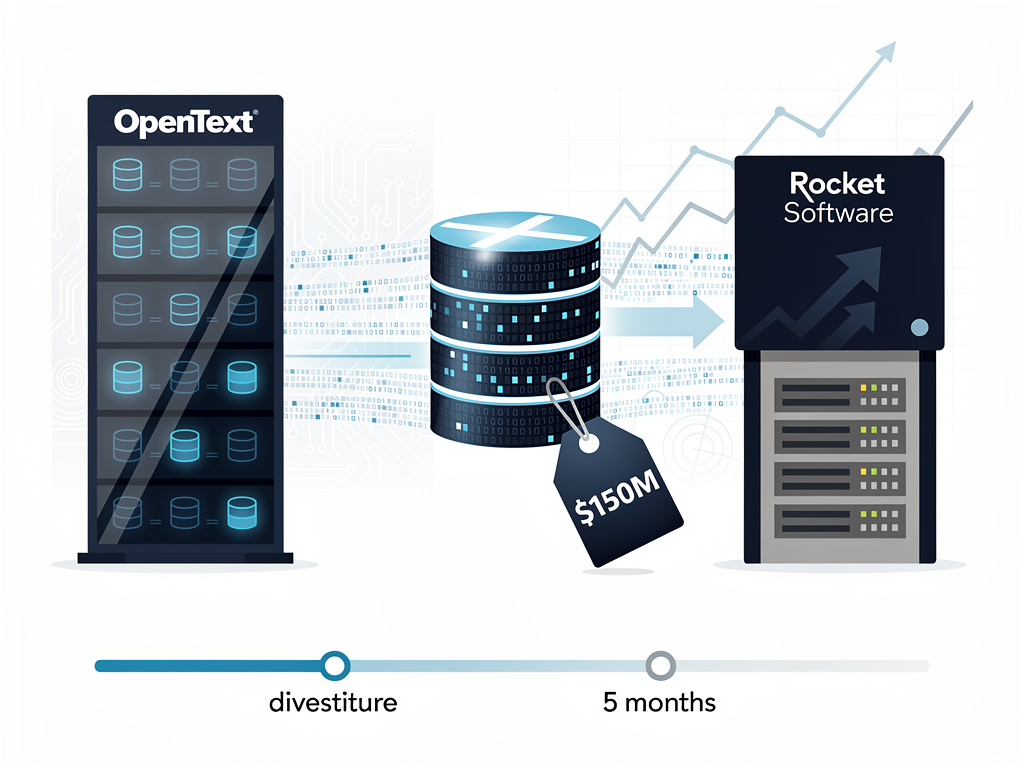

OpenText Corporation, the Canadian enterprise information management giant, has executed its second major divestiture in less than half a year, offloading its analytics database business Vertica to Rocket Software for $150 million. The transaction, announced in early 2025, represents a calculated move by the Waterloo-based software company to pare down its substantial debt load accumulated through years of aggressive acquisitions. According to BetaKit, this sale follows a pattern of strategic asset liquidation as OpenText confronts the financial realities of its expansion-focused business model.

The sale price of $150 million marks a significant discount from OpenText’s original 2018 acquisition of Vertica from Micro Focus for $350 million, reflecting both the challenging market conditions for analytics platforms and the urgency of OpenText’s debt reduction strategy. PR Newswire reported that the transaction is expected to close in OpenText’s fiscal fourth quarter of 2025, subject to customary closing conditions and regulatory approvals. The proceeds will be directed entirely toward reducing OpenText’s outstanding debt obligations, which have become increasingly burdensome as interest rates have remained elevated and enterprise software spending has softened.

A Pattern of Portfolio Pruning Emerges

This divestiture follows OpenText’s sale of its AMC business unit just months earlier, establishing a clear pattern of portfolio rationalization under CEO Mark Barrenechea’s leadership. The company’s willingness to divest businesses at substantial losses compared to acquisition prices signals a fundamental shift in strategy from growth-at-all-costs to financial stability and operational efficiency. Industry observers note that OpenText’s debt burden, accumulated through dozens of acquisitions over the past decade, has reached levels that constrain the company’s strategic flexibility and ability to invest in organic innovation.

Vertica, originally developed by database pioneer Michael Stonebraker and his team at MIT, was once considered a cutting-edge columnar analytics database that competed directly with offerings from Oracle, Teradata, and later cloud-native solutions like Snowflake and Databricks. The platform’s ability to handle massive datasets with high-performance analytics made it attractive to telecommunications companies, financial services firms, and other data-intensive enterprises. However, the rapid shift toward cloud-based data warehousing and the emergence of more flexible, scalable alternatives has eroded Vertica’s competitive position in recent years.

Rocket Software’s Strategic Acquisition Rationale

For Rocket Software, the Vertica acquisition represents a strategic addition to its portfolio of enterprise infrastructure software, which includes mainframe solutions, business process automation tools, and data management platforms. The Boston-based software company, backed by private equity firm Bain Capital, has built its business model around acquiring mature enterprise software products and optimizing them for sustained profitability. Rocket’s approach typically involves maintaining and enhancing legacy systems that remain critical to large organizations while extracting value from established customer relationships.

