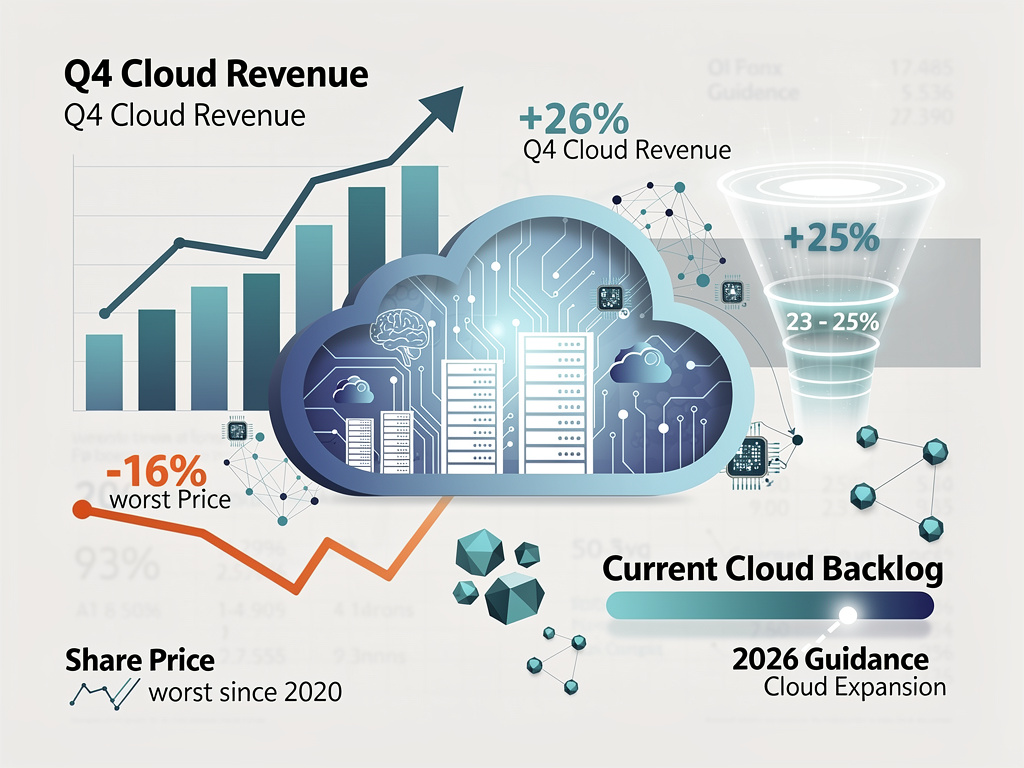

SAP SE’s shares plunged as much as 16% in Frankfurt trading Thursday, marking the steepest intraday drop since October 2020, after the German software giant disclosed a shortfall in its closely watched current cloud backlog for the fourth quarter. Total revenue rose 3% year-over-year to €9.68 billion, meeting analyst expectations, while adjusted non-IFRS operating profit surged 27% to €2.83 billion. Yet, the current cloud backlog grew just 16% to €21.05 billion—or 25% at constant currencies—falling short of the company’s internal 26% target.

Cloud revenue shone brightly, climbing 19% to €5.61 billion in the quarter, or 26% at constant currencies, with the Cloud ERP Suite up 30% at constant currencies to €4.86 billion. For the full year 2025, cloud revenue reached €21.02 billion, up 23% reported and 26% at constant currencies, beating prior estimates. Total cloud backlog hit a record €77.29 billion, up 30% at constant currencies, signaling robust long-term commitments amid SAP’s pivot from legacy on-premise licenses.

CEO Christian Klein emphasized the strength underneath, stating in the earnings release, “Q4 was a strong cloud quarter, with bookings resulting in 30% Total Cloud Backlog growth to a record 77 billion Euros.” He added that SAP Business AI featured in two-thirds of Q4 cloud order entry, driving adoption across the ERP suite. Wins included Adidas, L’Oréal, Pirelli, Nokia, the US Navy, Dexco, Lockheed Martin, and Rolls-Royce, with nearly half expanding software and cloud capabilities.

Backlog Miss Sparks Investor Fears

CFO Dominik Asam candidly addressed the slowdown on the earnings call, admitting, “This is a more pronounced slowdown than what we had anticipated and more than the slight deceleration we guided to at the beginning of last year.” He pinned the roughly 1 percentage point drag on Q4 constant currency growth to large transformational deals with revenue ramps pushed into outer years, plus termination-for-convenience clauses mandated by law, alongside geopolitical tensions favoring sovereign SaaS solutions that extend negotiations, especially in government, defense, and sensitive sectors. Benzinga highlighted Asam’s remarks as key to the stock’s premarket sink to a 52-week low.

