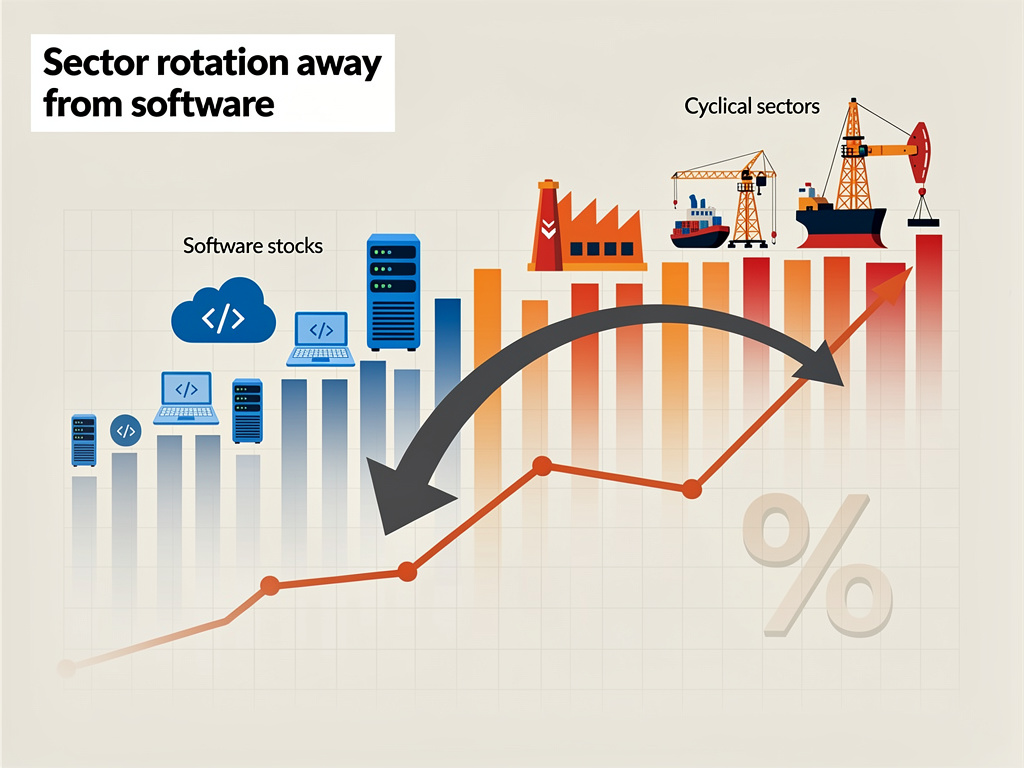

Wall Street’s love affair with technology stocks may be entering a prolonged cooling period, as major investment banks signal a fundamental shift in market dynamics that could reshape portfolio strategies through 2026. JPMorgan Chase analysts have issued a stark warning to investors: the decade-long dominance of software and technology equities is facing headwinds that extend far beyond typical market cycles, prompting a strategic rotation toward cyclical sectors that have languished in tech’s shadow.

The timing of this pivot comes as artificial intelligence hype reaches fever pitch, creating a paradox that has left many market participants questioning whether Wall Street’s smartest minds are missing the next great technological revolution or identifying an overextended bubble ready to deflate. According to Business Insider, JPMorgan’s equity strategy team has recommended clients reduce exposure to software stocks while increasing allocations to industrial, financial, and energy sectors—a dramatic departure from the playbook that generated outsized returns for much of the 2010s and early 2020s.

This strategic repositioning reflects deeper concerns about valuation compression, regulatory pressures, and the maturation of growth trajectories that once seemed limitless. The S&P 500’s technology sector, which commanded premium multiples justified by explosive growth rates, now faces a reckoning as interest rates remain elevated and investors demand profitability over promises. The rotation isn’t merely tactical—it represents a philosophical shift in how institutional capital views risk and reward in an economy transitioning from pandemic-era stimulus to normalized monetary policy.

