The U.S. economy received a welcome dose of relief on Thursday as the Bureau of Labor Statistics reported that consumer price inflation cooled more than economists had anticipated in January 2026, dropping to its lowest annual rate in eight months and rekindling hopes that the Federal Reserve may soon resume cutting interest rates. The data sent equity futures higher and bond yields lower, as traders recalibrated their expectations for monetary policy in the months ahead.

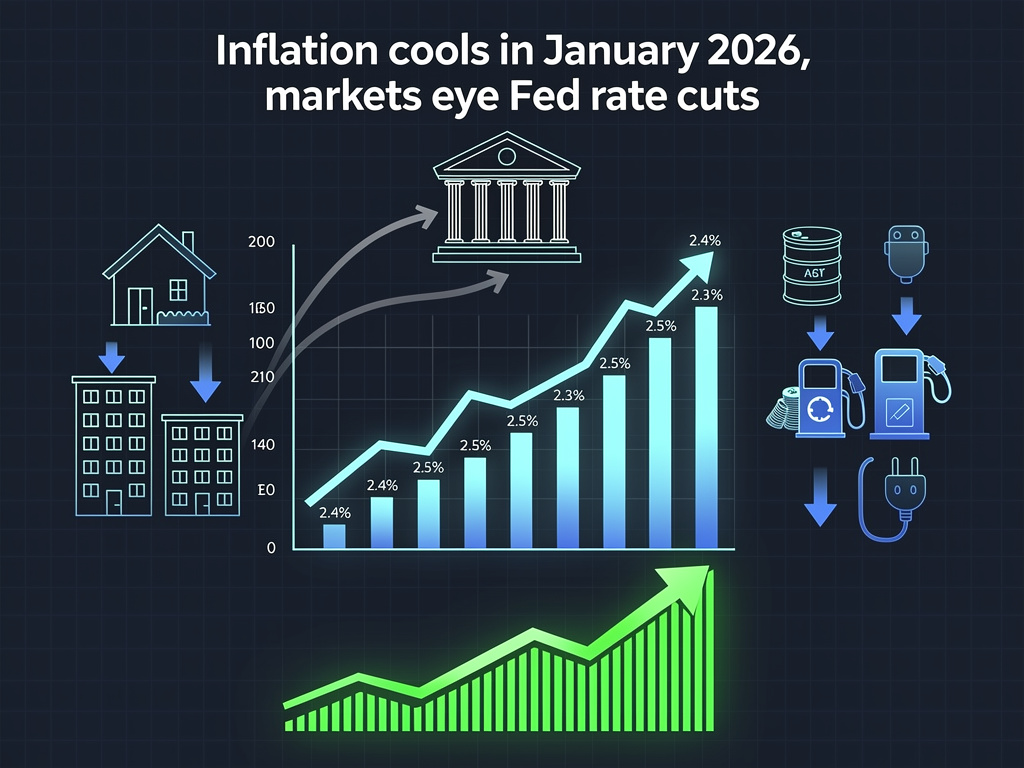

The Consumer Price Index rose 2.4% on a year-over-year basis in January, a notable deceleration from the 2.7% reading posted in December 2025 and below the 2.5% consensus forecast compiled by Dow Jones, according to CNBC. On a monthly basis, headline CPI increased just 0.2%, undershooting the 0.3% expectation that had been widely held on Wall Street. The report marked the most encouraging inflation print in months and suggested that the stubborn price pressures that had complicated the Fed’s plans throughout late 2025 may finally be abating in a meaningful way.

Core Inflation Hits a Nearly Five-Year Low, Signaling Broad-Based Disinflation

Perhaps more significant than the headline number was the performance of core CPI, which strips out volatile food and energy prices and is closely watched by Federal Reserve officials as a gauge of underlying inflationary trends. Core CPI rose 2.5% year-over-year in January, down from 2.6% in December and matching Wall Street expectations, as reported by Seeking Alpha. That reading represented the lowest core inflation rate since March 2021 — a milestone that underscored how far the economy has traveled from the inflationary crisis that peaked above 9% in mid-2022.

