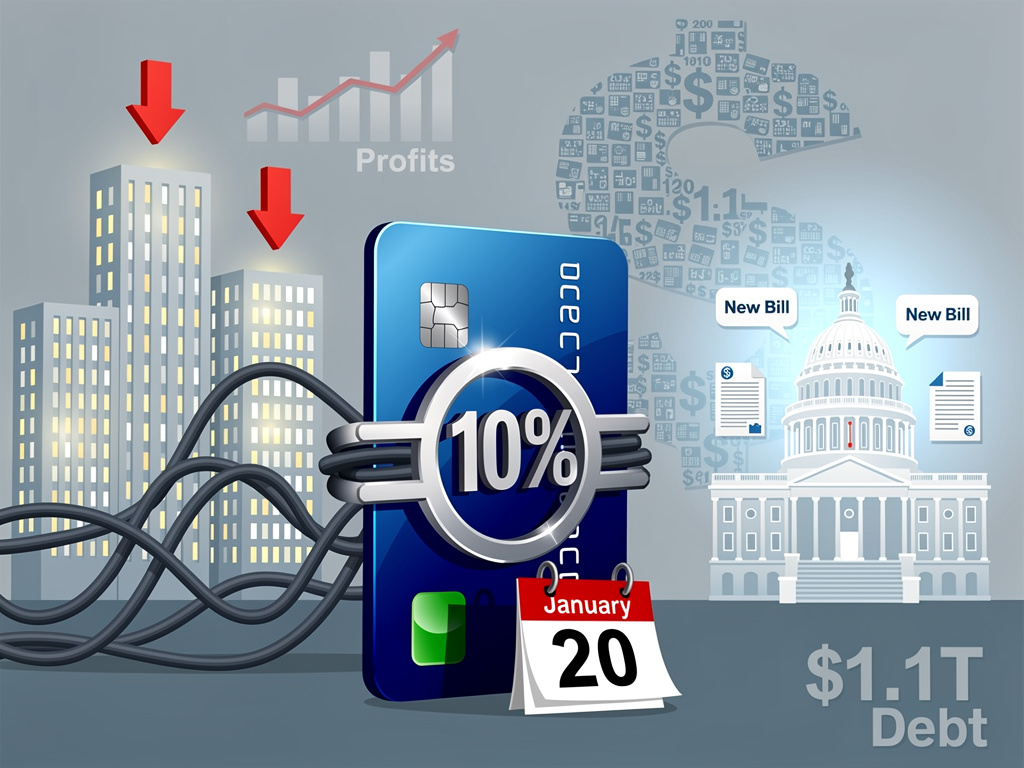

President Donald Trump ignited fresh debate over consumer debt on Friday by demanding a one-year cap on credit card interest rates at 10%, effective January 20, 2026. In a Truth Social post, he declared the American public has been ‘ripped off’ by rates of 20% to 30% that ‘festered unimpeded during the Sleepy Joe Biden Administration.’ The move revives a campaign promise aimed at easing affordability pressures amid record household debt levels.

Banking industry leaders swiftly pushed back, warning that such a cap could shrink credit access for millions of everyday Americans. Advocacy groups argue it would force issuers to tighten lending standards, favoring only high-income borrowers with pristine credit histories. Trump’s announcement coincides with the one-year anniversary of his administration’s start, framing it as a bold affordability initiative.

Reviving a Campaign Pledge

Trump first floated the idea during a September 2024 rally at Nassau Coliseum, telling supporters, ‘While working Americans catch up, we’re going to put a temporary cap on credit card interest rates.’ Average rates hit a record 21.76% in August 2024, per Federal Reserve data, before easing slightly to 20.97% by November 2025 under market pressures (New York Post).

The proposal echoes bipartisan efforts in Congress. Sens. Josh Hawley (R-Mo.) and Bernie Sanders (I-Vt.) introduced a bill last year for a five-year 10% cap, which stalled in committee. Hawley reacted enthusiastically on X, posting, ‘Fantastic idea. Can’t wait to vote for this,’ signaling potential legislative momentum (X post by Josh Hawley).

