The largest technology companies on Earth are engaged in a capital expenditure arms race unlike anything the industry has seen since the dot-com era. Amazon, Microsoft, Google, and Meta are collectively pouring hundreds of billions of dollars into artificial intelligence infrastructure — data centers, custom chips, cooling systems, and the vast networks of GPUs required to train and deploy ever-larger AI models. The bet is enormous, and the payoff remains uncertain. As 2026 approaches, Wall Street is beginning to ask a pointed question: When does all this spending start generating commensurate returns?

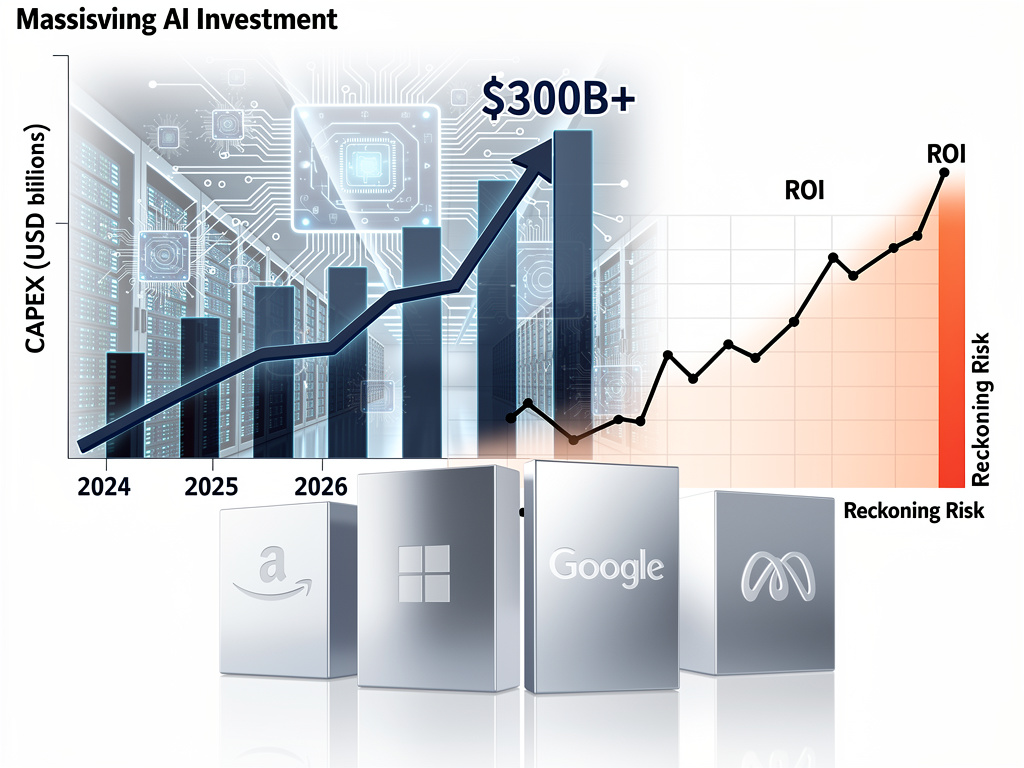

According to Business Insider, the hyperscalers are expected to spend more than $300 billion combined on capital expenditures in 2025 alone, a staggering figure that has prompted both excitement and anxiety among investors. The publication reports that the AI spending boom is creating a critical inflection point: either the massive infrastructure investments will be validated by surging enterprise demand and consumer adoption, or the industry will face a painful period of overcapacity and margin compression.

A Capital Expenditure Surge Without Modern Precedent

The numbers are breathtaking in their scale. Microsoft has signaled capital expenditure plans exceeding $80 billion for its fiscal year 2025, much of it directed at AI-related data center buildouts. Alphabet, Google’s parent company, has outlined similarly ambitious plans, with CEO Sundar Pichai telling analysts that the risk of underinvesting in AI far outweighs the risk of overinvesting. Amazon Web Services, the dominant cloud infrastructure provider, continues to expand its data center footprint at a furious pace, with capital spending expected to top $100 billion. Meta, meanwhile, has committed tens of billions to its AI ambitions under Mark Zuckerberg’s directive to make the company a leader in artificial general intelligence research.

This spending trajectory represents a fundamental shift in how Big Tech allocates capital. For years, these companies generated enormous free cash flow that funded share buybacks, dividends, and relatively modest infrastructure expansion. Now, the calculus has changed. As Business Insider detailed, executives at each of these firms have made the strategic decision that AI infrastructure is an existential investment — one that cannot be deferred without risking competitive irrelevance.

Wall Street’s Growing Impatience for Returns

Investors have largely given Big Tech the benefit of the doubt so far, buoyed by the explosive growth of generative AI applications like ChatGPT, Microsoft’s Copilot suite, and Google’s Gemini models. But patience has limits. Analysts are increasingly scrutinizing the gap between capital deployed and revenue generated from AI-specific products and services. The core concern, as outlined by Business Insider, is that 2026 will be the year when the market demands proof that these investments are translating into durable, high-margin revenue streams.

The tension is already visible in earnings calls. When Alphabet reported its most recent quarterly results, investors initially sold off the stock despite strong revenue growth, partly because capital expenditure guidance came in higher than expected. The same dynamic has played out with Microsoft and Meta, where any hint that spending might accelerate further has been met with skepticism. The market is signaling that it wants to see operating leverage — the point at which revenue growth begins to outpace spending growth — and it wants to see it soon.

