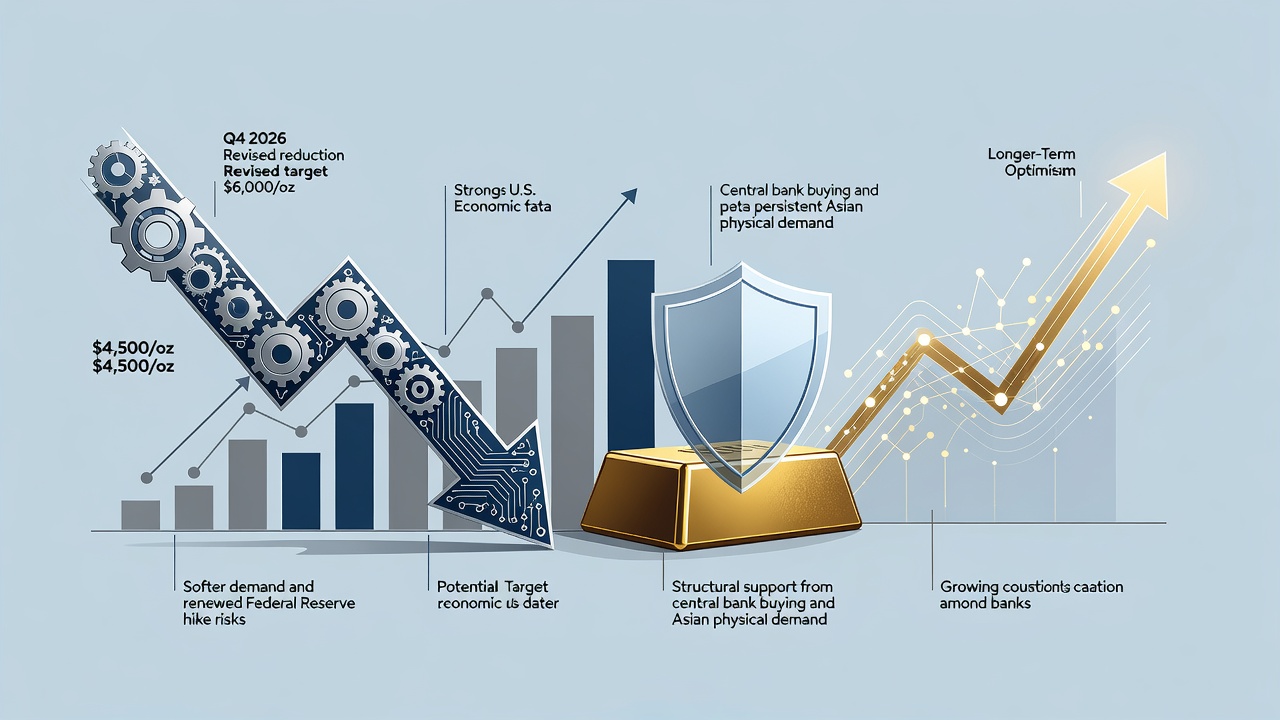

Gold prices sit near $4,170 an ounce. Momentum has cooled after early 2026 peaks. And now one of Wall Street’s most bullish voices has dialed back its expectations. Yahoo Finance reports JPMorgan lowered its fourth-quarter 2026 gold price target to $4,500 an ounce. That’s a sharp 25% cut from prior levels near $6,000.

The revision landed this week. It reflects softer near-term demand. Investor interest has dried up. Central bank purchases slowed on the surface. High interest rates keep weighing on the non-yielding metal. But don’t mistake this for surrender. The bank’s longer-term stance holds firmer ground.

Earlier this year JPMorgan Global Research painted a far more aggressive picture. Its February 2026 forecast called for gold to average $5,708 an ounce for the full year. Fourth quarter alone targeted $6,300. The new table shows meaningful trims across 2026 quarters. Third quarter now sits at $4,300. The full-year average dropped to $5,243.

Greg Shearer, head of base and precious metals at J.P. Morgan, captured the mood. “Gold is stuck in a bit of a technical no-man’s land, trudging above the 200-day moving average around $4,340/oz and capped for now below the 50-day moving average at $4,730/oz,” he said in the bank’s research note. “Amid this sideways plod, and with growing worries that the Fed might have to respond to energy-driven inflation with hikes, gold is on the back burner for most investors at the moment.”

