Michael Saylor built Strategy into Bitcoin’s most visible corporate champion. The company once boasted it would never sell. Now it has. And the scale surprised even seasoned watchers.

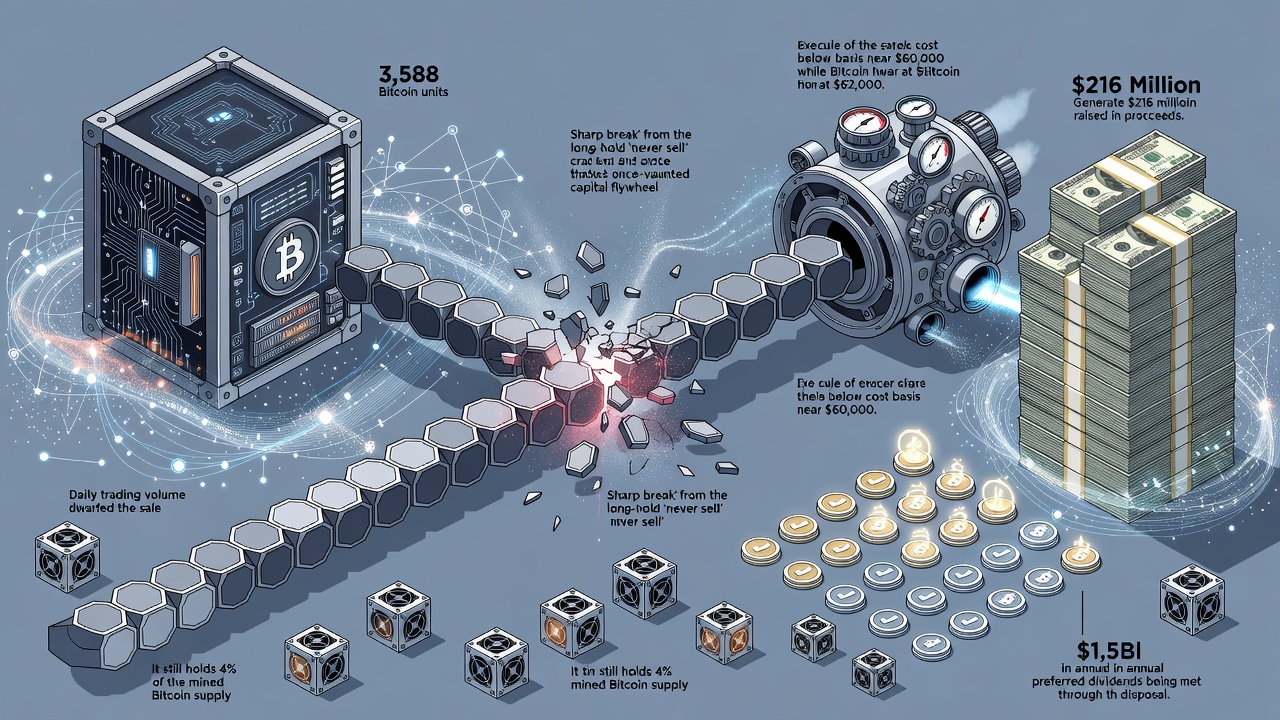

Between June 29 and July 5, Strategy unloaded 3,588 Bitcoins. The take? $216 million. That disclosure landed July 6. It marked the largest single sale in the firm’s six-year accumulation drive. The average exit price sat near $60,000. The company’s blended cost basis? Roughly $75,700. A loss, plain and simple. Yet the proceeds went straight to cover dividend obligations on a thick stack of preferred instruments. No drama in the filing. Just numbers. But the signal rippled fast.

Saylor once framed a tiny 32-Bitcoin sale as market “inoculation.” This transaction ran more than 100 times larger.

The Motley Fool first flagged the details and immediate questions it raised for retail holders. (The Motley Fool) Days later, major outlets piled on with fresh reporting. Fortune called it the “crypto hoarder’s largest sale ever.” (Fortune) CoinDesk highlighted the dramatic acceleration in pace. (CoinDesk) The Wall Street Journal examined how Strategy now finds itself trapped by its own Bitcoin math. (The Wall Street Journal)

So what changed? Start with the capital structure. Strategy carries several classes of preferred shares. Four of them pay cash dividends. The annual tab runs about $1.5 billion. For years the model hummed. Issue common shares at a premium to net asset value. Buy more Bitcoin. Higher coin prices lifted the stock. Investors tolerated dilution because the flywheel spun upward. That premium has now collapsed. In late June, MSTR shares traded below the value of its Bitcoin holdings. Issuing equity at those levels would punish existing owners. The old playbook broke.

