The retail landscape in 2024 is navigating through a period of transformation, marked by a mix of modest growth, strategic pivots, and increased competition. The latest retail sales data confirm a modest slowdown, reflecting the broader economic conditions and changing consumer behaviors that are shaping the industry. As Neil Saunders, Managing Director and Retail Analyst at GlobalData Retail, aptly summarized, “The market remains polarized with a balance of winners and losers,” highlighting the complexities facing retailers today.

Shifting Dynamics in Retail Performance

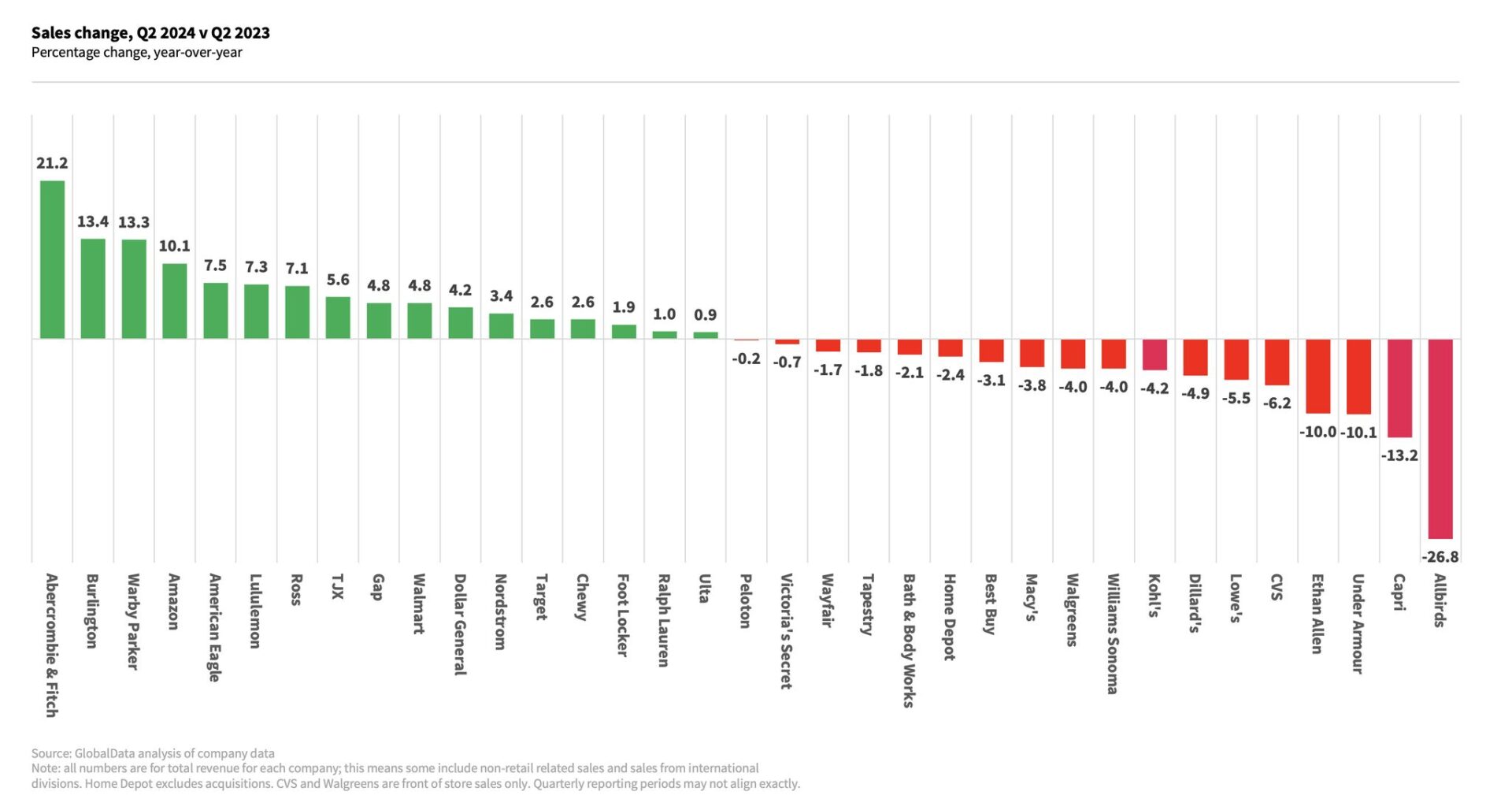

As the second quarter of 2024 comes to a close, a clearer picture of retail performance is emerging. According to Saunders, the results are akin to playing a reverse card in Uno—some retailers that had been struggling are beginning to see their declines bottom out or even move into modest growth. “Best Buy, Target, Foot Locker, Peloton, Victoria’s Secret, and Gap are examples of retailers showing signs of recovery,” Saunders notes. These companies have been implementing turnaround strategies, focusing on pricing, value, and customer experience, which are beginning to pay off.

