A recent Motley Fool article highlights the arrival of a fresh competitor in the stablecoin market that intends to challenge the dominance of Circle’s USDC. This development arrives as the sector continues to expand rapidly, with total stablecoin supply now exceeding $250 billion and showing no signs of slowing. The new entrant, currently known by the project name StellarX, brings a distinct approach that focuses on yield generation, regulatory clarity, and integration with traditional banking rails.

Stablecoins have grown from niche tools used primarily by cryptocurrency traders into instruments that facilitate cross-border payments, remittances, and even corporate treasury management. USDC, issued by Circle and backed one-to-one by cash and short-term U.S. Treasuries, commands a significant share of the market behind only Tether’s USDT. Circle has built its reputation on transparency, regular attestations from accounting firms, and partnerships with major financial institutions. Yet the stablecoin space remains open to disruption, particularly as issuers seek ways to offer holders more than the zero or near-zero yields that have become standard.

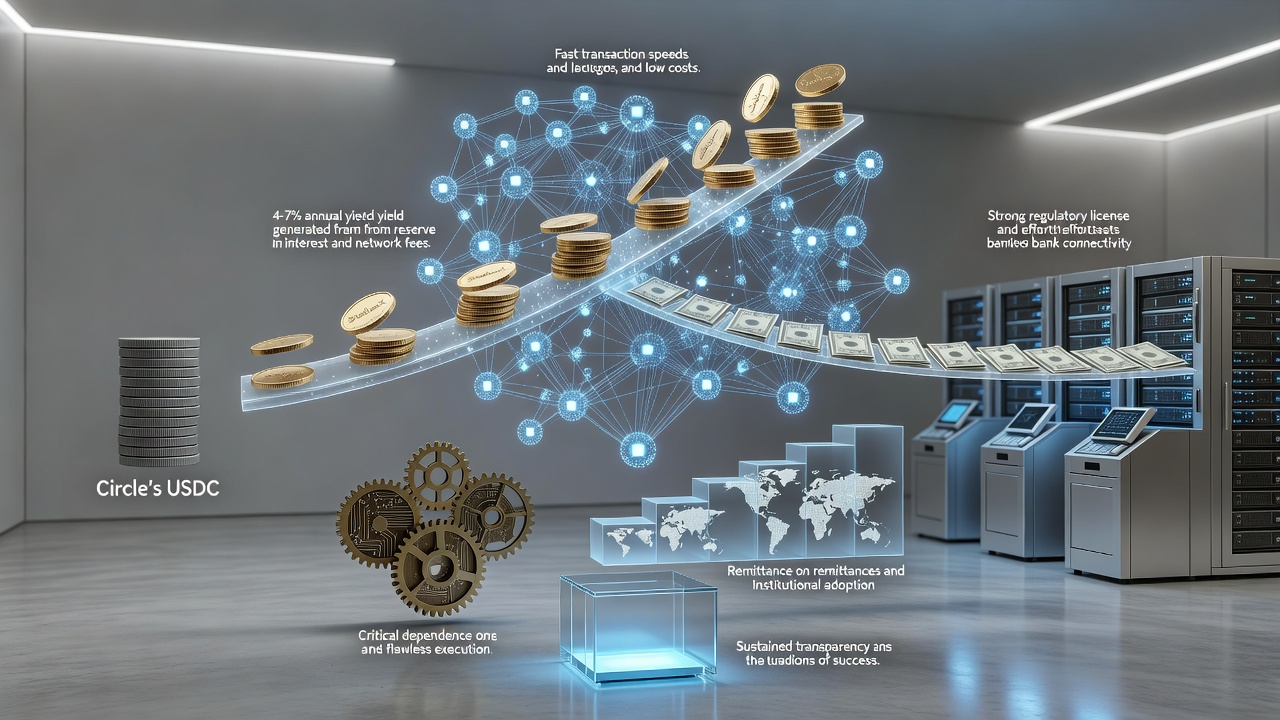

StellarX differentiates itself by promising holders a competitive annual percentage yield paid directly in additional tokens. The mechanism relies on a combination of interest earned from reserve assets and revenue generated through the project’s payment and settlement network. Rather than simply parking reserves in Treasury bills and passing minimal returns to users, the protocol allocates a portion of protocol-level fees back to token holders. Early projections shared by the development team suggest yields could range between 4 and 7 percent annually once the system reaches sufficient scale, though actual returns will depend on interest rates, adoption levels, and operational costs.

