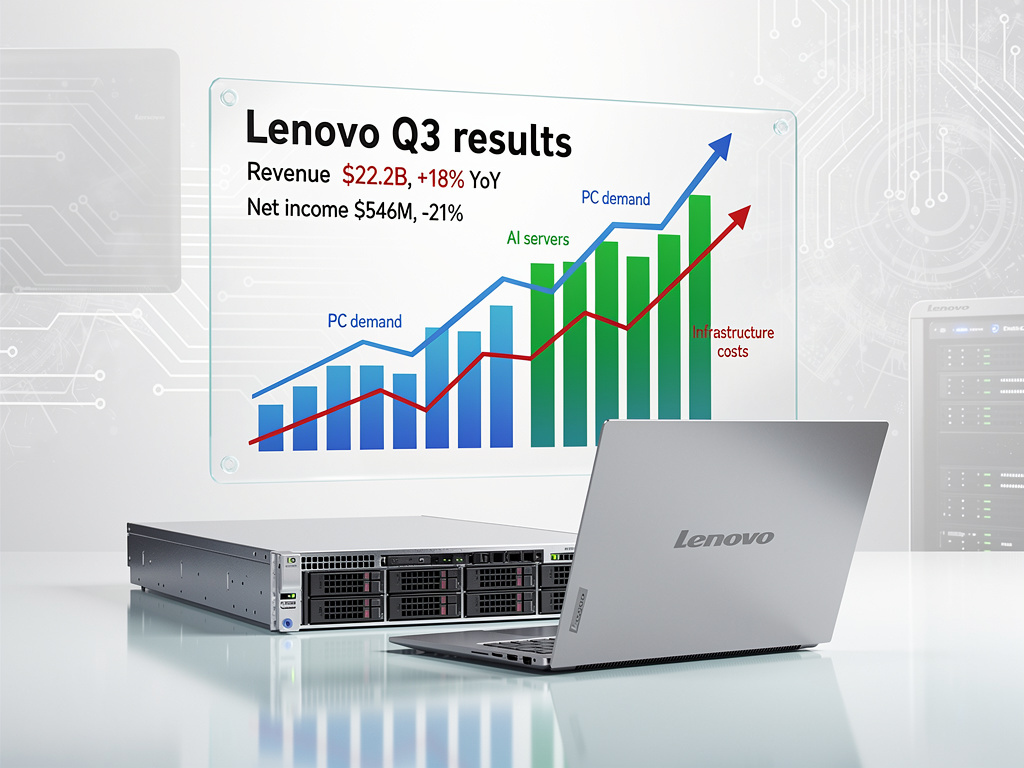

Lenovo Group Ltd., the world’s largest personal computer manufacturer, posted fiscal third-quarter revenue of $22.2 billion, an 18% year-over-year surge that underscored the powerful twin currents reshaping the technology hardware industry: an accelerating enterprise appetite for artificial intelligence infrastructure and a consumer rush to purchase PCs ahead of anticipated memory price increases. Yet beneath the top-line exuberance, profitability told a more complicated story — net income fell 21% to $546 million, a reminder that growth in the AI era comes with margin pressures that even the most diversified hardware conglomerates cannot easily sidestep.

The results, reported on February 12, 2026, for the quarter ending December 2025, beat analyst estimates on both revenue and profit, according to Reuters. The Hong Kong-listed company’s shares had already climbed more than 30% over the prior twelve months, buoyed by investor enthusiasm for its positioning in the AI server market and its diversification beyond traditional PCs. But the quarterly earnings report revealed a business in transition — one simultaneously benefiting from cyclical tailwinds in its legacy PC division and making costly bets on the infrastructure backbone of the AI revolution.

A Perfect Storm of Demand: Memory Prices and the PC Refresh Cycle

The most immediate driver of Lenovo’s revenue surge was a phenomenon familiar to anyone who has watched commodity cycles play out in the technology sector: anticipatory buying. As Bloomberg reported, customers — both enterprise and consumer — accelerated PC purchases ahead of expected memory price hikes. DRAM and NAND flash prices, which had been recovering from a deep cyclical trough throughout 2025, were projected to climb further in the first half of 2026 as memory manufacturers tightened supply and AI-related demand for high-bandwidth memory (HBM) chips siphoned capacity away from conventional memory production lines.