Analysts echoed the disappointment. Morgan Stanley’s Adam Wood called the backlog “disappointing, especially given the company’s more positive commentary at the 3Q results and through year end,” per Bloomberg. JPMorgan’s Toby Ogg noted the 2026 guidance implies further deceleration. UBS deemed the 25% growth a miss against prior 26% hopes, as reported by CNBC. Shares traded down over 11% early, erasing gains and pressuring the stock to levels not seen since mid-2024, according to Morningstar.

Klein pushed back on demand worries, insisting, “It’s a reflection of what is happening in the world… This is not a reflection of a demand issue.” He reiterated, “To make this very clear, we are winning deals because of AI. We are not losing deals because of AI.” The backlog slip stems from prolonged client negotiations over sanctions, export curbs, and regulations, not softening orders.

2026 Outlook Balances Optimism and Caution

SAP guided 2026 cloud revenue to €25.8-€26.2 billion at constant currencies, implying 23-25% growth from 2025’s €21.02 billion—slightly below some analyst averages around €26 billion. Cloud and software revenue is projected at €36.3-€36.8 billion (12-13% growth), non-IFRS operating profit at €11.9-€12.3 billion (14-18% rise), and free cash flow near €10 billion. Constant currency current cloud backlog growth will “slightly decelerate” from 2025’s 25%, but total revenue acceleration is expected through 2027 as cloud migrations hasten software support declines. SAP’s official release detailed these figures.

Asam underscored financial discipline: “We closed 2025 on a high note, delivering strong operating profit and free cash flow ahead of our expectations.” Full-year free cash flow hit €8.24 billion, up 95%, with more predictable revenue at 86%. SAP launched a €10 billion share repurchase through 2027, starting February, following a completed €5 billion program. Operating expenses should grow at 80-90% of revenue pace in 2027.

AI remains a cornerstone. Around 60% of customers use SAP’s AI features, 20% in implementation. Partnerships like Snowflake for AI Data Cloud and France’s Bleu, Capgemini, Mistral AI bolster the EU AI Cloud for sovereign needs. Klein told Diginomica, more customers seek “real business value from AI” via embedded agents in processes with rich data context, not generic models. Deals increasingly span multiple lines, with two-thirds over €1 million involving four or more.

Strategic Pivot Amid AI and Geopolitical Pressures

SAP’s cloud shift accelerates: subscription revenue up 22% to €21.33 billion yearly, licenses down 29% to €0.99 billion. Support revenue decline will quicken as on-premise ends by 2027, extended maintenance by 2030. Cloud now 84% of Q4 revenue, up 3 points. Regional strength spanned Canada, Brazil, Germany, India, Italy, Spain, U.K., South Korea, Australia, Japan, Mexico, Saudi Arabia, Singapore, and U.S., per Morningstar.

Asam tackled AI disruption fears: “What is clear is that one of the killer applications of AI is to completely transform the way companies develop code… So there is the question, will the customers now not be able to do everything themselves, and that means the pie will shrink?” SAP counters with 35,000 developers prioritizing AI R&D for scale advantages. Citi analysts, via Morningstar, affirmed fundamentals remain “intact” despite subdued sentiment.

Full-year 2025 non-IFRS operating profit rose 28% to €10.42 billion, EPS up 36% to €6.15. Q4 gross profit (non-IFRS cloud) climbed 27% at constant currencies to €4.19 billion. Yahoo Finance noted resilient cloud demand, with Q4 cloud revenue topping consensus at €5.6 billion versus €5.5 billion expected.

Market Echoes Broader Enterprise Software Anxieties

The selloff reflects wider jitters over legacy providers in the AI era, where in-house tools might erode demand. Yet SAP’s 23% full-year cloud growth outpaces peers, backlog record underscores visibility—85% of 2026 revenue booked post-Q4 in prior cycles. Seeking Alpha flagged the backlog miss but highlighted full-year beats. Reuters reported shares set for the biggest drop since 2020, wiping $150 billion from peaks.

Geopolitics looms large: sovereign clouds for data control lengthen cycles in public sectors. Asam noted “meaningfully less” deceleration than 2025’s trend. Klein’s October comment that 25% backlog would disappoint set high expectations, unmet at 25%. Still, pipeline health supports acceleration ambitions.

For insiders, SAP’s execution—AI penetration, mega-deals, cash generation—positions it for rebound if backlog stabilizes. The €10 billion buyback signals confidence, potentially cushioning valuation at 22-25x forward multiples amid 23%+ cloud growth. As Yahoo Finance observed, cloud demand holds firm despite macro cooling.