Tom Baker sees trouble ahead. The managing director for Bahrain at Vitol Group, one of the world’s largest commodity trading houses, told an industry conference that the oil market is underpricing risks tied to the Iran war. His remarks, delivered June 2 at the S&P Global Energy Middle East Petroleum and Gas Conference in London, cut against the recent calm in crude prices.

Iran’s effective closure of the Strait of Hormuz combined with attacks on energy infrastructure. Oilfields and refineries went offline. Some 14 million barrels per day of Middle East supply disappeared. That represents the largest oil supply crisis in history. Reuters first reported Baker’s comments.

“Crude can come back online, but from a product perspective, it might be very hard for the system to catch up for the rest of the year,” Baker said. Short sentences. Stark warnings. The physical market tells a different story than futures curves suggest.

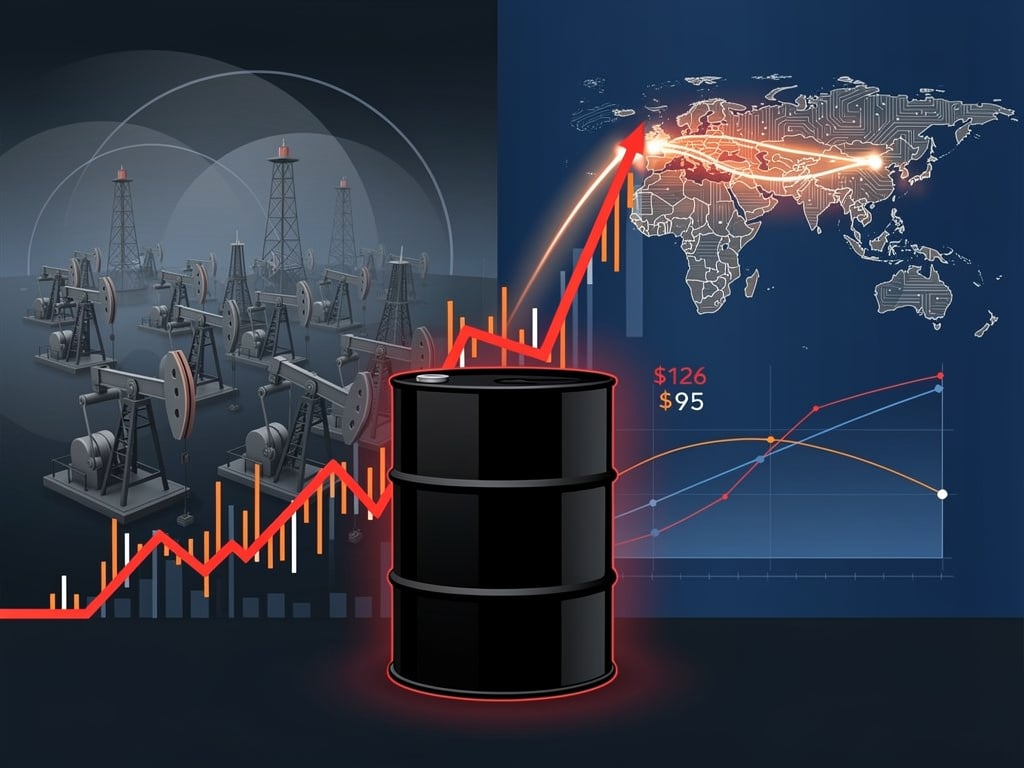

Prices spiked hard at first. Brent and WTI contracts climbed as high as $126 a barrel when the conflict intensified and the strait closed. They have since eased. Crude stood around $95 on the day of Baker’s speech. Yet that retreat masks deeper strains. Inventories cannot be drawn down forever. China cannot skip importing 5 million barrels per day indefinitely.

“The turning point could be when someone really needs those physical molecules and the physical molecules just aren’t there to buy,” Baker added. And at that moment the price needs to go higher. The only resolution then becomes demand destruction. Consumers forced to cut back because costs climb too far. Baker noted such destruction looks unlikely if prices slip toward $90.

