For nearly two centuries, Siemens AG has reinvented itself through successive waves of technological transformation — from telegraphs to turbines, from factory automation to digital twins. Now, the German industrial conglomerate is riding what may be its most consequential tailwind yet: the explosive global demand for artificial intelligence infrastructure and the data centers that power it.

On February 13, 2025, Siemens raised its full fiscal year 2025 outlook after posting a strong first quarter, citing robust demand driven by AI-related infrastructure spending. The company’s results sent a clear signal to investors and industry watchers alike — the AI revolution is not merely a software story. It is rapidly becoming a hardware and infrastructure story, and Siemens is positioning itself squarely at the center of that transformation.

A Quarter That Beat Expectations Across the Board

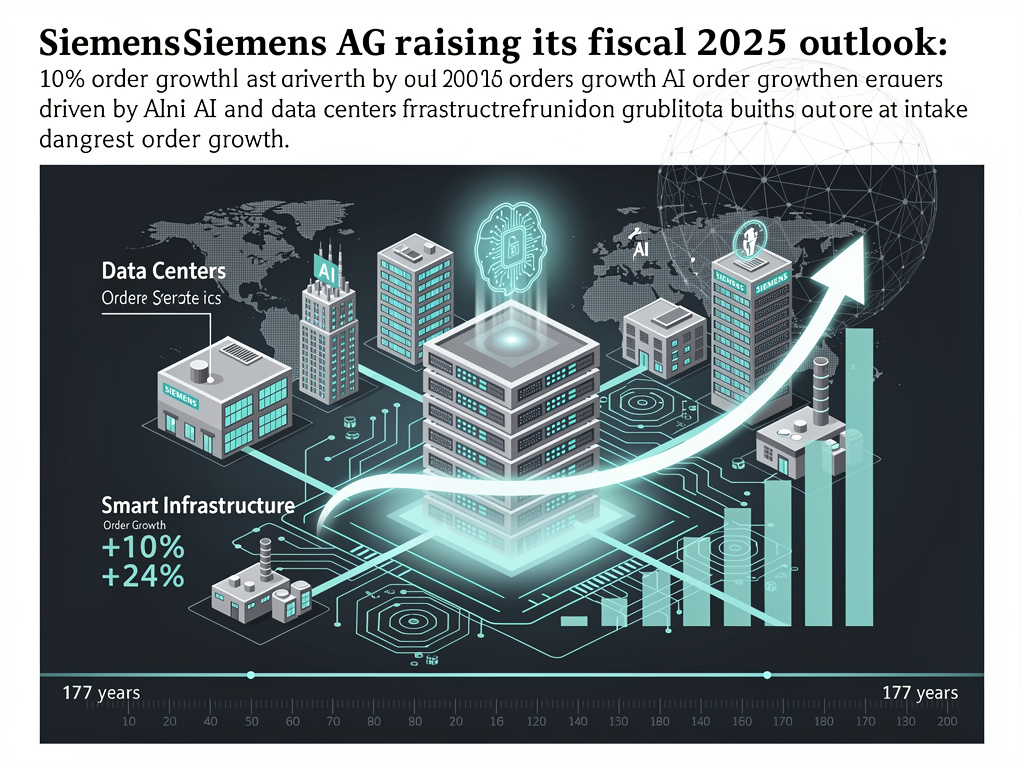

Siemens reported first-quarter revenue of €18.4 billion, a 3% increase year over year on a comparable basis. But the real headline was in orders: the company booked €20.8 billion in new orders, representing a 10% increase over the same period last year. That order growth was led by the company’s Smart Infrastructure division, which saw orders surge 24% to €6.3 billion, as reported by Manufacturing Dive.

The Smart Infrastructure segment, which provides electrical products, building automation systems, and energy distribution technology, has become a primary beneficiary of the global data center construction boom. Data centers require enormous amounts of electrical infrastructure — from power distribution and switchgear to cooling systems and building management platforms — and Siemens is one of the few companies in the world capable of delivering integrated solutions at scale.

CEO Roland Busch Sees AI as a Structural Growth Driver

Siemens CEO Roland Busch was unequivocal about the source of the company’s momentum. “We had an outstanding start to fiscal 2025,” Busch said during the company’s earnings call, emphasizing that AI and data center demand are not cyclical blips but structural growth drivers that will persist for years. He pointed to the company’s raised guidance as a reflection of management’s confidence in the durability of these trends.

For fiscal 2025, Siemens now expects comparable revenue growth of 5% to 7%, up from its prior guidance of 3% to 7%. The company also raised its earnings per share forecast to a range of €10.40 to €11.00, compared with the previous range of €10.40 to €11.00. The book-to-bill ratio — a key indicator of future revenue — stood at a healthy 1.13, meaning Siemens is booking more orders than it is currently fulfilling, building a strong backlog for coming quarters.

The Data Center Gold Rush and Its Industrial Ripple Effects

The scale of global data center investment is staggering. According to recent estimates from multiple industry analysts, global spending on data center construction and infrastructure is expected to exceed $350 billion annually by 2027, driven primarily by the compute requirements of large language models, generative AI applications, and cloud computing expansion. Companies like Microsoft, Amazon, Google, and Meta have each announced capital expenditure plans in the tens of billions of dollars for 2025 alone.

