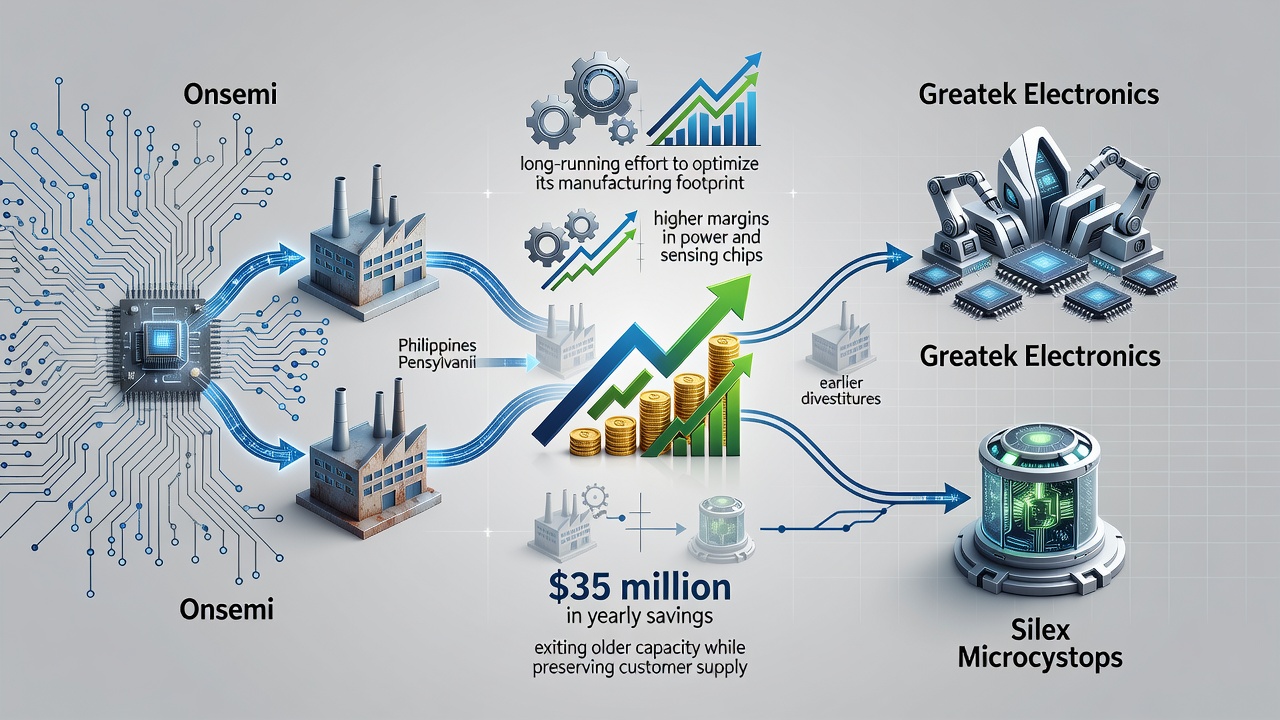

Onsemi is exiting two wafer fabs. The chipmaker signed deals to sell its plant in Tarlac, Philippines, to Taiwan’s Greatek Electronics and its Mountain Top, Pennsylvania, facility to Sweden’s Silex Microsystems. No price tags were disclosed. The moves form the latest step in a years-long effort to slim its manufacturing base.

Shares of the Scottsdale, Arizona-based company fell more than 3% in premarket trading Tuesday. They have still climbed nearly 75% so far this year. Onsemi makes power and sensing chips. Those parts end up in electric vehicles, automated factories and the servers that power AI data centers.

The sales align with what Onsemi calls its Fab Right strategy. The approach aims to cut costs. It improves efficiency. It focuses capital on the operations that deliver the highest returns. Both sites will keep producing during the handover. A long-term supply pact with Greatek will protect customer shipments after the Philippine deal closes.

The transactions are expected to deliver about $35 million in annual savings. Initial benefits arrive in 2027. The full run-rate hits in 2028. The Tarlac deal should close in three to six months, subject to regulatory approvals. The Mountain Top transaction wraps in January 2028. That extra time lets Onsemi shift output elsewhere.

Pattern of Portfolio Pruning

This isn’t Onsemi’s first divestiture. The company has shed older trailing-edge assets for years. Back in 2022 it sold a fab in Pocatello, Idaho, to LA Semiconductor. It also divested facilities in South Portland, Maine, and Oudenaarde, Belgium. Those three deals came within a 12-month window. An industry broker called ATREG handled the Pocatello transaction.

