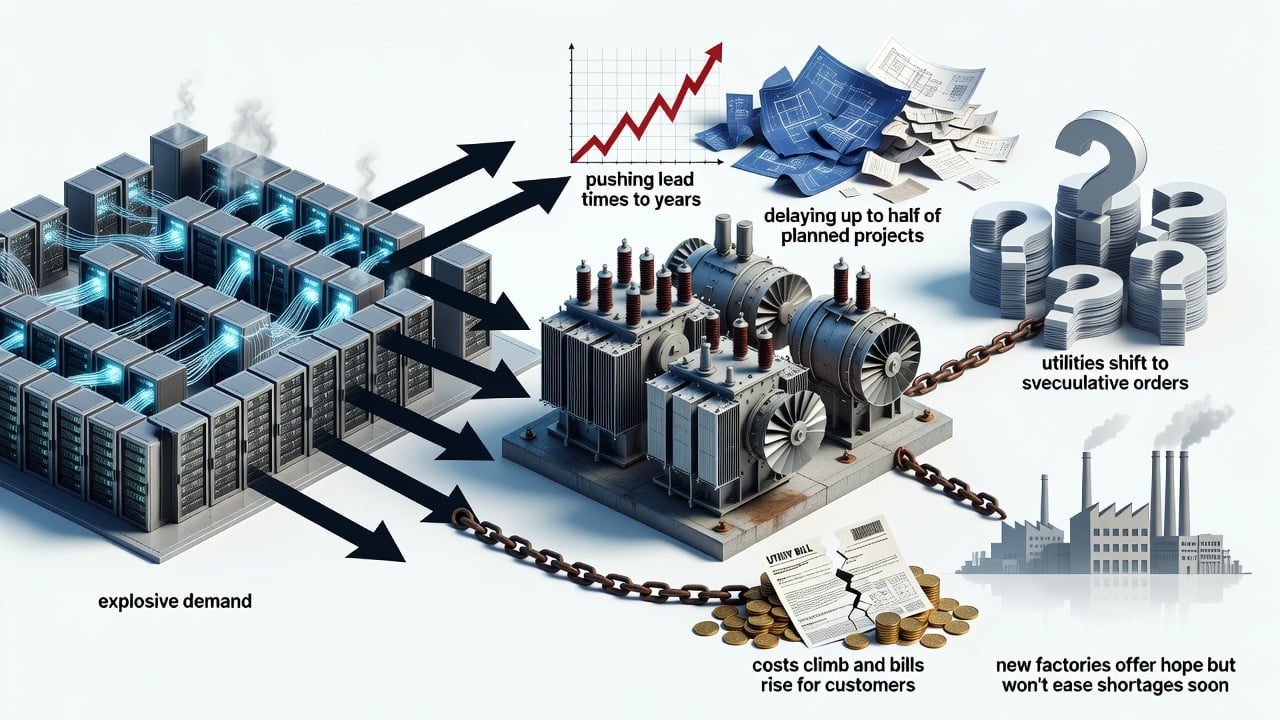

US power companies find themselves in a frantic contest for essential gear. Surging needs from AI data centers have stretched supplies of transformers, turbines and switchgear to the breaking point. Lead times once counted in months now stretch into years. Factories sit fully booked. Developers lock in orders far ahead of any shovel hitting dirt.

Shortages hit hardest with large power transformers. These hulking substation units step voltage up or down across the network. Average US lead times now hover near 128 weeks, according to The Next Web. Some of the largest models face waits of three to five years, up from 24 to 30 months before the boom. Generator step-up transformer queues surpassed 160 weeks in the first quarter of 2026. That compares with an average of 143 weeks in 2024. High-voltage circuit breakers climbed to 125 weeks in the second half of last year from 77 weeks in 2023.

Ben Boucher, senior analyst at Wood Mackenzie, calls the shift stark. “Equipment availability is becoming the biggest concern for developers as they value time to market so highly,” he told Reuters in a report published today. Data center construction also drives demand for circuit breakers and switchgear. Those categories face even larger market deficits ahead.