In contrast, traditional star performers like Lululemon, Ulta, and Dollar General are experiencing a slowdown. Saunders attributes this to a mix of economic dynamics and competitive forces. “Ulta has more competition, so too does Lululemon, which failed to inspire with its womenswear in Q2,” he explains. The competitive landscape has intensified, and retailers that were once market leaders are now facing challenges in maintaining their growth momentum.

The Role of Economic Factors

Economic conditions are undeniably playing a significant role in the current retail environment. High interest rates are impacting big-ticket purchases, particularly in home-related categories, which have been under significant pressure. “A sluggish housing market, combined with high interest rates, is dampening demand for home goods,” says Saunders. This trend is reflected in the performance of retailers like Dillard’s and Nordstrom, where short-term gains do not necessarily indicate long-term health. “Dillard’s reported a 4.9% decline this quarter, but when we compare their sales to 2019, they’ve actually grown by 4.4%, while Nordstrom’s growth is a mere 0.2%,” Saunders points out, emphasizing the importance of a long-term perspective.

Inflation, which had previously bolstered retail growth by inflating sales numbers, is no longer providing the same level of support. Retailers like Dollar General are finding it increasingly difficult to maintain growth as inflation’s impact wanes and competition intensifies. “Dollar General blames weaker numbers on pressures on its customers, but this has been true for a long time. The issue now is that inflation is not flattering growth as much, and there is more price competition in grocery,” Saunders explains. The pressures on consumers, particularly those in lower-income brackets, are becoming more pronounced, leading to shifts in spending behavior.

Competitive Pressures and Strategic Missteps

Increased competition is another critical factor contributing to the slowdown in retail sales. Saunders notes that “some of the traditional star performers are struggling to keep up the fast pace,” as they face stiffer competition and changing consumer preferences. Lululemon’s struggles with its womenswear line in Q2 serve as a case in point. The brand, which had previously been a market leader, is now facing challenges in maintaining its appeal amid a crowded market.

Retailers are also grappling with the consequences of strategic missteps. As Saunders warns, “Don’t always buy the narratives retailers spin.” For instance, while some retailers may blame external factors like economic pressures or changing consumer behavior for their poor performance, the reality is often more complex. “Some stores are terrible and are preventing sales and repeat visits,” Saunders states bluntly, pointing to operational inefficiencies and poor customer experiences as significant factors behind declining sales.

Long-Term Outlook and Sector-Specific Trends

Despite the current challenges, the long-term outlook for retail remains mixed, with some sectors poised for growth while others continue to struggle. Home-related categories, for instance, are likely to remain under pressure as long as the housing market stays sluggish and interest rates remain high. “Moving is an important driver of demand, and with the housing market slowing down, we’re seeing a corresponding decline in sales for home goods,” Saunders explains.

On the other hand, sectors like electronics and groceries are showing more resilience. “Retail sales showed robust performance in sectors such as electronics and groceries, with increases of 1.6% and 1% respectively in July 2024,” according to recent data. These categories are benefiting from steady consumer demand, although the overall growth rate has modestly deteriorated since Q1.

Saunders also highlights the polarization within the market, where a balance of winners and losers persists. Out of a selection of retailers analyzed, 17 are in growth, while 18 are in decline. “Growth rates have generally deteriorated since Q1, with 21 retailers showing lower growth rates than in Q1, while only 14 have higher growth rates,” Saunders notes. The average overall growth rate has dropped by a modest 0.5 percentage points since Q1, indicating that while the market is not in recession, there is a clear slowdown.

Strategic Responses to a Changing Market

Retailers are responding to these challenges in various ways, with some investing in digital transformation and e-commerce strategies to stay competitive. Phil Masiello, CEO of CrunchGrowth, suggests that “Retailers who have successfully integrated online and offline experiences are likely to see more resilient performance.” Masiello emphasizes the importance of omnichannel capabilities, personalized customer experiences, and data analytics in navigating the current retail landscape. “Sustainability and ethical practices are also becoming increasingly important to consumers, and retailers who prioritize these aspects could gain a competitive edge in the long run,” he adds.

The retail sector in 2024 is facing a complex and challenging environment. While there is no immediate sign of a recession, the modest slowdown in sales reflects broader economic conditions and intensified competition. Retailers must stay agile, focusing on long-term strategies that prioritize customer experience, operational efficiency, and innovation to navigate the fluctuations in the market successfully. As Saunders advises, “The long-term picture remains vital because quarterly results fluctuate and create noise,” underscoring the need for a strategic approach to ensure sustained growth in an increasingly competitive landscape.