“In addition to our South Portland, Maine and our Oudenaarde, Belgium fabs, this is the third manufacturing asset disposition that ATREG has helped us with over the past 12 months,” said the executive vice president of global manufacturing and operations at the time. “This divestment is a continuation of onsemi’s fab-liter manufacturing strategy aimed at achieving a sustainable financial performance through upscaling capacity for products in our key markets of automotive and industrial.”

The language has evolved. Onsemi now brands the effort Fab Right. The goal stays consistent. Shed low-margin, older capacity. Scale up in silicon carbide and other high-growth areas. Keep supplying customers through foundry partnerships and long-term agreements. The pattern shows a company determined to avoid the heavy capital demands of running every fab itself.

Investors have watched similar moves across the sector. Chipmakers face relentless pressure to improve margins even as demand for power semiconductors surges with the rise of EVs and data-center cooling systems. Onsemi’s power chips help manage electricity in these applications. Yet older 200-millimeter fabs can drag on profitability when utilization slips or when newer competitors bring larger wafers online.

The latest sales target exactly those kinds of sites. Mountain Top and Tarlac represent legacy capacity. Transferring them to specialized buyers like Greatek, which focuses on packaging and testing, and Silex, a pure-play foundry, lets Onsemi exit without stranding output. Customers keep their parts. Onsemi keeps its gross margin trajectory pointed upward. Simple as that.

But the stock reaction Tuesday reminds how markets parse these announcements. Initial skepticism often greets divestitures. The 3% premarket drop reflected uncertainty over execution timelines and any one-time charges that might hit near-term earnings. Longer term the savings and sharper focus tend to win out. Onsemi’s own history bears that out. Previous sales contributed to a more streamlined operation and better returns on invested capital.

Recent coverage echoes the details. Reuters reported the exact buyers, timelines and $35 million savings figure within hours of the announcement. StreetInsider highlighted the long-term supply agreements and the three-to-six-month close for the Philippine asset. Finimize noted the streamlining effort in a shorter dispatch published Monday.

Broader industry context adds weight. Semiconductor demand remains strong in automotive and industrial segments despite cyclical softness elsewhere. Onsemi’s silicon carbide platform has won design slots at major EV makers. Scaling that business requires capital. Every dollar tied up in underutilized older fabs is a dollar not spent on SiC capacity or advanced packaging. The math is straightforward.

So the company keeps pruning. Four fab sales since the start of the decade. A clear preference for asset-light manufacturing in non-core areas. Partnerships with foundries and OSATs fill the gaps. The strategy isn’t flashy. It works.

Executives have avoided dramatic language in public statements. They talk about optimization, not transformation. They emphasize continuity for customers rather than disruption. That measured tone matches the methodical pace of the divestitures. One plant at a time. Measured savings. Predictable margin expansion.

Still, questions linger. How quickly can production shift from Mountain Top without hiccups? Will Greatek maintain the quality standards Onsemi’s automotive customers demand? The long-term supply deal offers some protection. The 18-month window for the Pennsylvania transition gives breathing room. Execution will decide whether the $35 million target lands cleanly.

Analysts following the stock have generally viewed the portfolio adjustments positively. They see a firm sharpening its edge in high-voltage power devices at a time when data centers and EVs consume ever more electricity. Onsemi’s sensing portfolio adds another growth vector. The fabs now on the block contributed less to that future.

The sales also reflect a maturing view of global supply chains. Onsemi once operated a sprawling network of 19 manufacturing sites. It has steadily reduced that footprint. The remaining assets focus on differentiated processes. Silicon carbide epitaxy and fabrication sit at the core. Older silicon lines move to partners better equipped to run them at scale.

Nothing groundbreaking here. Just a semiconductor company behaving like one that has learned from past cycles. Build what you must. Sell what you don’t. Keep margins headed north. Onsemi’s latest transactions follow that playbook to the letter. The market may need a day or two to digest the news. The strategic direction has been clear for some time.

And the savings will compound. Thirty-five million dollars a year adds up when reinvested in the technologies that actually move the needle. For an industry obsessed with the next big node, Onsemi’s approach looks almost old-fashioned. Focus. Efficiency. Sustainable performance. Those words may not spark headlines. They do improve returns.