Market forces at play

Those Fed worries dominate the near-term outlook. Hot U.S. economic data could push policymakers toward rate hikes instead of cuts. That scenario raises the bar for gold. Higher yields make yield-bearing assets more attractive. Western exchange-traded fund flows turn negative. The Reuters story on the latest tweak highlights exactly this risk. “Risks to the forecast skew to the downside” if summer data reignites inflation concerns, the bank warned.

Central banks drove much of gold’s run from 2021 through 2025. Net purchases averaged 225 tons per quarter. That pace looked to falter in early 2026. Reported first-quarter net buying totaled just 16 tons. Turkey sold 60 tons in March alone. Yet the picture gets murkier once unreported flows enter the equation.

The World Gold Council uses London over-the-counter data and Swiss refinery flows to estimate true demand. Those metrics suggest first-quarter purchases actually rose to around 244 tons. China stands out. Net imports hit 317 tons. The People’s Bank of China stepped up reported buying from one ton per month to eight tons in April. Strategic diversification away from dollar assets explains much of this activity. The 2022 freezing of Russian reserves sent a clear signal.

Additional demand channels could surprise markets. Chinese insurance companies won approval in 2025 to allocate up to 1% of assets under management to physical gold. That equates to roughly 200 tons at current levels. Analysts speculate the cap could rise toward 5%. Disclosure rules remain loose for now. Any ramp-up would add fresh buying pressure.

Geopolitical fractures add another layer. The Iran-Israel-U.S. tensions, while easing in some respects, underscore longer-term risks around inflation, U.S. fiscal policy, and global power shifts. These themes support gold as a hedge. Clarity on conflict resolution would remove some tail risks for energy prices and yields. Until then, uncertainty lingers.

Other major banks show a range of views. Goldman Sachs trimmed its end-2026 target to $4,900 an ounce but still cites sovereign demand and emerging-market diversification. Bank of America sees $4,800 by year-end. Morgan Stanley points to $5,200 in the second half, stressing the need for stronger ETF inflows. UBS and Deutsche Bank land in similar territory around $5,200 and $4,800 respectively. Consensus sits well below JPMorgan’s earlier calls. Yet most remain directionally positive for late 2026 and 2027.

The bank’s own research page, updated in recent months, still lists a base case of $6,000 an ounce by the final quarter of 2026 and $6,300 in 2027. Those figures appear in older quarterly breakdowns. The latest client note clearly walks them back for the immediate horizon. This gap between average annual forecasts and year-end targets often reflects front-loaded weakness dragging down the full-year number even as a second-half recovery is expected.

Physical demand in Asia offers a structural floor. Hong Kong’s new gold clearing system, launching with participation from JPMorgan, Deutsche Bank, and major Chinese and Singaporean lenders, could shift some settlement activity eastward. Asia already accounts for the bulk of global physical offtake. Reduced reliance on London and New York infrastructure may gradually influence liquidity and pricing power.

Current spot prices trade roughly 25% below the January 2026 all-time high near $5,589. The 200-day moving average around $4,340 acts as a technical support level in JPMorgan’s bear-case analysis. A break below could accelerate selling. But the bank continues to view that as a structural floor rather than a breakdown point.

So what happens next? Short-term pressure looks real. Fed rhetoric, summer economic prints, and lingering high rates cap upside. But structural buyers haven’t vanished. Central banks in emerging markets keep accumulating. Chinese institutions eye larger allocations. Geopolitical risks refuse to disappear entirely.

Investors who bought the early 2026 dip may feel validated if prices stabilize here. Those waiting for a deeper pullback now have fresh encouragement from the bank’s revised targets. The rebound’s durability faces a test. Whether gold breaks toward $5,000 later this year or stays rangebound near $4,200-$4,500 depends heavily on policy signals from Washington.

One thing seems clear. The bull case didn’t evaporate with this tweak. It simply got postponed. Demand re-acceleration in the second half remains the base assumption. Physical and official buying should regain traction once rate-cut prospects firm up again. Until that clarity arrives, gold trades in limbo. Bulls watch the Fed. Bears eye the data. And the metal itself? It waits.