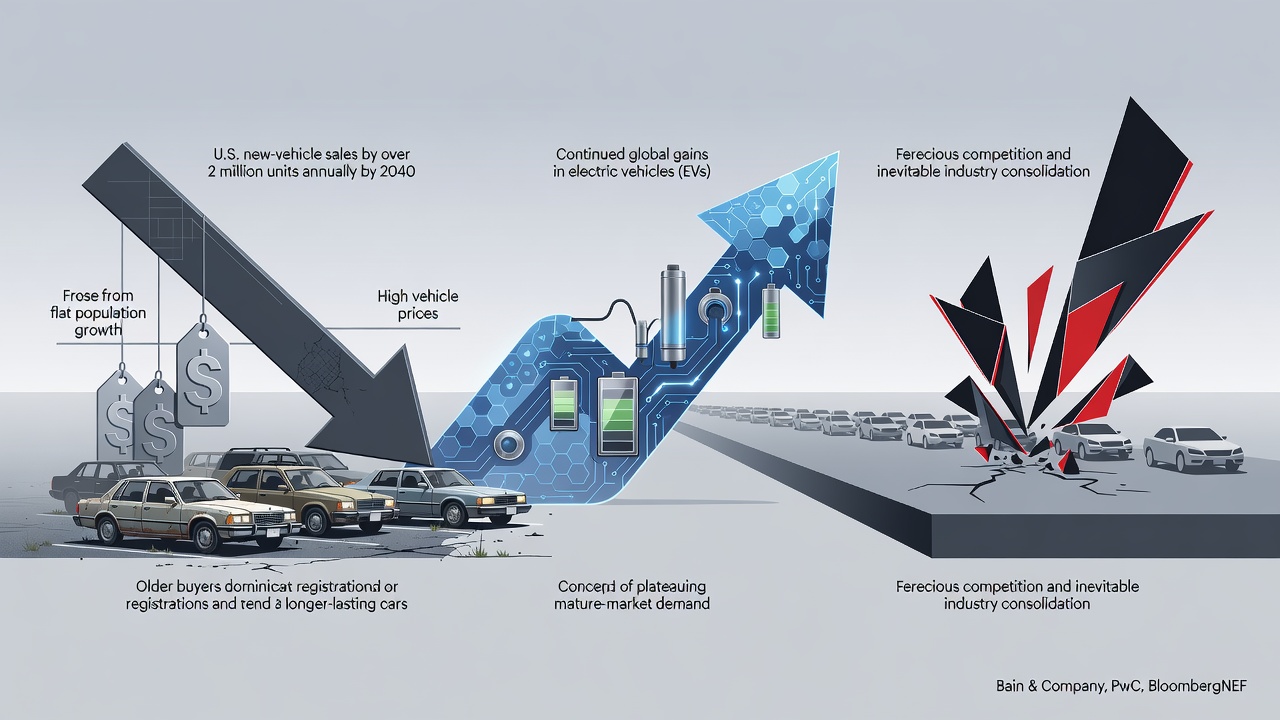

Mark Gottfredson saw the signs years ago. Now the Bain & Company partner watches them converge with striking speed. Falling birth rates. Soaring vehicle prices. Younger drivers who skip licenses altogether. The result? A U.S. car market that must contract sharply over the next decade and a half. Sales could fall by more than two million units annually by 2040. The industry that once counted on steady expansion now confronts a perfect storm of structural limits.

Gottfredson laid it out plainly in a recent CNBC report. “It is the perfect storm,” he said. “You’re a declining industry at a time when the technology is disrupting everything.” His revised forecast points to new-vehicle sales dipping below 14 million sometime after 2030. That marks a steep slide from the 2016 peak of 17.6 million. Earlier projections had pinned the drop on 2030 itself. Slower-than-expected progress on autonomous vehicles pushed the timeline out. The direction stays the same.

Demographics form the foundation of this shift. The U.S. fertility rate sits at 1.6 births per woman. Replacement level is 2.1. Immigration has been cut roughly in half from historical net migration levels. Population growth that once averaged 1 percent per year now hovers near flat. The auto sector matured in an era of reliable expansion. Those days are gone. Fewer people means fewer households needing cars. Simple as that.

Behavior compounds the numbers. Only half of today’s 16-year-olds hold a driver’s license. The figure stood near 70 percent from 1966 through 1984. Most still get licensed by age 25. Yet the delay signals deeper change. Ride-hailing services. Urban living. Different priorities. AutoForecast Solutions expects sales to remain flat around 16 million through 2033. “When you look into the future, younger people are more likely to use Uber or Lyft when they’re going somewhere,” the firm told CNBC.

Expense erects another barrier. New cars average around $50,000. No models sell below $20,000 anymore. Monthly payments jumped 30 percent over four years. One in five now exceeds $1,000. These figures come straight from Bain’s analysis and supporting data in the CNBC piece. Buyers feel the pinch. Many simply walk away. A Wall Street Journal report last month, referenced in Gizmodo coverage, combined projections from Ford, GM, Toyota and others. It identified roughly one million potential new-car buyers who have vanished from the U.S. economy. They are unlikely to return.

Those who do buy skew older. Consumers aged 55 and above account for nearly half of new-car registrations. They have for eight straight quarters. The 18-to-34 cohort represented 12 percent of registrations in 2021. That share fell below 10 percent last year. Automakers respond by designing for retirees. Features. Styling. Marketing. The preferences of younger buyers receive less attention. The cycle reinforces itself.

