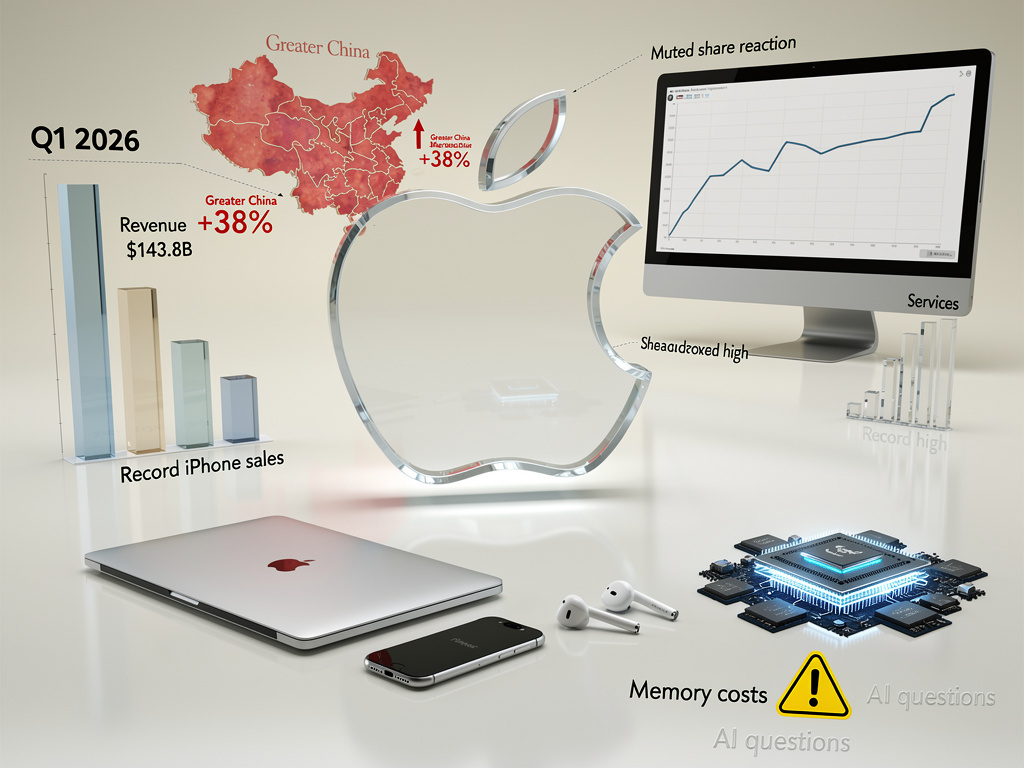

Apple Inc. unveiled fiscal first-quarter results that shattered expectations, propelled by blockbuster iPhone sales and a rebound in Greater China, but investors delivered a muted response amid worries over escalating memory costs and lingering questions about artificial intelligence momentum. Revenue climbed 16% year-over-year to $143.8 billion, topping LSEG estimates of $138.5 billion, while diluted earnings per share hit $2.84, surpassing forecasts of $2.67. The iPhone category alone generated $85.3 billion, up 23% and marking an all-time high, as CEO Tim Cook described demand as “simply staggering.”

Services revenue also reached a record $30 billion, rising 14%, underscoring the resilience of Apple’s high-margin ecosystem. Gross margins expanded to 48.2%, bolstered by favorable product mix during the robust iPhone cycle. Operating cash flow surged to a record $53.9 billion, enabling $32 billion in shareholder returns, including $25 billion in buybacks and a $0.26 per share dividend payable February 12. Apple’s installed base of active devices swelled to over 2.5 billion, up from 2.35 billion a year earlier, highlighting enduring customer loyalty.

iPhone Ignites Global Revenue Surge

In Greater China, sales rocketed 38% to $25.53 billion, exceeding estimates of $21.8 billion and driven by iPhone strength, where Cook noted an “all-time record for upgraders in mainland China” and double-digit switcher growth far exceeding projections. Every geographic region posted records: Americas up 11%, Europe 13%, Japan 5%, Rest of Asia Pacific 18%. iPhone topped smartphone sales in urban China, the U.S., U.K., Australia, and Japan, with 99% customer satisfaction for the iPhone 17 family per 451 Research.