Valuation Pressures Mount as Growth Narratives Fade

The mathematics underlying JPMorgan’s bearish software stance reveal uncomfortable truths about sector valuations. Software companies in the S&P 500 have historically traded at price-to-earnings multiples significantly above the broader market average, premiums justified by superior revenue growth and scalability. However, as growth rates decelerate toward mid-single digits for many enterprise software providers, those valuation premiums have become increasingly difficult to defend. The gap between expectations embedded in current stock prices and realistic earnings projections has widened to levels that historically preceded meaningful corrections.

JPMorgan analysts point to specific vulnerabilities within the software sector that extend beyond simple valuation concerns. Cloud computing growth, once considered an unstoppable force, has normalized as enterprise adoption reaches maturity in developed markets. Subscription revenue models that Wall Street once valued at astronomical multiples now face churn pressures as corporate IT budgets tighten and chief financial officers scrutinize software spending with unprecedented rigor. The shift from growth-at-all-costs to profitable growth has left many software companies struggling to maintain the narrative that justified their valuations.

The artificial intelligence boom, paradoxically, may be exacerbating rather than alleviating these pressures. While AI has generated enormous excitement and driven spectacular gains for semiconductor manufacturers and infrastructure providers, the benefits for traditional software companies remain largely theoretical. Many enterprise software firms have rebranded existing products with AI labels without fundamentally transforming their value propositions or growth trajectories. Investors are beginning to distinguish between companies genuinely positioned to capitalize on AI and those simply riding the hype cycle.

Cyclical Sectors Emerge from the Shadows

The flip side of JPMorgan’s recommendation involves a compelling case for sectors that have underperformed during technology’s dominance. Industrial companies, financial institutions, and energy producers offer valuations that appear attractive on both absolute and relative bases. These cyclical sectors have spent years in the wilderness, overlooked by growth-focused investors chasing the next Amazon or Microsoft. Now, with economic growth stabilizing and infrastructure spending increasing globally, the fundamental backdrop for cyclicals has improved materially.

Financial stocks present a particularly interesting opportunity within this rotation framework. Banks and insurance companies benefit directly from higher interest rates—the same monetary policy environment that pressures high-multiple technology stocks. Net interest margins have expanded significantly as the Federal Reserve maintained restrictive policy, translating to improved profitability for well-capitalized financial institutions. Regulatory concerns that once weighed heavily on the sector have moderated, while valuations remain compressed relative to historical averages and compared to the broader market.

Energy sector dynamics add another dimension to the rotation thesis. Despite political pressures and long-term transition risks, traditional energy companies have demonstrated remarkable discipline in capital allocation and shareholder returns. The sector’s valuation multiples reflect persistent skepticism about long-term viability, creating opportunities for investors willing to look beyond decarbonization narratives. Global energy demand continues growing, particularly in developing economies, while supply constraints and underinvestment in new production capacity support pricing power that translates to robust cash flows.

Institutional Money Follows the Smart Money

The JPMorgan recommendation carries weight beyond a single firm’s research report because it reflects broader positioning shifts among sophisticated institutional investors. Hedge funds, pension managers, and sovereign wealth funds have begun rotating capital away from technology concentration toward more diversified sector exposure. This movement creates self-reinforcing dynamics as outflows from technology funds pressure valuations while inflows to cyclical sectors provide support. The technical picture increasingly aligns with fundamental arguments for rotation.

Options market activity provides additional evidence of changing sentiment. Put option volumes on major technology ETFs have increased substantially, indicating growing hedging activity or outright bearish positioning. Conversely, call option interest in financial and industrial sector funds has picked up, suggesting investors are positioning for upside in previously neglected areas. These derivative flows often presage larger moves in underlying equities as market makers adjust their hedges and momentum builds.

