics could shift substantially, potentially prompting other nations to implement similar nationalist policies. Some analysts predict a bifurcation of rare earth markets, with a premium-priced Western supply chain serving allied nations and a separate Chinese-dominated system serving other markets, similar to patterns emerging in semiconductor manufacturing.

Implementation Challenges and Timeline Uncertainties

Translating Project Vault from announcement to operational reality will require overcoming substantial logistical and bureaucratic obstacles. Establishing secure storage facilities for rare earth materials, which can oxidize or degrade if improperly stored, requires specialized infrastructure. Determining optimal stockpile compositions that balance current needs against future demand shifts presents complex forecasting challenges. Developing acquisition strategies that achieve value for taxpayers while incentivizing domestic production requires sophisticated program design.

The timeline for achieving meaningful supply chain independence extends well beyond typical political cycles, creating risks that future administrations might deprioritize or defund the initiative before it achieves its objectives. Rare earth mines require five to ten years from discovery to production, while processing facilities demand similar development periods. This extended timeline necessitates sustained political commitment and funding across multiple administrations—a challenge in America’s polarized political environment. The initiative’s ultimate success may depend as much on maintaining bipartisan support as on technical and economic factors.

The Road Ahead for American Mineral Independence

Project Vault represents a watershed moment in American industrial policy, marking a decisive shift from market-based approaches to strategic government intervention in critical supply chains. Whether the initiative succeeds in fundamentally reshaping rare earth markets or becomes another well-intentioned program that fails to achieve transformative results will depend on execution quality, sustained funding, and the ability to navigate environmental, regulatory, and political obstacles. Early indicators suggest the administration recognizes the magnitude of the challenge and has committed resources commensurate with the task.

The broader implications extend beyond rare earths to questions about America’s industrial strategy in an era of great power competition. If Project Vault succeeds in revitalizing a critical industry hollowed out by decades of globalization, it could serve as a template for addressing vulnerabilities in other strategic sectors from pharmaceuticals to advanced semiconductors. Conversely, if the initiative stumbles, it may reinforce skepticism about government’s ability to effectively direct industrial development, potentially constraining future efforts to address supply chain vulnerabilities. The stakes extend well beyond the $12 billion price tag, encompassing fundamental questions about economic security in an increasingly fractured global economy.