The project is built on a hybrid blockchain architecture that combines elements of the Stellar network with newer layer-two scaling solutions. This design choice aims to deliver transaction finality in under three seconds while maintaining costs below one cent per transfer. Such performance metrics matter particularly for use cases in emerging markets where remittances represent a meaningful percentage of household income. According to data from the World Bank, remittance costs still average above 6 percent in many corridors; a stablecoin that can reduce those fees while offering yield could attract both individual users and financial institutions looking to modernize their rails.

Regulatory preparedness forms another pillar of the StellarX strategy. The team has engaged early with the New York Department of Financial Services and has applied for a limited-purpose trust charter in South Dakota. These steps reflect lessons learned from previous stablecoin issuers that faced enforcement actions or unexpected regulatory hurdles. By securing licenses before launching at full scale, the project hopes to position itself as a compliant alternative that large corporations and banks can adopt without fear of future crackdowns. Circle itself has spent years obtaining money transmitter licenses across U.S. states and maintains a Money Services Business registration with FinCEN, yet the regulatory environment has grown only more complex with new legislation under consideration in Congress.

One notable feature of StellarX involves direct integration with traditional bank accounts through partnerships with several regional banks. Users will be able to mint and redeem the stablecoin directly from their checking accounts without first converting to another cryptocurrency. This on-ramp and off-ramp simplicity addresses a persistent pain point for mainstream adoption. Circle has made progress in this area through its Circle Account product, but many users still report friction when moving between traditional finance and blockchain systems. If StellarX can deliver a genuinely straightforward experience, it may capture market share among businesses that want stable digital dollars without needing to manage crypto wallets or private keys.

The competitive dynamics between StellarX and USDC will likely center on three areas: yield, usability, and institutional trust. USDC benefits from first-mover advantage, an established brand, and deep liquidity across decentralized finance platforms. Many decentralized exchanges, lending protocols, and decentralized autonomous organizations hold USDC as their primary reserve asset. Switching costs are real. Developers who have written smart contracts around USDC would need to update code, liquidity providers would need to migrate pools, and users would need to adjust their habits.

Yet history shows that dominant market positions in digital assets can erode when superior value propositions emerge. Tether maintained an overwhelming lead for years despite repeated transparency concerns, only to see USDC gain meaningful ground between 2020 and 2023. More recently, PayPal’s PYUSD has demonstrated that a well-resourced incumbent from traditional finance can carve out a niche, even if it has not yet reached the scale of the top two stablecoins. StellarX enters this fray with backing from several venture capital firms known for successful crypto investments, including a lead investment from a fund that previously supported both Circle and Coinbase.

Yield-bearing stablecoins are not an entirely new concept. Projects such as Mountain Protocol’s USDM and Ethena’s USDe have already introduced versions of this idea, though each takes a different technical approach. USDM allows holders to earn yield by staking the token and receiving a share of protocol revenue, while USDe relies on a delta-neutral hedging strategy involving perpetual futures. StellarX appears to follow a more conservative path by focusing primarily on interest from high-quality reserves and transaction fees rather than derivatives exposure. This choice may appeal to institutions wary of the additional risks that come with synthetic yield methods.

