Wall Street has spent much of 2026 celebrating headline GDP numbers and AI-fueled stock gains. Yet one veteran strategist sees a different story buried in the data. Jim Paulsen, former chief investment officer at The Leuthold Group, warns that a shift in the balance between private and public contributions to growth points to trouble ahead for equities.

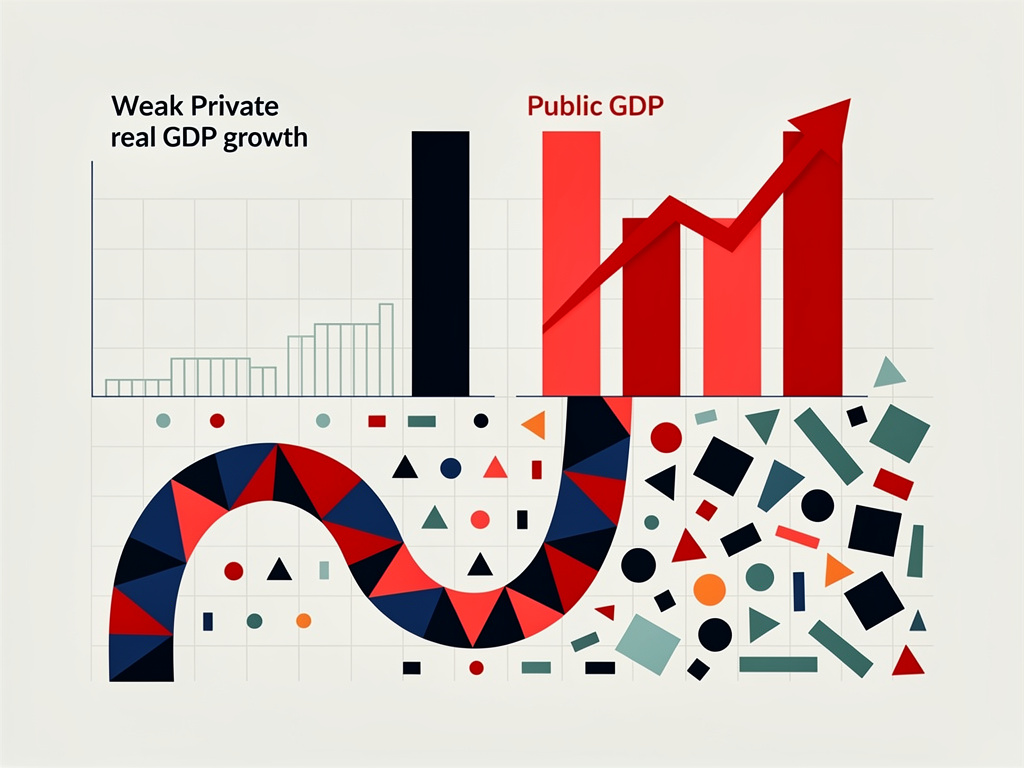

The numbers tell a stark tale. Private real GDP rose just 1% year-over-year in the first quarter of 2026. Public real GDP, by contrast, jumped 4%. That reversal in the private-to-public real GDP ratio marks a break from the norm. For decades the private sector has grown faster. When the pattern flips, stocks have often suffered.

Public Spending Takes the Lead

Paulsen laid out his concerns in a Substack post that quickly drew attention from market participants. He noted the first-quarter drop in the ratio might prove temporary. “I am concerned, however, that this may just be the first of several quarters when the private/public real GDP ratio declines,” he wrote. (Business Insider, June 18, 2026)

Higher defense outlays tied to the Iran conflict are set to boost public GDP further in the current quarter. Private activity, meanwhile, faces headwinds from elevated interest rates and energy costs. The combination could sustain the imbalance. And history offers little comfort. Periods when public spending has dominated GDP growth have coincided with stock-market weakness. Think World War II, the years after the global financial crisis, and the COVID shock. The S&P 500 typically declined in years when the private-public ratio contracted, including the early 2000s and post-crisis period.

So far this year the market has masked these pressures. Tech shares climbed 29% through mid-June, powered by investor enthusiasm, infrastructure programs and administration support. Energy and industrials that benefit from federal grants have also outperformed. Yet other sectors tell a different story. Financials, health care, consumer discretionary and communications have fallen between 1% and 7% since January, according to State Street Investment Management data.

This divergence is no accident. The same forces lifting public GDP appear to be propping up select parts of the market while leaving the broader economy and many stocks behind. Paulsen’s analysis suggests the private sector’s slowdown is real. And it is showing up in asset prices.

Just days earlier Paulsen highlighted additional signals from the stock market itself. Despite solid jobs data, employment-services stocks trade near their lowest relative levels in at least 26 years. “Despite a small increase in employment, the relative price of employment services stocks has not shown any sign of improvement in overall job conditions,” he observed. Consumer discretionary names, which historically track real retail sales, have underperformed since 2020. Their relative prices sit near 2011 lows and show no lift from recent employment gains. “Consumer stocks on Wall Street are suggesting retail results on Main Street are poised — not to improve soon on better job prospects — but rather to worsen further.” (Business Insider, June 9, 2026)

Cyclical stocks paint an even darker picture. These names, sensitive to overall economic momentum, have seen their relative prices collapse since the start of the year. They now hover near the lowest levels since 1990. The speed and extent of that drop mirror behavior before or during past recessions in 1990, 2002, 2009-10 and 2020. “Cyclical stocks — those most sensitive to the pace of economic growth — are suggesting the economy is closer to a recession than a period of improvement,” Paulsen said. “The speed of the collapse in the relative price of cyclical stocks and their current relative price low both portray a weak U.S. economy.”

But. The broader market narrative remains upbeat. Many forecasters point to resilient consumer spending and corporate earnings. Paulsen’s work challenges that view. He has long argued that headline growth can overstate underlying momentum. In earlier commentary he described recent GDP prints as something of an illusion when stripped of certain volatile components. His latest observations fit a consistent theme: the economy’s private engine is sputtering even as public spending and select technology investments provide a temporary lift.

Investors face a difficult task. They must weigh strong official statistics and narrow market leadership against these persistent undercurrents. Paulsen does not predict an immediate crash. He does warn of turbulence if the private-public imbalance persists. “This could bring turbulence for the stock market,” he added.

Recent market action lends weight to the caution. Dispersion between winners and losers has widened. Volatility has ticked higher in some measures. And policy pressures — from oil prices to interest rates to currency strength — continue to build with lagged effects that could weigh on activity through the fall, according to separate analysis by Paulsen reported in Financial Post earlier this week.

The coming quarters will test which signals prove more reliable. If private growth remains subdued while public spending surges, the historical pattern Paulsen identifies may reassert itself. Stock prices have ignored such warnings before. They have also paid the price when the disconnect eventually closes. For portfolio managers and analysts watching the composition of GDP as closely as the headline number, Paulsen’s ratio offers a metric worth tracking closely.