This pull-forward effect was particularly pronounced in Lenovo’s Intelligent Devices Group (IDG), which encompasses PCs, tablets, and smartphones. The IDG segment reported robust growth, driven by what the company described as broad-based strength across geographies and product categories. Corporate refresh cycles, many of which had been delayed during the post-pandemic normalization period, added further fuel. Organizations upgrading to Windows 11-compatible hardware and AI-capable PCs — machines equipped with neural processing units (NPUs) — provided a structural demand layer on top of the cyclical memory-driven urgency. According to Lenovo’s own press release, the company maintained its position as the global leader in PC shipments during the quarter, extending a streak that has persisted for over a decade.

The AI Infrastructure Buildout: Lenovo’s Fastest-Growing Frontier

While PCs provided the revenue volume, it was Lenovo’s Infrastructure Solutions Group (ISG) that captured Wall Street’s imagination. The ISG division, which sells servers, storage systems, and networking equipment to enterprises and hyperscale data center operators, has become the company’s most strategically important growth engine. Revenue in the segment surged as demand for AI-optimized servers — machines built around NVIDIA’s GPU accelerators and increasingly around custom AI silicon — continued to outpace supply across the industry.

Lenovo has been investing aggressively to position itself as a credible alternative to Dell Technologies and Hewlett Packard Enterprise in the AI server market. The company’s Neptune liquid cooling technology, designed to manage the extreme thermal loads generated by dense GPU clusters, has been a key differentiator. As reported by Morningstar, Lenovo maintained its revenue momentum in part because of strong order pipelines in AI infrastructure, with enterprise customers ranging from sovereign AI initiatives in the Middle East and Asia to Western financial services firms building proprietary large language model capabilities. Chairman and CEO Yuanqing Yang has repeatedly emphasized that the company’s strategy is to become an end-to-end AI solutions provider — from the edge device in a worker’s hands to the server rack in the data center.

Profit Pressures: The Cost of Playing in the AI Arena

The 21% decline in net income, however, revealed the tension at the heart of Lenovo’s transformation. Several factors weighed on profitability. First, the AI server business, while growing rapidly, operates at significantly thinner margins than the mature PC division. GPU components from NVIDIA command premium pricing and are subject to allocation constraints, leaving server assemblers like Lenovo with limited room to mark up finished systems. Second, Lenovo’s investments in research and development — particularly in AI software, services, and hybrid cloud solutions — have been ramping, adding to operating expenses. Third, the company faced higher financing costs related to its expanded debt load, a consequence of acquisitions and capital expenditures aimed at scaling its infrastructure business.

As Reuters noted, despite the profit decline, the $546 million net income figure still exceeded analyst consensus estimates, suggesting that the market had already priced in the margin compression associated with Lenovo’s business mix shift. The company’s pre-tax income margin and operating margin both came under pressure, but management signaled confidence that margins would improve as the ISG business scales and as higher-margin AI services — including consulting, deployment, and managed infrastructure offerings — become a larger share of the revenue mix. According to the Financial Post, Lenovo’s Solutions and Services Group (SSG) continued to deliver industry-leading margins, providing a partial offset to the margin dilution from hardware-heavy AI server sales.

Solutions and Services: The Margin Anchor

Lenovo’s SSG division, which provides IT managed services, device-as-a-service offerings, and increasingly AI-powered digital workplace solutions, has quietly become the company’s most profitable segment on a percentage basis. While smaller in absolute revenue terms than IDG or ISG, SSG’s recurring revenue model and high attach rates to Lenovo’s hardware installed base give it a financial profile more akin to a software company than a hardware manufacturer. The segment’s performance during the quarter helped cushion the overall margin impact of the lower-margin AI server ramp.