His assessment arrives as the futures market shows clear backwardation. Near-term contracts trade at a sharp premium to later 2026 deliveries. CME Group analysts have examined whether this structure signals fading supply worries or an underpricing of persistent risk amid ongoing Middle East conflict. The CME analysis highlights the front-end strength tied directly to regional tensions.

Recent coverage reinforces the pattern. Geopolitical risk, not current supply-demand balances, has driven much of the price action this year. StoneX noted in January that escalation fears around the Strait of Hormuz amplified volatility and embedded a near-term risk premium. Markets focused on worst-case scenarios even as fundamentals appeared stable.

Broader research points to lasting effects. A study published this year examined oil price reactions to Middle East escalations in 2025 and 2026. It found measurable changes in pricing behavior tied to those shocks. The MDPI paper provides evidence from the recent wave of tensions.

Analysts at Franklin Templeton warned in April that energy markets show signs of complacency. They may structurally underprice the duration of geopolitical risk. The shock extends beyond crude into power markets and cross-industry cost pressures. Their analysis argued that investors underestimate how long disruptions could last.

Yet the response has often felt contained. Oil surged. Bond yields adjusted. Equity markets absorbed the blow. Aswath Damodaran observed in March that the price of risk rose only modestly despite war headlines, oil spikes, and uncertainty. Markets acknowledged the disturbance. They stopped short of treating it as a structural break. His substack post captured the muted equity risk premium reaction.

Other voices sounded alarms earlier. Bloomberg reported in March that markets were underpricing the commodity shock from interrupted flows through the Strait of Hormuz. Interest rates looked too low given the potential fallout. The piece highlighted how quickly the situation could widen.

Reuters itself documented multiple flare-ups. Simultaneous geopolitical events in Venezuela, Iran, and the Black Sea pushed prices to three-month highs in January while a supply glut still loomed. Traders wrestled with that tension. The dispatch captured the treacherous environment for investors.

By spring the risks had intensified. Aspiriant advisors noted in March that rising Middle East tensions lifted oil and forced a rethink of inflation and growth outlooks. Historical patterns suggested every 10 percent oil increase trims global growth by 0.1 percent while adding 0.2 percent to inflation. Severe disruption could push crude above $125 and deliver a full percentage point drag on output. Their quick take outlined the transmission channels.

Kitces.com reviewed 10 charts addressing 2026 geopolitical concerns in April. Oil prices had climbed on supply disruptions. Brent held above $110 in recent weeks at that time. The futures curve remained in backwardation. Investors debated whether the spike would fade or signal a sustained shock. The analysis tied energy costs directly to inflation expectations and central bank decisions.

Morgan Stanley’s fixed income team described a sharp reset in April followed by stabilization. Geopolitical tensions drove energy higher. Oil-linked risk premia stayed embedded even as broader sentiment improved after a temporary U.S.-Iran ceasefire. Their May note tracked the partial reversal of risk-off moves.

Schwab highlighted relief after a truce in Iran but cautioned that volatility would linger. The oil futures curve steepened sharply during the conflict then moderated. Markets staged a relief rally. Energy sectors led. Yet headline risk kept swings possible. The commentary stressed that nothing had been resolved.

Baker’s warning stands out for its focus on physical realities. Traders can debate curves and premiums. The absence of actual barrels creates a harder stop. China resuming full imports. Refineries needing feedstock. Inventories hitting limits. These pressures build quietly until they don’t.

So the market sits in an uneasy spot. Prices have come off the peak. Backwardation persists. Geopolitical headlines continue. And a veteran trader at the largest independent oil merchant says the true cost of risk has not yet been paid. Physical molecules will decide the next chapter. Not spreadsheets.

Industry insiders have heard similar cautions before. This time the scale feels different. Fourteen million barrels a day. The largest crisis on record. Demand destruction as the backstop. Those numbers concentrate the mind. Especially when $95 crude still feels cheap relative to the potential gap.

Watch the inventories. Monitor Chinese import flows. Listen for signs that refiners are scrambling. The turning point Baker described arrives without much notice. Then the scramble begins. And prices move to ration what remains.