This spending does not simply flow to chip designers like Nvidia or cloud platform operators. It cascades through the entire industrial supply chain — to electrical equipment manufacturers, power generation companies, cooling technology providers, and construction firms. Siemens, with its diversified portfolio spanning electrification, automation, and digitalization, is uniquely positioned to capture value at multiple points along this chain. As Manufacturing Dive noted, the Smart Infrastructure division’s 24% order growth is a direct reflection of this dynamic.

Smart Infrastructure: The Division Powering Siemens’ AI Play

The Smart Infrastructure segment deserves particular scrutiny because it illustrates how traditional industrial businesses are being transformed by the AI era. The division manufactures and sells medium-voltage and low-voltage power distribution equipment, fire safety systems, building management platforms, and grid-edge technologies. These are not glamorous products — they are the unglamorous but essential backbone of every data center, hospital, factory, and commercial building on the planet.

What has changed is the volume and urgency of demand. Hyperscale data center operators are racing to bring new capacity online as quickly as possible to meet the insatiable demand for AI training and inference compute. Each new facility requires massive electrical infrastructure buildouts, often with lead times that stretch months or even years. Siemens’ ability to deliver these systems reliably and at scale gives it a significant competitive advantage over smaller, less diversified rivals.

Digital Industries and Automation: A More Mixed Picture

While Smart Infrastructure surged, Siemens’ Digital Industries division — which focuses on factory automation and industrial software — presented a more nuanced picture. The segment has been navigating a period of inventory normalization, particularly in China, where the manufacturing sector has been slower to recover than many analysts had hoped. However, even here, Siemens sees reasons for optimism. The company’s Xcelerator digital platform, which integrates industrial IoT, simulation, and AI-powered analytics, continues to gain traction among manufacturers seeking to digitize their operations.

Busch has repeatedly emphasized that Siemens’ industrial software business — anchored by its Teamcenter and Mendix platforms — represents a long-term strategic asset. As factories become increasingly automated and data-driven, the demand for digital twin technology, predictive maintenance, and AI-optimized production planning is expected to grow substantially. Siemens’ $4.6 billion acquisition of Brightly Software in 2022 and its ongoing investments in industrial AI capabilities underscore this strategic bet.

Siemens Healthineers and Mobility Round Out the Portfolio

Beyond its core industrial divisions, Siemens also benefits from its majority stake in Siemens Healthineers, the medical technology company, and its Siemens Mobility division, which supplies rail infrastructure and rolling stock. Healthineers has been integrating AI into diagnostic imaging and laboratory diagnostics, while Mobility continues to benefit from global investments in sustainable transportation infrastructure. Together, these businesses provide Siemens with a degree of diversification that insulates it from downturns in any single end market.

The company’s overall industrial profit margin came in at 15.9% for the quarter, reflecting strong operational execution across its portfolio. Management indicated that margin expansion remains a priority, with ongoing efforts to optimize supply chains, reduce costs, and shift the business mix toward higher-margin software and services revenue.

How Siemens Stacks Up Against Global Peers

Siemens’ AI-driven growth story does not exist in isolation. Competitors like Schneider Electric, ABB, and Eaton have also reported strong demand tied to data center electrification. Schneider Electric, in particular, has been aggressive in positioning itself as a data center infrastructure leader, recently reporting record order intake in its energy management division. ABB has similarly highlighted data center demand as a key growth driver for its electrification business.

What distinguishes Siemens is the breadth of its portfolio and its deep integration of hardware and software capabilities. Few companies can offer a customer everything from the medium-voltage switchgear that connects a data center to the grid, to the building management system that optimizes its energy consumption, to the digital twin platform that models its operations in real time. This end-to-end capability is increasingly valued by hyperscale operators who prefer to work with a smaller number of trusted, large-scale suppliers.

What the Raised Outlook Signals for the Broader Industrial Sector

Siemens’ upgraded guidance carries implications that extend well beyond its own balance sheet. When a company of Siemens’ size and diversification raises its outlook on the basis of AI-related infrastructure demand, it serves as a powerful signal to the broader industrial sector. It suggests that the AI investment cycle is not only real but accelerating, and that its benefits are flowing through to traditional industrial companies in tangible, measurable ways.

For investors, the message is clear: the AI trade is no longer confined to semiconductor stocks and software companies. Industrial conglomerates with exposure to power infrastructure, electrification, and building technology are emerging as significant beneficiaries. Siemens’ stock has reflected this thesis, trading near all-time highs in early 2025 as the market prices in sustained demand growth.

As Roland Busch put it, Siemens is experiencing a “once-in-a-generation” convergence of electrification, digitalization, and AI adoption. For a company that has survived and thrived through multiple technological revolutions over 177 years, this may prove to be among the most transformative yet. The question is no longer whether AI will reshape industrial markets — it is how quickly, and which companies will capture the most value. Siemens, with its first-quarter results and raised outlook, has made a compelling case that it intends to be at the front of that line.