Other segments showed mixed results. Macs fell 7% to $8.4 billion amid launches of M4 models, iPads rose 6% to $8.6 billion with record upgraders, and wearables dipped 2% to $11.5 billion due to AirPods Pro 3 supply limits. Services thrived with double-digit paid subscriber growth, Apple TV viewership up 36%, and developers earning over $550 billion via App Store since 2008.

China Rebound Defies Headwinds

The Greater China turnaround stood out after years of declines averaging 5%, tying near prior peaks from December 2021. Cook attributed it to “product strength,” with iPhones, iPads, and Macs leading categories. India also shone with quarterly records across iPhone, Mac, iPad, and services, plus double-digit install base growth, where most buyers were new to Apple’s products. Globally, nearly half of Mac buyers and over half of Apple Watch purchasers were first-timers.

Yet, forward guidance tempered enthusiasm. Apple projected 13%-16% revenue growth for the March quarter ($107.8-$110.7 billion, above LSEG’s $104.8 billion), but flagged iPhone supply constraints from tight 3-nanometer capacity at Taiwan Semiconductor Manufacturing Co. CFO Kevan Parekh noted gross margins of 48%-49%, incorporating rising memory prices that had minimal Q1 impact but loom larger ahead.

Memory Crunch Clouds Margins

Cook confirmed “market pricing for memory increasing significantly,” with DRAM up 55-60% and NAND 33-38% per TrendForce, tied to AI-driven shortages. Parekh affirmed these costs are “baked into” guidance, alongside higher R&D for AI atop normal investments. Operating expenses rose 19% to $18.4 billion, reflecting AI and silicon pushes like Apple’s modem.

AI progress featured prominently: A majority of eligible iPhone users leverage Apple Intelligence, with a Google partnership integrating Gemini models for enhanced Siri launching spring 2026. Cook emphasized on-device and private cloud processing for privacy, calling Apple’s platforms “the best in the world for AI.” Still, analysts like Morgan Stanley’s Erik Woodring flagged near-term caution from memory pressures and historical Q1 S&P 500 underperformance.

Investor Restraint Persists

Despite the blowout—EPS up 19%, EBIT margins at 35.4%—Apple shares rose only about 1% in extended trading to around $261, per MacRumors and CNBC, far from explosive moves implied by options pricing a 3.9% swing. Pre-earnings, shares had slipped on leadership rumors and AI delays, with JPMorgan’s Samik Chatterjee noting memory cost concerns overshadowing iPhone signals.

Wedbush’s Daniel Ives stayed bullish with a $350 target, deeming 2026 “massive” for AI, services, and iPhone upgrades, keeping Apple on his Best Ideas List. Gene Munster of Deepwater Asset Management hailed the China result as evidence of Apple’s “Teflon” brand amid geopolitics. On X, traders like @StockMKTNewz and @amitisinvesting celebrated the smash—revenue $143.8 billion vs. $138.1 billion expected—but reaction stayed subdued.

AI Roadmap Draws Scrutiny

Apple’s AI path includes Siri relaunch in February, WWDC features in June, a foldable iPhone, and 2nm chips for iPhone 18. Partnerships like Google validate strategy, but spending trails Meta and Microsoft, per Apple’s press release. Investors seek monetization clarity beyond hardware, with services as the high-margin bet.

Tariffs impacted $1.4 billion, in-line. U.S. investments hit $600 billion over four years, supporting 500,000 jobs. As Cook put it, “This was a remarkable quarter… our best work is yet to come.” Yet, with valuation at 31 times forward earnings and peers like Nvidia promising faster growth, Wall Street demands proof AI delivers supercycle profits.

Strategic Horizons Ahead

Analysts like Bank of America’s Wamsi Mohan expect strong iPhone and services continuity despite China App Store softness. Evercore ISI added Apple to its Tactical Outperform list on core strength. Supply chase persists with lean inventories, but Cook cautioned balancing demand remains unpredictable. India’s opportunity looms large as the second-biggest smartphone market.

Apple’s fortress—ecosystem lock-in, 97-99% satisfaction—powers through cycles. Q1 proves iPhone endures, China revives, services scale. Investor tepidness reflects high bars: Can AI unlock services explosion amid cost storms? 2026’s foldables, 2nm, Siri pivot hold keys, positioning Apple for outperformance if execution matches ambition.