The Enterprise Adoption Question

The bull case for Big Tech’s AI spending rests heavily on enterprise adoption. The theory is straightforward: as companies across every industry integrate AI into their operations — from customer service chatbots to supply chain optimization to drug discovery — demand for cloud-based AI computing will explode. Amazon, Microsoft, and Google are all positioning their cloud platforms as the primary delivery mechanism for AI capabilities, and each has reported strong growth in AI-related cloud revenue.

But the pace of enterprise adoption remains a subject of debate. While early adopters in financial services, healthcare, and technology have moved aggressively to deploy AI tools, many large enterprises are still in the experimentation phase. Proof-of-concept projects have not always translated into full-scale deployments, and concerns about data privacy, regulatory compliance, and the reliability of AI outputs have slowed adoption in regulated industries. According to recent reporting from Reuters, enterprise AI spending is growing but remains concentrated among a relatively small number of large customers, raising questions about the breadth of demand.

The GPU Supply Chain and Nvidia’s Pivotal Role

No discussion of the AI spending boom is complete without addressing Nvidia, the chipmaker whose graphics processing units have become the essential building blocks of AI infrastructure. Nvidia’s data center revenue has grown at a pace that would have seemed fantastical just three years ago, driven almost entirely by purchases from the hyperscalers. The company’s H100 and newer Blackwell-architecture chips command premium prices and remain in high demand, giving Nvidia extraordinary pricing power.

Yet the GPU supply chain also represents a risk factor. If demand for AI computing plateaus or if the hyperscalers pull back on spending, Nvidia’s revenue growth could decelerate sharply — a scenario that would ripple through the entire semiconductor ecosystem. Conversely, each of the major cloud providers is investing heavily in custom silicon — Amazon’s Trainium and Inferentia chips, Google’s TPUs, and Microsoft’s Maia accelerators — in an effort to reduce their dependence on Nvidia and lower the per-unit cost of AI inference workloads. The success or failure of these custom chip programs will be a critical variable in determining whether the economics of AI infrastructure improve over time.

The Overcapacity Risk: Lessons From Previous Tech Cycles

History offers cautionary tales. The late 1990s telecommunications boom saw companies like WorldCom, Global Crossing, and others lay vast amounts of fiber-optic cable in anticipation of internet traffic growth that did eventually materialize — but not before a brutal period of overcapacity, bankruptcies, and write-downs. The parallel is imperfect but instructive. As Business Insider noted, some analysts worry that the current AI infrastructure buildout could follow a similar pattern: the long-term demand thesis may prove correct, but the timing mismatch between investment and returns could punish investors in the interim.

The key difference, bulls argue, is that today’s hyperscalers are far more financially robust than the telecom companies of the late 1990s. Amazon, Microsoft, Google, and Meta generate hundreds of billions of dollars in combined annual revenue and maintain fortress-like balance sheets. They can absorb a period of elevated spending without existential risk. But even for companies of this scale, sustained capital expenditure at current levels will compress free cash flow and could limit their ability to return capital to shareholders — a dynamic that some institutional investors are already flagging as a concern.

The Monetization Playbook: From Infrastructure to Revenue

Each of the major players is pursuing a slightly different monetization strategy. Microsoft has arguably moved most aggressively, embedding AI capabilities across its Office 365 suite through Copilot and charging premium prices for AI-enhanced subscriptions. The company has also deepened its partnership with OpenAI, giving it a privileged position in the generative AI ecosystem. Amazon is focused on making AWS the platform of choice for AI model training and inference, offering a broad menu of tools and services designed to attract both startups and large enterprises. Google is leveraging its AI research prowess — particularly through DeepMind — to enhance its search, advertising, and cloud businesses simultaneously.

Meta presents perhaps the most unconventional case. Unlike its peers, Meta does not operate a major cloud computing business, so its AI investments are primarily directed at improving its advertising targeting, content recommendation algorithms, and long-term research into artificial general intelligence. Zuckerberg has framed AI as the next great computing platform, analogous to mobile, and has committed to open-sourcing many of Meta’s AI models through the Llama family — a strategy designed to build an ecosystem around Meta’s technology even if it doesn’t generate direct infrastructure revenue.

What 2026 Will Reveal About the AI Bet

The coming eighteen months will be decisive. By mid-2026, the first wave of massive data center buildouts currently under construction will be fully operational, adding enormous new capacity to the global AI computing supply. If enterprise demand scales in tandem — driven by the deployment of AI agents, autonomous systems, and next-generation applications — the hyperscalers’ bets will be vindicated, and the current spending levels will look prescient. If demand growth disappoints, the industry could face a period of reckoning characterized by utilization rate concerns, pricing pressure, and investor backlash.

For now, the executives leading these companies are betting that the transformative potential of artificial intelligence justifies the extraordinary capital commitments. As Pichai, Jassy, Nadella, and Zuckerberg have each argued in their own way, the cost of missing the AI wave would be far greater than the cost of building too much infrastructure too soon. Whether that conviction holds up under the unforgiving scrutiny of quarterly earnings reports and stock market expectations will be one of the defining business stories of 2026 and beyond.