Adoption will ultimately determine whether StellarX succeeds in its challenge to USDC. The project has announced several pilot programs with payment companies in Southeast Asia and Latin America, regions where demand for dollar-denominated payment rails remains strong due to local currency volatility. Early results from these pilots show transaction volumes growing month-over-month, though the absolute numbers remain small compared with established players. The team plans a phased rollout that begins with these emerging market corridors before expanding into European and North American markets once additional licenses are secured.

Transparency measures will play a key role in building confidence. The project has committed to monthly attestations from a top-tier accounting firm, similar to the process Circle follows. Beyond basic reserve verification, StellarX promises to publish detailed breakdowns of how yield is calculated and distributed. Such disclosures could help differentiate the token from competitors that offer less visibility into their operations. Regular communication from the development team through both traditional press channels and on-chain governance updates will also be necessary to maintain credibility as the project scales.

The broader macroeconomic environment provides both tailwinds and potential headwinds for all stablecoin issuers. Higher interest rates have made reserve assets more productive, allowing issuers to generate substantial revenue from their treasuries. This reality has prompted many observers to ask why stablecoin holders have not historically received a larger share of that income. StellarX directly addresses this question by baking yield distribution into its core design. Should the Federal Reserve begin cutting rates later in 2026 or 2027, the available yield will naturally compress, testing whether the project can still offer competitive returns through its payment network fees.

Critics have raised questions about the sustainability of yield-bearing stablecoins. Some argue that offering attractive yields could incentivize speculative behavior rather than genuine payment usage. Others worry that in times of market stress, redemption queues could form if reserve liquidity becomes constrained. The StellarX team has attempted to address these concerns by maintaining a conservative reserve composition and implementing circuit breakers that can temporarily adjust yield distributions during periods of extreme volatility. Whether these safeguards prove sufficient will only be known during the next significant market downturn.

For Circle, the emergence of a well-funded and thoughtfully designed competitor serves as a reminder that market leadership must be continually earned. The company has responded by accelerating its own product development, including plans for a yield-bearing version of USDC aimed at institutional clients. This competitive pressure benefits users and the broader industry by driving innovation and forcing all participants to improve their offerings. Circle has also expanded its focus beyond stablecoins into payment infrastructure and compliance tools, seeking to build a more comprehensive financial technology platform.

The stablecoin market still has substantial room to grow. Estimates suggest that total supply could reach one trillion dollars within the next five years if adoption continues at current rates. Much of this expansion is expected to come from traditional financial institutions incorporating stablecoins into their product suites for settlement, collateral, and client liquidity management. In this environment, the winner may not be the issuer with the largest existing market share but rather the one that best combines regulatory compliance, attractive economics for users, and superior technology.

StellarX still faces significant execution risks. Building a compliant, scalable, and secure stablecoin system requires expertise across cryptography, traditional finance, regulatory affairs, and software engineering. The project must also navigate complex international tax considerations related to yield distributions, as different jurisdictions treat staking rewards and interest payments differently. Success will depend on the team’s ability to attract talent, maintain security standards, and execute against an ambitious roadmap without major setbacks.

As more companies explore blockchain-based payment solutions, the competition among stablecoin providers will likely intensify. Users stand to benefit from lower fees, higher yields where appropriate, and improved user experiences. For businesses that send or receive frequent cross-border payments, the ability to hold a stable digital dollar that earns interest while remaining instantly transferable represents a meaningful improvement over traditional banking products. Whether StellarX can capture a meaningful portion of the market from Circle’s USDC remains to be seen, but its entry adds another compelling option to an already dynamic sector.

The coming months will reveal how quickly the new stablecoin gains traction among both retail users and institutional partners. Early indicators from pilot programs suggest genuine demand for a product that combines stability, yield, and ease of use. If the project can deliver on its technical promises while maintaining the highest standards of regulatory compliance and transparency, it may indeed pressure USDC’s dominant position. The stablecoin market has always rewarded those who solve real problems for real users, and the coming contest between established leaders and ambitious newcomers promises to drive continued progress across the entire industry.