German engineering once defined reliability and prestige on roads worldwide. BMW, Mercedes-Benz and Volkswagen built empires on that reputation. Their vehicles carried premium prices and even higher margins. Entire regions in Germany rose around their factories. Pension funds across Europe and the United States held their shares as ballast.

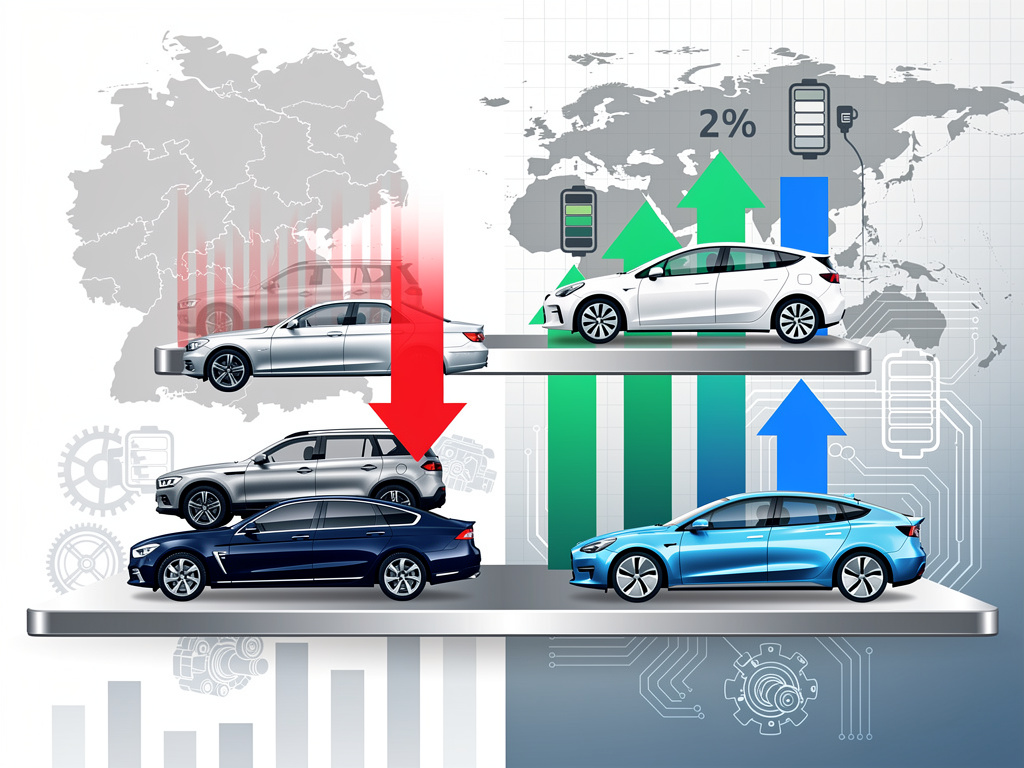

That era is slipping away. A single data point from the first quarter of 2026 captures the shift with brutal clarity. Global revenue among major automakers climbed 2 percent. German producers posted a 4 percent drop. The six-point spread reveals more than a bad quarter. It shows a structural reversal.

Reuters first reported the figures from an EY analysis released June 5. Japanese and American manufacturers drove the overall gain. German names moved in the opposite direction. Only one major car-producing bloc went backward while the industry advanced.

The decline did not arrive without warning. Chinese competitors such as BYD surged ahead in electric vehicles with lower prices, longer ranges and quicker charging times. U.S. tariffs under President Donald Trump added fresh pain for exporters already stretched thin. The costly and uneven switch to battery power compounded the pressure. Billions poured into new technology produced slower returns than expected.

Constantin Gall, an EY sector specialist, described the situation in stark terms. “The entire German automotive industry is undergoing a profound structural transformation,” he told Reuters. He pointed to lost sales in the United States and China, expensive overcapacity, heavy spending on software and the sluggish adoption of electric models. Then he delivered a blunt forecast. “2026 will be another crisis year for the automotive industry.”