Enter the Digital Credit Capital Framework. Unveiled in late June, it authorized sales of up to $1.25 billion in Bitcoin. The goal? Build cash reserves. Service those preferred payouts. Avoid further equity dilution. The first big test arrived almost immediately. Two tranches made up the recent sale. One moved 1,363 BTC for $80.8 million. The second cleared 2,225 BTC for $135.2 million. Proceeds funded distributions and replenished the USD reserve. After the deal, Strategy held 843,775 Bitcoins and $2.55 billion in cash, according to Saylor’s own update on X.

But hold on. This isn’t capitulation in the classic sense. Daily Bitcoin trading volume hit $33.2 billion on July 7. The sale represented a rounding error. Strategy still controls roughly 4% of all mined coins in circulation. A few thousand coins per quarter won’t drain the ocean. Yet the optics matter. Saylor had long preached “never sell your Bitcoin” to retail audiences. He once suggested people sell a kidney before parting with coins. The shift to corporate pragmatism stings for some.

And. Recent buying adds irony. Just days before the sale, the company acquired 3,657 Bitcoins at higher prices. That produced an $8.3 billion unrealized loss on the broader portfolio for the quarter. Realized losses from the sale itself stayed modest. The mismatch between recent purchases and this sale underscores the bind. Fixed cash obligations meet volatile asset prices. Something has to give.

Analysts split on the implications. Bernstein and others view Strategy as a net buyer over longer horizons. The firm scooped 85,000-plus Bitcoins in the second quarter alone against this one sale. Saylor himself described the earlier small sale as a way to normalize the idea of modest disposals. It inoculates the market against future shock. JPMorgan takes a harder line. The preferred-share structure, especially the heavily marketed STRC notes held by retail, now carries real risk if Bitcoin stays depressed. A negative feedback loop looms. Lower coin prices compress the premium. Equity issuance becomes toxic. Preferred instruments lose appeal. More Bitcoin must be sold to pay the bills. Pressure builds.

Bitcoin itself barely flinched. It dipped about 1% in the first hour after the news, then recovered above $62,000. Market participants seem to price in the volume as manageable. Yet the episode exposes deeper tensions in Saylor’s model. The company converted its software business into a leveraged Bitcoin bet. That bet once looked unstoppable. Now the leverage cuts both ways. Perpetual preferreds demand cash regardless of coin direction. When the equity premium evaporates, the treasury itself becomes the backstop.

History offers mixed lessons. Strategy did sell Bitcoin in late 2022, but only to harvest tax losses before repurchasing. This round feels different. It’s not tax-driven. It’s structural. And it arrives while Bitcoin sits 54% off its all-time high, per recent analysis. (The Motley Fool) Some voices on X frame it as the start of a reset. Others see tactical treasury management in a tough stretch. Saylor continues to argue that if Bitcoin appreciates faster than the dividend yield on the credit stack, the math works long term. He has said the firm can fund payouts through capital gains and still grow its Bitcoin per share.

Investors face a sharper question. Does this sale represent prudent adaptation to new realities? Or does it mark the moment when the virtuous cycle turned vicious? The answer likely hinges on where Bitcoin trades over the next several quarters. Stay above the cost basis and the pressure eases. Slip below for an extended period and sales could accelerate. Even then, liquidating the entire hoard wouldn’t erase Bitcoin’s underlying scarcity or network effects. It would simply transfer coins to new hands.

Short-term noise. That’s how many Bitcoin natives dismiss it. The asset’s fundamentals remain intact. Adoption marches forward. Yet for a company that once defined maximalist conviction, the shift carries symbolic weight. Strategy didn’t just sell Bitcoin. It rewrote part of its founding creed to survive the current math. Markets will watch the next 8-K filing closely. So will holders who took Saylor’s earlier words as gospel.

The empire hasn’t fallen. But the guardrails look different now. And everyone from retail speculators to institutional desks must recalibrate accordingly.