On a month-over-month basis, core CPI also rose a modest 0.2%, matching the headline figure and reinforcing the narrative that price pressures are dissipating across a broad swath of the economy. The combination of cooler headline and core readings provided what many economists described as the clearest evidence yet that the disinflationary trend, which had appeared to stall in the fourth quarter of 2025, has resumed with renewed momentum. For Fed Chair Jerome Powell and his colleagues on the Federal Open Market Committee, the data offered a measure of reassurance that their patient approach to rate cuts has not allowed inflation to become re-entrenched.

Shelter Costs Finally Crack: The Key Driver Behind the Cooling Trend

The single most important factor behind January’s encouraging inflation report was the continued deceleration in shelter costs, which represent roughly one-third of the overall CPI basket and have been the most persistent source of above-target inflation over the past two years. According to USA Today, rental increases slowed to their lowest levels since 2021, a development that economists have long anticipated but that took far longer to materialize in the official data than many had expected. The lag between real-time rent measures — which showed significant cooling beginning in mid-2024 — and the CPI’s methodology for capturing housing costs had been a source of frustration for policymakers and market participants alike.

The shelter component’s deceleration is particularly consequential because of its outsized weight in the index. When shelter inflation was running hot, it was nearly impossible for the overall CPI to converge toward the Fed’s 2% target, regardless of what was happening in other categories. Now, with rent growth moderating meaningfully, the arithmetic of inflation is shifting in a more favorable direction. Energy prices provided an additional tailwind in January, falling 1.5% during the month and helping to pull the headline figure below the core reading. Gasoline prices, which had been a source of consumer angst throughout much of 2025, contributed to the energy decline as global crude oil markets remained well-supplied heading into the new year.

Markets Rally as Rate-Cut Expectations Surge

Financial markets responded enthusiastically to the data. The Dow Jones Industrial Average climbed sharply in early trading, with TipRanks reporting that the blue-chip index led major averages higher as investors priced in a greater probability of Federal Reserve rate cuts in the coming months. The S&P 500 also advanced, building on gains that had been tentative in the days leading up to the report. Treasury yields fell across the curve, with the benchmark 10-year note yield dropping several basis points as bond traders moved to reflect the improved inflation outlook.

The interest rate futures market shifted meaningfully in response to the report. Federal funds futures contracts began pricing in a higher likelihood that the Fed would cut its benchmark rate at one of its upcoming meetings, with some traders now betting on a move as early as the March or May FOMC gatherings. As Investor’s Business Daily noted, the inflation data has significant implications for the S&P 500 and broader equity markets, as lower rates tend to boost stock valuations by reducing the discount rate applied to future corporate earnings. Growth stocks, which are particularly sensitive to interest rate expectations, outperformed value shares in the immediate aftermath of the release.

The Fed’s Dilemma: Patience Versus the Risk of Overtightening

The January CPI report arrives at a critical juncture for Federal Reserve policymakers. After cutting rates by a cumulative 75 basis points in the second half of 2025, the central bank paused its easing cycle at its January 2026 meeting, citing the need for additional evidence that inflation was sustainably moving toward its 2% target. That decision drew criticism from some quarters of the market, where participants argued that the Fed was being unnecessarily cautious and risking an economic slowdown by keeping rates too restrictive for too long.

Thursday’s data lends ammunition to those who have been calling for a resumption of rate cuts. With headline CPI at 2.4% and core at 2.5%, the gap between actual inflation and the Fed’s 2% target has narrowed considerably. More importantly, the trajectory is clearly downward. The three-month and six-month annualized rates of core inflation have both decelerated, suggesting that the improvement is not merely a one-month aberration but part of a sustained trend. Fed officials have repeatedly emphasized that they are looking for confidence in the direction of inflation, not necessarily waiting for it to hit 2% precisely before adjusting policy. By that standard, the January report should provide meaningful comfort.