The mutual fund and ETF industry has responded to shifting demand with new product launches targeting cyclical exposure and away from technology concentration. Asset managers recognize that a decade of technology outperformance has created crowded positioning and concentration risks in portfolios nominally designed for diversification. The proliferation of equal-weight strategies and sector-rotation funds reflects this awareness, providing vehicles for investors seeking to reduce technology exposure without completely exiting equity markets.

Historical Parallels and Precedents

Market historians point to previous periods when technology stocks faced extended underperformance following years of dominance. The aftermath of the dot-com bubble provides the most obvious parallel, though current circumstances differ in important respects. Today’s technology giants generate substantial profits and cash flows, unlike many late-1990s internet companies with questionable business models. However, the psychological dynamics share similarities—extended outperformance creates complacency, valuation discipline erodes, and eventually mean reversion asserts itself.

The 1970s offer another instructive example, when the “Nifty Fifty” growth stocks—including technology leaders of that era like IBM and Xerox—suffered prolonged underperformance despite strong underlying businesses. Valuation compression can persist for years when sentiment shifts and investors reassess appropriate multiples. The transition from growth to value leadership doesn’t require business deterioration; changing perceptions of risk and return suffice to drive sustained rotation.

JPMorgan’s timeline extending through 2026 suggests analysts expect this rotation to unfold gradually rather than through a sudden crash. Multi-year underperformance grinds down investor enthusiasm more effectively than sharp corrections that often create buying opportunities. The psychological shift required for sustained rotation takes time as investors abandon strategies that worked for years and embrace approaches that felt wrong throughout technology’s dominance.

Risks to the Rotation Thesis

Skeptics of the rotation narrative argue that technology’s structural advantages remain intact despite valuation concerns. Software economics—high gross margins, recurring revenue, and network effects—haven’t fundamentally changed. The best technology companies continue generating superior returns on invested capital and free cash flow conversion. Betting against innovation has proven costly historically, and artificial intelligence may yet deliver transformative changes that justify current valuations and drive further gains.

Macroeconomic developments could also derail the rotation thesis. If economic growth disappoints or recession materializes, cyclical sectors would likely suffer disproportionately while defensive technology businesses might outperform. The Federal Reserve’s policy path remains uncertain, and unexpected shifts in monetary policy could rapidly alter sector leadership. Geopolitical risks, from trade tensions to regional conflicts, introduce additional variables that could overwhelm sector-specific fundamentals.

The concentration of index returns in a handful of mega-cap technology stocks creates technical challenges for rotation advocates. Passive investing flows continue favoring market-cap weighted indices, providing structural support for the largest technology companies regardless of valuation or growth concerns. Breaking this technical support requires sustained active management outperformance—a difficult proposition given the industry’s mixed track record against benchmarks.

Portfolio Implications and Strategic Considerations

For investors evaluating JPMorgan’s rotation recommendation, implementation matters as much as the underlying thesis. Wholesale abandonment of technology exposure seems extreme given the sector’s genuine strengths and innovation potential. More nuanced approaches might involve trimming the most expensive software positions while maintaining exposure to technology leaders with reasonable valuations and durable competitive advantages. Selectivity within technology becomes paramount rather than blanket sector avoidance.

The case for increasing cyclical exposure appears stronger than the argument for eliminating technology entirely. Financial, industrial, and energy sectors offer compelling valuations and improving fundamentals that deserve consideration in diversified portfolios. The key question involves sizing these positions appropriately given individual risk tolerances and time horizons. Long-term investors might gradually shift allocations while maintaining flexibility to adjust as conditions evolve.

Ultimately, JPMorgan’s call for rotation through 2026 challenges investors to question assumptions formed during technology’s extended outperformance. Whether this marks the beginning of a multi-year regime change or proves a temporary interruption in technology’s dominance remains uncertain. What seems clear is that the easy money in software stocks has been made, and generating returns going forward will require more careful analysis, valuation discipline, and willingness to look beyond the sectors that dominated the previous decade. The great rotation may be underway, and investors ignoring the shift do so at their own peril.