Management highlighted that the attach rate of services to device sales continued to climb, a metric that investors have been watching closely as a barometer of Lenovo’s ability to extract more value from each customer relationship. The company’s TruScale infrastructure-as-a-service platform, which allows enterprises to consume Lenovo servers and storage on an operating-expense basis rather than a capital-expense basis, has been gaining traction particularly among mid-market enterprises that lack the capital budgets of hyperscale cloud providers but still require AI-capable infrastructure. As detailed in Lenovo’s earnings release, the company’s non-hardware revenue streams are growing at a rate that significantly outpaces its overall top line.

Geopolitical Crosscurrents and Supply Chain Resilience

Lenovo’s results also underscored the company’s ability to navigate an increasingly complex geopolitical environment. As a Chinese-headquartered multinational with significant operations in the United States, Europe, and across Asia, Lenovo sits at the intersection of U.S.-China technology tensions. Export controls on advanced semiconductors, evolving tariff regimes, and data sovereignty requirements have forced the company to maintain a geographically diversified manufacturing and supply chain footprint. Lenovo operates major production facilities in China, Mexico, Hungary, Brazil, India, and Japan — a distributed model that provides resilience against single-point-of-failure risks.

The memory price dynamics that boosted Q3 revenue also carry a cautionary note for the quarters ahead. If customers have indeed pulled forward purchases to beat price increases, there is a risk of a demand air pocket in the first half of calendar 2026. Analysts at several brokerages flagged this concern in post-earnings commentary, though most maintained that the structural AI-driven upgrade cycle would provide a floor under demand even if the cyclical pull-forward effect fades. Bloomberg reported that Lenovo executives acknowledged the pull-forward dynamic but expressed confidence that the breadth of demand drivers — including the AI PC refresh cycle, enterprise digital transformation, and sovereign AI infrastructure buildouts — would sustain momentum.

The AI PC Gambit: Betting on the Next Hardware Supercycle

Beyond the data center, Lenovo is making a significant strategic wager on the concept of the “AI PC” — a personal computer equipped with dedicated neural processing hardware capable of running AI inference workloads locally, without relying on cloud connectivity. The company has been among the most aggressive in the industry in marketing AI PC capabilities, partnering with Intel, AMD, and Qualcomm on next-generation processor platforms that integrate NPUs alongside traditional CPU and GPU cores.

The thesis is straightforward: as AI applications — from real-time translation and intelligent document summarization to code generation and creative tools — become embedded in everyday productivity workflows, the demand for local AI processing power will drive a massive hardware upgrade cycle. Lenovo’s scale in the PC market, with a global share consistently above 23%, positions it to capture a disproportionate share of this transition. The company has launched AI PC models across its ThinkPad, Yoga, and Legion product lines, targeting enterprise, consumer, and gaming segments respectively. Early adoption rates have been encouraging, though the true inflection point is expected to arrive as software ecosystems mature and killer AI applications emerge that require on-device processing capabilities.

What Wall Street Is Watching Next

For investors, the Lenovo earnings report crystallized a set of questions that will define the company’s trajectory over the next several quarters. Can the ISG division achieve meaningful margin expansion as AI server volumes scale? Will the pull-forward in PC demand create a hangover effect, or will the AI PC upgrade cycle provide sustained tailwinds? And can the SSG services business grow fast enough to shift Lenovo’s overall margin profile toward a more software-like model?

The answers will depend in part on factors outside Lenovo’s control — NVIDIA’s GPU supply allocation decisions, memory pricing trajectories, and the pace of enterprise AI adoption. But the Q3 results demonstrated that Lenovo has built a diversified platform capable of riding multiple technology waves simultaneously. With $22.2 billion in quarterly revenue and a clear strategic roadmap spanning edge devices, AI infrastructure, and managed services, the company has established itself as a formidable participant in the global technology hardware industry’s most consequential transformation in decades. Whether the profit line can catch up to the revenue ambition remains the central question for the quarters ahead, as reported across coverage from Morningstar and the Financial Post.