And the Iran crisis adds another layer. Higher fuel prices and rising inflation threaten to weaken demand across Europe. German carmakers, already facing headwinds, can expect the slide to continue.

Investors have taken notice. Shares of the big three have lagged broader market gains for years. The “made in Germany” label still carries weight in certain segments. Yet its power to command loyalty and premium pricing has eroded. Regions built on auto employment now confront slower growth and potential job losses.

This reversal carries implications far beyond boardrooms in Munich, Stuttgart and Wolfsburg. The auto sector anchors the German economy. It supports hundreds of thousands of jobs directly and millions more in the supply chain. When these companies falter, the effects ripple through suppliers, logistics firms and local communities. Pension portfolios that counted on steady dividends must adjust.

Compare the current moment to past cycles. German brands once set standards that others chased. They dominated luxury segments and held strong positions in volume markets. China represented the great growth story. Sales there powered expansion for more than a decade. Now that same market has become a threat as domestic producers scale rapidly and capture share at home and abroad.

Tariffs complicate the picture further. The U.S. market remains critical for German luxury exports. New duties raise costs and reduce competitiveness against locally built alternatives. Executives have voiced concerns in recent months. BMW’s leadership offered particularly direct comments on the tariff threat, according to reports tied to the Yahoo Finance coverage of the EY study.

The pivot to electric vehicles has proven especially expensive. German firms invested heavily in battery technology, new platforms and the software that differentiates modern cars. Results have lagged. Competitors from Asia moved faster and cheaper. Sales of battery models in Europe have softened in some periods, adding to overcapacity at plants designed for traditional engines.

Industry watchers see no quick fix. The EY outlook suggests the revenue gap could persist. Structural changes take time. Reshaping product lines, renegotiating supply contracts and rebuilding brand appeal in a crowded electric segment will stretch across multiple years.

Some analysts draw parallels to other mature industries that faced sudden competitive shocks. The difference here lies in the speed. Chinese EV makers did not simply copy designs. They innovated on cost and technology in ways that caught established players off guard. Add geopolitical tensions and regulatory pushes for emissions cuts, and the challenges multiply.

Yet not every signal points downward. Certain German models retain strong resale values. Engineering expertise in areas like autonomous systems and premium interiors still matters. Partnerships with technology firms could accelerate software development. The question is whether these advantages can offset the current revenue slide before deeper damage sets in.

Portfolio managers who hold international equity funds have already felt the impact. German auto stocks once provided ballast during volatility. Their recent performance has made them a source of drag instead. Funds that once allocated significant weight to the sector now debate how much exposure to maintain.

The six-point gap from the first quarter offers a clear metric. It quantifies the trouble in language investors understand. Revenue contraction while peers expand signals lost momentum. It raises questions about future cash flows, dividend sustainability and the ability to fund necessary investments.

Broader market context adds perspective. While U.S. technology giants dominate headlines with artificial intelligence gains, traditional manufacturers face different pressures. The auto sector’s troubles highlight how uneven the global recovery remains. Some regions and industries advance. Others struggle to adapt to new realities around energy, trade and consumer preferences.

German officials and industry leaders have called for policy support. Faster permitting for factories, incentives for battery production and measures to ease the transition appear on wish lists. Whether governments can deliver in time remains uncertain. Political debates over budgets and green targets create additional friction.

In the meantime, the big three continue their balancing act. They cut costs where possible. They accelerate select electric launches. They defend margins in segments where they still lead. Progress is incremental. The EY numbers suggest it has not been enough to reverse the trend.

History offers mixed lessons. Industries rarely regain dominance once they lose it to nimbler rivals. But adaptation has happened before. The German carmakers bet that precision, quality and innovation can still carry the day. The coming quarters will test that conviction. The six-point gap is not just one number. It is an early indicator of how steep the climb back may be.