The $150 million price tag suggests Rocket Software sees opportunity in Vertica’s existing customer base and the potential to integrate the analytics database with its broader product portfolio. The Canadian Press News noted that the transaction includes Vertica’s technology, customer contracts, and associated intellectual property, providing Rocket with immediate revenue streams and cross-selling opportunities across its existing enterprise customer base.

The Debt Burden Driving Divestiture Decisions

OpenText’s debt situation has become increasingly pressing as the company grapples with the financial consequences of its acquisition-driven growth strategy. Over the past fifteen years, OpenText has completed more than 100 acquisitions, transforming itself from a document management specialist into a sprawling enterprise information management conglomerate. This aggressive expansion required substantial borrowing, and the company’s debt-to-equity ratio has climbed to levels that concern investors and credit rating agencies alike.

The elevated interest rate environment of 2023 and 2024 has made this debt particularly expensive to service, diverting cash flow that might otherwise fund product development, sales expansion, or shareholder returns. By divesting non-core assets like Vertica, OpenText aims to reduce its debt burden while focusing resources on higher-margin, more strategic business units. The company’s management has indicated that further portfolio optimization may be forthcoming as it seeks to achieve more sustainable financial ratios and improved operational efficiency.

Market Dynamics in Enterprise Analytics

The sale of Vertica occurs against a backdrop of dramatic transformation in the enterprise analytics and data warehousing market. Cloud-native platforms such as Snowflake, Google BigQuery, Amazon Redshift, and Microsoft Azure Synapse Analytics have fundamentally altered customer expectations around scalability, pricing models, and ease of deployment. These newer solutions offer elastic compute resources, separation of storage and compute, and pay-as-you-go pricing that traditional on-premises databases struggle to match.

Vertica’s columnar storage architecture and massively parallel processing capabilities were revolutionary when first introduced, but the platform’s on-premises heritage has become a liability in an era when enterprises increasingly prefer cloud-first or cloud-only solutions. While Vertica did develop cloud deployment options, it faced intense competition from vendors that built their architectures specifically for cloud environments from the ground up. This competitive pressure likely contributed to OpenText’s decision that Vertica no longer fit its strategic priorities.

Implications for OpenText’s Future Direction

The dual divestitures within a five-month span suggest OpenText is entering a new phase of corporate evolution, one focused on consolidation rather than expansion. After years of being a serial acquirer in the enterprise software sector, the company appears to be acknowledging that not all acquisitions delivered the expected synergies or strategic value. This recalibration may ultimately benefit OpenText by allowing management to concentrate resources on core competencies in content services, business network operations, and information governance.

Investors and industry analysts will be watching closely to see whether additional asset sales follow, and which business units OpenText considers essential to its long-term strategy. The company’s stock performance and credit ratings will likely depend on management’s ability to execute this portfolio rationalization while maintaining revenue stability and demonstrating a clear path to organic growth. The success of this strategy will also hinge on whether OpenText can use the proceeds from asset sales to meaningfully reduce debt while avoiding the sale of businesses at fire-sale prices.

Broader Industry Trends in Software M&A

OpenText’s situation reflects broader trends in the enterprise software industry, where companies that pursued aggressive acquisition strategies during the low-interest-rate era now face pressure to rationalize portfolios and improve financial efficiency. Many software companies expanded rapidly through debt-financed acquisitions when borrowing costs were minimal, assuming that revenue growth and market consolidation would justify the leverage. However, the combination of rising interest rates, economic uncertainty, and more cautious enterprise IT spending has forced a reckoning.

The private equity-backed model exemplified by Rocket Software—acquiring mature software assets and optimizing them for cash generation—has become increasingly prevalent as larger software companies divest non-core businesses. This creates a secondary market for enterprise software products that may no longer fit their original owners’ strategies but retain value through established customer bases and recurring revenue streams. The Vertica transaction fits squarely within this pattern, representing a transfer of ownership from a growth-oriented conglomerate to a financial buyer focused on operational optimization.

Customer and Partner Considerations

For Vertica’s existing customers, the ownership change introduces both uncertainty and potential opportunity. On one hand, transitions between software vendors can create disruption, raise questions about product roadmaps, and complicate support relationships. Customers who selected Vertica as part of a broader OpenText ecosystem may need to reassess their analytics strategies and vendor relationships. On the other hand, Rocket Software’s focus on enterprise infrastructure and its track record of maintaining and enhancing acquired products could provide stability and renewed investment in the Vertica platform.

The technology partners and systems integrators that have built practices around Vertica will also need to adapt to the new ownership structure. Rocket Software’s approach to partner ecosystems and its commitment to maintaining Vertica’s competitive capabilities will significantly influence whether these partnerships continue to thrive or gradually diminish. The coming months will be critical as Rocket communicates its vision for Vertica and demonstrates its commitment to the product’s evolution and market position.

As OpenText continues its debt reduction campaign and portfolio optimization, the Vertica sale stands as a clear marker of the company’s strategic pivot. Whether this approach ultimately strengthens OpenText’s competitive position or signals deeper challenges will depend on execution, market conditions, and the company’s ability to articulate a compelling vision for its post-divestiture future. For now, the transaction represents a pragmatic response to financial pressures and a recognition that not every acquisition in a serial acquirer’s history deserves permanent placement in the portfolio.