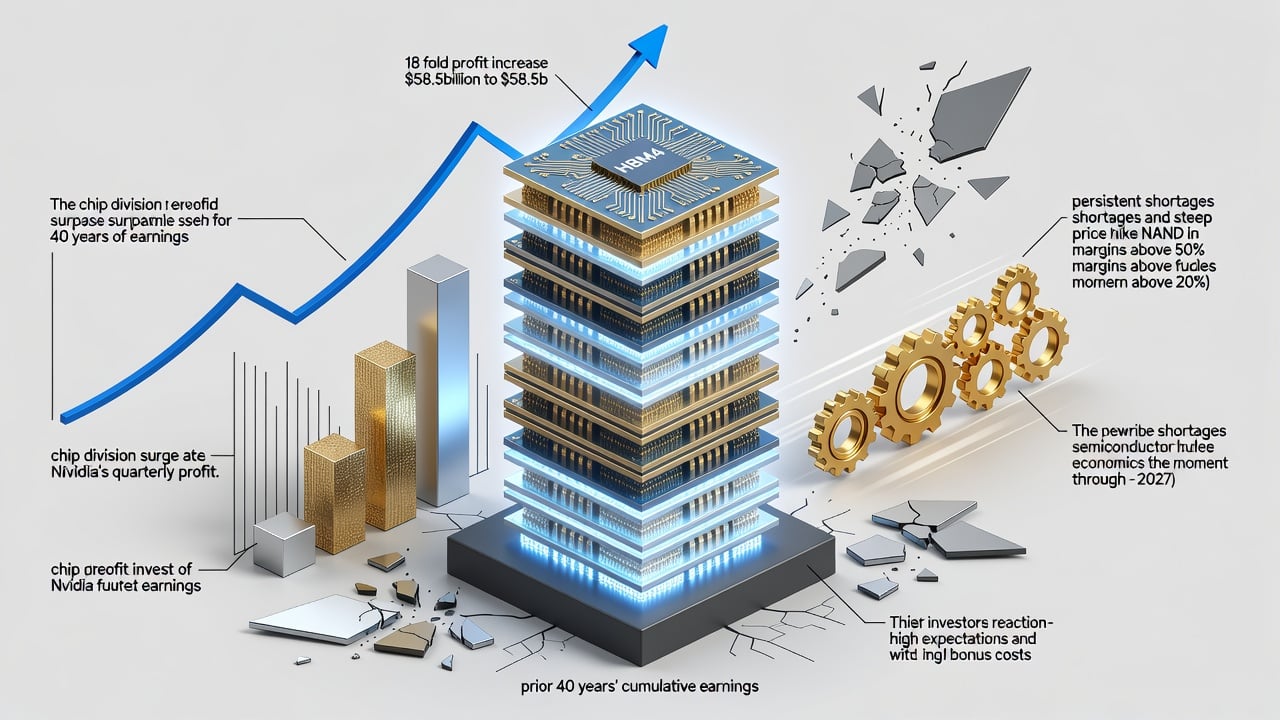

Samsung Electronics just delivered numbers that defy recent history. Its second-quarter operating profit hit a record 89.4 trillion won, or about $58.5 billion. That marks an 18-fold jump from a year earlier. The semiconductor division alone generated more money in 2026 than in the previous 40 years combined.

But the stock fell anyway. Investors, conditioned by triple-digit gains in AI plays, wanted more. They got a preview of what memory scarcity really means. And the picture is stark.

AI Servers Devour Bandwidth

High-bandwidth memory sits at the center. Hyperscalers can’t build inference clusters fast enough. Each new generation of large language models demands faster data movement between processors and memory. Traditional DRAM no longer cuts it. HBM stacks multiple DRAM dies with a logic base. They deliver terabytes per second of bandwidth.