And the numbers keep climbing. Demand for generator step-up transformers jumped 274 percent between 2019 and 2025. Substation transformer demand rose 116 percent over the same span. US spending on data center electrical equipment could surge from $20 billion in 2025 to $65 billion by 2030. Data center capacity itself is forecast to reach 110 gigawatts in 2030 from about 24 gigawatts now. That load will consume eight times more electricity than electric vehicles over the period, per Wood Mackenzie analysis cited by Reuters.

Prices follow the pressure. Transformer costs may rise 4 percent to as much as 10 percent over the next year, depending on type. Up to half of planned US data center projects have slipped or been canceled. Many cannot secure the necessary hardware or grid connections fast enough.

Utilities rewrite old playbooks under the strain.

They once bought just in time. Now many place speculative orders and pay to reserve factory slots years before projects win approval. Some bid on equipment five years out. California’s Roseville Electric Utility provides one example. Its CEO Dan Beans described a shift from one-year timelines to three-year waits, prompting purchases for projects still half a decade away. Others refurbish older transformers or prepay suppliers. Smaller cooperatives feel the pinch most. Long-term supply agreements help larger players but “don’t solve everything, particularly for smaller utilities that don’t have the scale,” said Louis Finkel, senior vice president of government relations at the National Rural Electric Cooperative Association, in the Reuters report.

Developers diversify sources. They court multiple suppliers across geographies. Miska Pukkila, senior manager of strategic sourcing at Wärtsilä Energy Storage, noted the trend toward long-term agreements and broader sourcing. Imports rise. China remains a key supplier for certain components despite trade tensions. The reliance adds geopolitical risk to an already fragile chain.

But the upstream constraints run deep. Transformers require grain-oriented electrical steel and specialized labor. Both stay scarce. Production cannot ramp quickly enough even as orders flood in. GE Vernova’s gas-turbine backlog reached 100 gigawatts in the first quarter of 2026. The company expects at least 110 gigawatts by year-end. Some frames sell into the next decade. Siemens Energy carries a record order backlog of roughly €136 billion. Rivals including Mitsubishi hold books stretched about five years.

Regulators notice the logjam. The Federal Energy Regulatory Commission has pushed grid operators to overhaul rules and fast-track data center connections. Last month it ordered reviews of new protocols for quicker hookups. Yet a faster queue cannot manufacture a transformer. Underlying shortages of hardware and new generation capacity persist.

The mismatch lands on customer bills. Utilities near major data center hubs warn of higher rates. Connection queues in several markets now exceed four years. Scarcity inflates equipment prices along with delays. Households and businesses foot the bill while hyperscalers race to build.

Manufacturers respond with fresh investment. Hitachi Energy pledged more than $1 billion to US production, including a new plant in South Boston, Virginia, slated for 2028. Siemens expands transformer manufacturing in North Carolina. New facilities still take years to build, permit and certify. Few expect meaningful relief before the end of the decade.

Recent analysis reinforces the picture. Goldman Sachs projected US data center power demand will climb from 31 gigawatts in 2025 to 41 gigawatts in 2026 and 66 gigawatts in 2027. Only 50 to 60 percent of scheduled capacity for the next one to two years may come online on time amid delays and cancellations. Supply chain and labor shortages rank among the top causes.

Bloomberg reported in April that more than half the US data centers planned for 2026 face delays or cancellation. The piece highlighted heavy dependence on hard-to-find electrical equipment and creative sourcing, including from overseas. A separate Bloomberg feature detailed how the AI build-out relies on Chinese electrical equipment imports, adding another layer of complexity to supply chains already under stress.

Grid Strategies LLC documented enormous load growth in regions like Texas, where Oncor alone received 103 gigawatts of new load requests including 82 gigawatts from data centers. PJM, the nation’s largest grid operator, has flagged unprecedented data center growth that could exhaust remnant transmission capacity and create reliability risks. The operator now eyes extra-high voltage reinforcements with long lead times.

The pattern repeats. Data centers no longer compete just for chips or land. They battle for electrons and the metal that delivers them. Securing a transformer slot now sits as central to an AI project as the GPUs inside the racks. Utilities scramble. Manufacturers expand where they can. Regulators tweak rules. Yet the hardware gap remains. And it will shape how fast the AI economy can scale for years ahead.