Vehicles themselves last longer. Average age on the road has climbed. The annual deregistration rate — cars taken off the road permanently — stood at 6 percent in 2000. It dropped to 5 percent in 2025. Bain sees it falling to 4.4 percent by 2040. Cars now average 12.8 years before they exit the fleet. Owners keep them running. Repair costs. Reliability improvements. High replacement prices. All play a role. Slower turnover reduces demand for new models. The used-car market absorbs more activity. New sales suffer.

PwC’s 2026 automotive outlook echoes the pressure on mature markets. “We expect unit sales growth in mature markets to plateau through 2030 due to the sticky prices for new vehicles, and our view reflects constrained consumer spending power and changing market preferences,” the firm stated in its analysis. Average transaction prices in the U.S. and Europe exceed $45,000 after 15 to 25 percent increases since 2020. Lending tightened. Macroeconomic uncertainty lingers. Households delay purchases or turn to used options. The demand ceiling feels real.

Yet the story is not uniform. China exports roughly three million vehicles annually to Europe, Latin America and Southeast Asia since 2020. Its domestic market benefits from lower prices near $25,000 and faster battery-cost declines. BloombergNEF’s latest Electric Vehicle Outlook projects EVs reaching 56 percent of global passenger sales by 2035 and 70 percent by 2040 in its base case. Those figures come from the firm’s June 2025 update. Adoption accelerates abroad. The U.S. lags. Only 24 percent of the American fleet may be electric by 2040 under some scenarios. Regulatory shifts and infrastructure gaps slow progress here.

The International Energy Agency paints a similar long-term picture. Electric-car sales should surpass 20 million globally in 2025. They represent more than a quarter of total sales. In a net-zero pathway, EVs hit 65 percent of new-car sales by 2030. Battery prices continue falling. Total cost of ownership favors electric models over time. Still, the U.S. market’s structural headwinds remain. Hybrids gain ground as a practical bridge. PwC notes their adoption has doubled in recent years. They carry a 5-to-10 percent premium over pure gasoline equivalents but deliver better ownership economics for many drivers.

Autonomous technology adds another variable. Bain’s modeling shows robotaxis could reduce the licensed driving population by two to three percentage points, down to 85 percent. Vehicles per driver might slip from 1.2 to 1.1. That translates to 10 to 20 percent of households shedding a vehicle entirely. Yet full autonomy has arrived more slowly than once predicted. The delay gives traditional automakers breathing room. It also postpones potential demand destruction. Uncertainty reigns.

Competition intensifies inside a smaller pie. “The competition in the U.S. is going to be ferocious,” Gottfredson warned. “There’s too many automakers and too many brands competing for the consumers. The market is going to have to consolidate.” Margins already compress. PwC reported industry EBITDA falling from nearly 11 percent in the third quarter of 2024 to below 8 percent a year later. Suppliers chase scale through mergers and acquisitions. Software-defined vehicles. Electrification. Autonomy. These demand heavy investment at a moment when volume growth has stalled.

Dealers face their own reckoning. Fewer new sales mean thinner service revenue over time. Financing volumes shrink. Insurance pools contract. Parts demand softens. Labor needs adjust. The entire value chain feels the contraction. Some manufacturers may exit segments or exit the market. Consolidation could produce larger, more efficient players. Consumers might see fewer choices and higher prices in the interim. The small, affordable sedans many crave have largely disappeared. Profit margins favor SUVs and trucks. That pattern persists even as buyers seek relief.

Recent analysis reinforces the trend. A June 2026 PwC outlook highlights how Chinese competition and domestic price sensitivity reshape global flows. BloombergNEF’s 2026 Electric Vehicle Outlook, released in recent weeks, trimmed long-term EV forecasts slightly for the second consecutive year. Growth continues. The pace moderates in key regions including the U.S. These updates arrive against a backdrop of record EV sales in 2025 and 2026. The transition unfolds. The total addressable market for personal vehicles may not expand with it.

Industry veterans remember different eras. Annual sales climbed with population, suburban expansion and rising incomes. That model no longer holds. Fertility trends move slowly but inexorably. Immigration policy shifts with politics. Vehicle longevity improves with each generation of engineering. Affordability crises have persisted long enough to alter habits. Younger cohorts normalize car-light lifestyles in dense cities. Ride-sharing costs fluctuate yet remain an option. The cumulative effect points lower.

Executives must plan for contraction rather than recovery. Product portfolios need realignment toward segments that still generate demand. Cost discipline becomes paramount. Investment in software and electrification must deliver returns even if unit volumes fall. Partnerships. Platform sharing. Selective mergers. These tactics gain appeal. Waiting for rates to ease or demographics to reverse looks risky. The data suggest structural change, not cyclical dip.

Global contrasts sharpen the picture. Emerging markets in Asia and Africa could add buyers. China’s export machine floods certain regions with affordable EVs. Europe pushes regulatory mandates that accelerate fleet turnover toward zero-emission models. The U.S. stands apart. Its mature market, high prices, aging buyer base and cultural attachment to personal vehicles create unique vulnerabilities. Sales may stabilize at a lower level. The days of 17 million units look like a historical anomaly rather than the new normal.

Longer term, the fleet itself could shrink. Higher utilization per vehicle through sharing or autonomy reduces the total number required. Vehicles lasting 15 or 20 years instead of 12 further dampen replacement demand. Deregistration rates falling to 4.4 percent capture that reality. The industry built on volume must adapt to one built on value per unit, utilization and services. Transition will prove painful for many participants.

Gottfredson offered no sugarcoating. Too many brands chase too few buyers in a market shaped by forces beyond easy control. Consolidation appears inevitable. Winners will be those who read the demographic and economic signals early. They resize operations. They innovate within the new boundaries. The road ahead narrows. Automakers that navigate it with clear eyes stand the best chance of survival.