Industry Warnings Mount

Banking groups like the American Bankers Association have long opposed rate caps, contending they distort markets and reduce credit availability. ‘A cap would reduce credit availability,’ a Reuters report noted, citing industry advocates who predict issuers would ration cards to low-risk customers only (Reuters).

The Consumer Financial Protection Bureau’s past analyses support this view: usury caps historically lead to 20-30% drops in revolving credit for subprime borrowers. With U.S. credit card debt surpassing $1.1 trillion in late 2025, per recent Fed figures, the stakes are high for issuers reliant on interest income, which accounts for over 60% of major banks’ card revenues.

Bipartisan Momentum Builds

Sanders has championed the cause, stating in February 2025, ‘Trump pledged to cap credit card interest rates at 10%. Today, I introduced legislation with Sen. Hawley to do just that.’ Their bill highlighted how rates doubled in recent years, with $105 billion in interest charged in 2022 alone (X post by Sen. Bernie Sanders).

Hawley echoed the sentiment earlier, noting in November 2024, ‘Average credit card interest rates are near 30%. It’s a total ripoff. Congress should cap them’ (X post by Josh Hawley). Posts on X from both senators show growing public support, with Hawley’s updates garnering millions of views.

Market Reactions and Risks

Financial markets showed muted response on Monday, but bank stocks like Capital One and Discover dipped 2-3% in premarket trading. Analysts at JPMorgan warned clients that a cap could slash industry profits by $20-30 billion annually, prompting issuers to hike fees or cut rewards programs (CNN Business).

Elizabeth Warren praised the idea on X, while billionaire Bill Ackman offered mixed views, cautioning against unintended credit contraction. U.S. banking groups decried it as ‘price controls’ that punish responsible lenders (LiveMint).

Historical Precedents and Data Dive

Rate caps have varied success globally. In the U.S., 18 states impose limits below 36%, but federal efforts like the 2009 CARD Act focused on transparency rather than ceilings. Trump’s one-year limit aims for temporary relief, potentially saving consumers $50 billion in interest, based on current balances and rate differentials.

Fed data reveals subprime borrowers face rates above 28%, versus 12-15% for prime customers. A 10% cap could boost delinquency rates if issuers exit the market, mirroring effects seen in 1980s state caps that halved credit supply (The New York Times).

Legislative Path Forward

Trump lacks unilateral authority; implementation requires congressional action or regulatory pressure via the CFPB. Hawley and Sanders’ framework provides a blueprint, but Republican leadership must weigh party divisions—free-market allies like Senate Banking Chair Tim Scott have voiced skepticism.

Politico reports Trump specified the cap starts January 20, pressuring issuers voluntarily but eyeing executive orders to enforce compliance (Politico). Bipartisan appeal could fast-track it amid midterm pressures.

Issuer Strategies Emerge

Major players like Visa, Mastercard, and issuers such as Chase and Citi are lobbying intensely. CBS News notes ‘pushback from card issuers’ who favor alternatives like fee reforms Trump previously nixed (CBS News). Some propose voluntary reductions for good-standing customers.

Insiders predict a hybrid: caps for existing balances, with new credit at market rates. The Hill frames it as Trump’s bid to tackle high living costs, potentially reshaping $1.13 trillion in outstanding debt (The Hill).

Consumer Impact Projections

For a $10,000 balance at 21% versus 10%, monthly interest drops from $175 to $83, freeing $1,100 yearly per household. With 45% of Americans carrying balances, aggregate savings could hit $40 billion, per CardHub estimates. Yet, experts warn of backlash: reduced approvals could spike payday lending usage.

Business Insider highlights Trump’s phrasing as a direct call to companies, not law, testing industry goodwill (Business Insider). Long-term, it challenges the post-Dodd-Frank model where deregulation fueled rate surges.