Samsung shipped its first commercial HBM4 in February 2026. The part runs at a consistent 11.7 Gbps. Peak speeds hit 13 Gbps. Bandwidth per stack reaches 3.3 TB/s. That’s 2.7 times better than HBM3E. Customers reserved supply years out. Supply remains tight through at least 2027. (Tom’s Hardware)

Prices followed. Contract DRAM rose 44 percent in the second quarter. NAND jumped 53 percent. NAND operating margins climbed into the 40 to 50 percent range during the first half. A 12 GB LPDDR5X module now fetches around $145. Samsung is already negotiating further increases for commodity DRAM in the third quarter. (Reuters)

The memory business used to swing wildly with PC and smartphone cycles. Oversupply crushed margins for years. This time feels different. AI workloads consume memory even during inference. Data centers keep adding capacity. Brokerages now forecast Samsung’s full-year 2026 operating profit near 300 trillion won. That single-year figure exceeds the chip division’s cumulative earnings from 1985 through 2025. (Tom’s Hardware)

SK Hynix still leads in HBM market share. It supplies the bulk of Nvidia’s current needs. Samsung entered the HBM3 and HBM3E markets later. Volume suffered. Yet the company has narrowed the gap. HBM revenue grew more than 50 percent sequentially in the second quarter. Executives expect sales to double every quarter through the second half. Full-year HBM volume should rise fourfold. It doubles again in 2027. (The Information)

But execution matters. Samsung’s early HBM products faced thermal and yield issues. Stacking 12 layers without excessive heat or defects isn’t trivial. The company invested heavily in advanced packaging and test capacity. Production bases in Korea are expanding. Those capital expenditures will rise sharply again this year.

Foundry results tell another story. Samsung’s contract manufacturing arm still lags TSMC in yield on leading-edge nodes. Market share hovers around 7 to 8 percent. Some analysts see a path to 15-20 percent if hyperscalers diversify supply. Yet logic chips remain secondary to memory profits right now. The memory division carried the company.

So why did shares drop after the preliminary results? Expectations had run ahead. Some brokers forecast closer to 90 trillion won. Employee bonuses clouded the picture. Chip workers receive 10.5 percent of semiconductor operating profit in stock grants. That payout could exceed 40 trillion won for the year. Timing of the expense recognition might have trimmed reported profit. Mobile margins also faced pressure. Rising memory component costs squeezed handset profitability even as average selling prices climbed. (Reuters)

Analysts brushed off the sell-off. “Samsung’s operating profit in a single quarter has exceeded the total of the past three years,” noted Mizuho’s Jordan Klein. He pegged the memory business’s implied operating margin above 80 percent after adjusting for bonuses. Revenue shortfalls likely came from phones, TVs, and displays. Not memory. Third-quarter DRAM and NAND prices look even stronger. Some forecasts point to 35-40 percent sequential NAND gains. (Yahoo Finance)

The broader market reaction rippled. Chip stocks from Micron to AMD fell several percent. Yet the underlying demand signals haven’t changed. Amazon is borrowing $25 billion for AI infrastructure. Other hyperscalers continue to raise capital expenditure guidance. Memory shortages could persist beyond 2027 if training and inference clusters scale as projected.

Samsung isn’t standing still. It shipped HBM4E samples in May. The new variant delivers more than 20 percent higher speed than initial HBM4. Bandwidth and power efficiency both improve. The company also pushes advanced DDR5 and LPDDR5X variants tailored for AI servers. High-capacity QLC SSDs round out the portfolio for storage-heavy workloads.

Competitors face the same constraints. Micron ramps its own HBM output. SK Hynix maintains its lead but can’t meet every request. Global capacity additions trail order books. That imbalance keeps pricing power with suppliers for now. Yet history warns against complacency. Memory cycles eventually turn. New fabs come online. Demand could moderate if AI model efficiency improves faster than expected or if enterprise adoption slows.

For the moment, the supercycle rolls on. Samsung’s chip division booked 53.7 trillion won in operating profit during the first quarter alone. The second quarter pushed the combined total for SK Hynix and Samsung near 150 trillion won. Nvidia’s latest quarter came in at $53.5 billion. Samsung passed it. Memory, once the volatile stepchild, now drives the industry’s highest profits.

Executives plan to reinvest aggressively. More production lines. Better yields on advanced stacks. Closer collaboration with GPU designers. The goal is clear. Capture a larger slice of the HBM pie before the next wave of capacity eases the bottleneck. Whether that succeeds will determine if 2026 marks a peak or the start of sustained dominance.

One thing is certain. The old rules no longer apply. AI changed the math. Bandwidth became the new bottleneck. And Samsung, after years of cyclical pain, finally sits at the center of the spending boom.