What’s Driving Disinflation Beyond Housing

While shelter costs have garnered the most attention, the disinflation story extends well beyond the housing sector. Used car prices, which had been a volatile and often inflationary force in the post-pandemic economy, have stabilized and in some months declined. Medical care services inflation has moderated. And goods prices more broadly have been in outright deflation for several months, reflecting improved supply chains, normalized inventory levels, and subdued consumer demand for discretionary items. According to CNBC, the breadth of the disinflation in January was notable, with fewer individual CPI components showing elevated price increases than at any point since the inflationary surge began.

Food prices, which had been a persistent pain point for American households, also showed signs of moderation. Grocery store inflation has slowed considerably from its peak, though prices at restaurants and other food-away-from-home establishments remain somewhat elevated due to ongoing labor cost pressures in the hospitality industry. Still, the overall food category contributed less to the annual CPI increase than it had in any month since early 2021, providing additional relief for consumers who have been vocal about the cumulative impact of price increases on their household budgets.

The Consumer Confidence Connection

The inflation report carries implications that extend well beyond monetary policy and financial markets. Consumer sentiment, which has lagged behind the improvement in hard economic data for much of the post-pandemic period, could receive a meaningful boost if Americans begin to perceive that price pressures are genuinely easing. Surveys from the University of Michigan and the Conference Board have consistently shown that inflation remains the top economic concern for a majority of U.S. households, even as the labor market has remained strong and wage growth has been solid. A sustained decline in CPI readings could help close the gap between economic reality and public perception.

For the Biden administration and policymakers in Washington, the data provides a welcome talking point. The cumulative increase in consumer prices since the onset of the pandemic remains substantial — roughly 22% since January 2020 — and that sticker shock continues to shape voter attitudes toward the economy. But the direction of travel matters, and a CPI reading that is meaningfully below expectations offers evidence that the worst of the inflationary episode is firmly in the rearview mirror. As USA Today reported, the January data suggests that inflationary pressures are dissipating in a manner that could give both consumers and policymakers greater confidence in the economic outlook.

Risks on the Horizon: Tariffs, Geopolitics, and the Path Ahead

Despite the encouraging headline figures, economists cautioned that several risks could complicate the disinflationary trend in the months ahead. Trade policy remains a wildcard, with the potential for new or expanded tariffs on imported goods threatening to inject fresh inflationary impulses into the economy. Geopolitical tensions, particularly in the Middle East and Eastern Europe, could disrupt energy markets and reverse the recent decline in oil prices. And the labor market, while showing signs of gradual cooling, remains tight enough that wage growth could put upward pressure on service-sector prices if productivity gains fail to keep pace.

There are also base-effect considerations that could make year-over-year comparisons less favorable in certain months ahead. The sharp decline in energy prices that occurred in early 2025 means that the favorable base effects that have been helping to push down the annual CPI rate will begin to fade. Economists at several major Wall Street banks have noted that the path from 2.4% to the Fed’s 2% target may prove more difficult than the journey from 3% to 2.4%, as the remaining sources of above-target inflation — particularly in services — tend to be stickier and less responsive to monetary policy.

What This Means for the Federal Reserve’s Next Move

The January CPI report does not guarantee an imminent rate cut, but it significantly strengthens the case for one. Fed officials will have additional data points to consider before their next policy meeting, including the Producer Price Index, the Personal Consumption Expenditures price index (the Fed’s preferred inflation gauge), and the February employment report. If those readings corroborate the message of the CPI — that inflation is cooling broadly and sustainably — the pressure on the FOMC to act will intensify considerably.

As Investor’s Business Daily emphasized, the interplay between inflation data and Fed policy remains the single most important driver of equity and fixed-income markets in 2026. Thursday’s report tilted the balance toward a more dovish policy stance, but the central bank has shown a strong preference for moving deliberately and avoiding the kind of premature easing that could allow inflation to reignite. For now, markets are betting that the data will continue to cooperate — and that the next rate cut is a matter of when, not if. The January CPI report, with its broad-based cooling and encouraging trajectory, has brought that moment measurably closer.