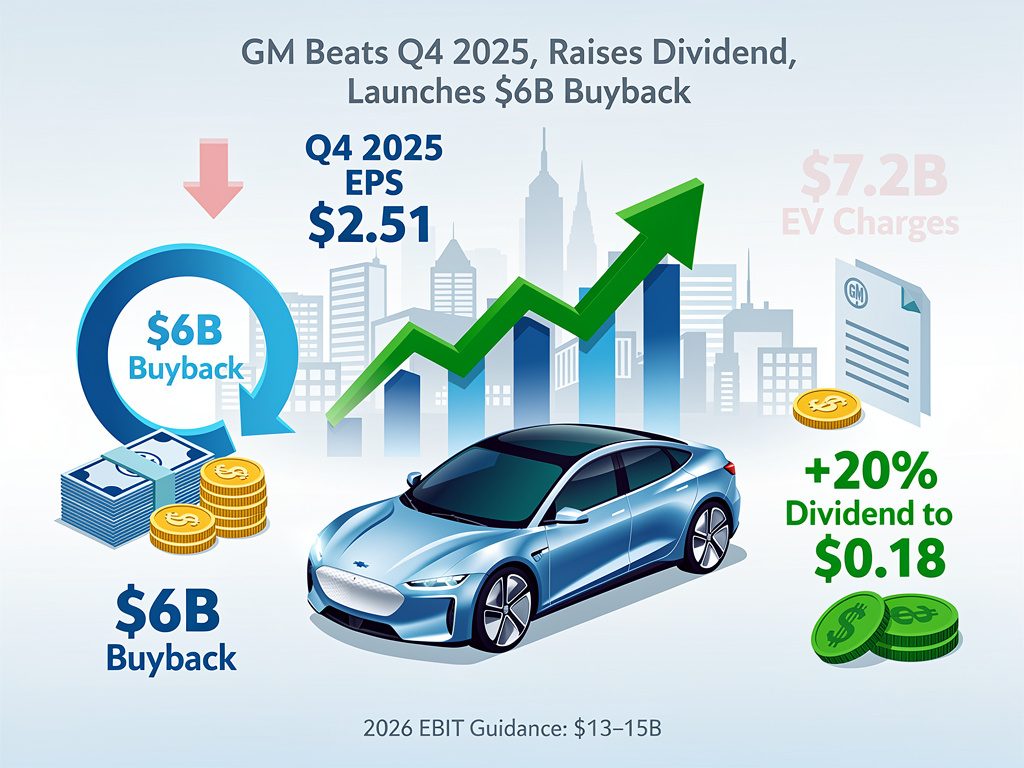

General Motors Co. surpassed Wall Street’s earnings forecasts for the fourth quarter of 2025, delivering adjusted earnings per share of $2.51 against expectations of $2.20, while announcing a 20% dividend hike and a fresh $6 billion stock repurchase program. The Detroit automaker reported revenue of $45.29 billion, edging below the $45.8 billion anticipated, as a quarterly net loss of $3.3 billion reflected over $7.2 billion in special charges tied to electric vehicle strategy shifts and China restructuring. Shares climbed more than 4% in premarket trading following the release, signaling investor approval of the capital return measures amid broader industry headwinds.

CEO Mary Barra emphasized the company’s robust cash generation, stating in the earnings materials, “GM remains in a strong position to return capital to shareholders.” The quarterly dividend on common stock rose 3 cents to 18 cents per share, payable March 19 to shareholders of record by March 6. This follows a pattern of share reduction, with outstanding shares dropping to 904 million at year-end 2025 from 995 million in 2024 and 1.2 billion in 2023, boosting per-share metrics through prior buybacks. The new repurchase authorization carries no expiration date and can be paused at management’s discretion, per the PR Newswire release.

Quarterly Results Under the Hood

Adjusted EBIT for the quarter stood at $2.8 billion, up from $2.5 billion a year earlier, with an automotive free cash flow of $2.8 billion nearly doubling the prior year’s figure. North America delivered $2.2 billion in adjusted EBIT, while international markets added $278 million. China equity income improved sharply to a $513 million loss from $4.1 billion last year, though restructuring charges weighed heavily. Special items included $7.914 billion for EV realignment due to softer demand and policy shifts like the end of federal incentives, plus $842 million for China exits, as detailed in reconciliations from StockTitan.

Full-year 2025 net income attributable to stockholders came in at $2.7 billion, down from $6.0 billion in 2024, with adjusted EBIT steady at $12.7 billion on $185 billion in revenue. Automotive operating cash flow totaled $18.7 billion, yielding $10.6 billion in adjusted free cash flow, meeting updated guidance. These figures underscore operational resilience despite EV setbacks, with GM North America margins at 6.8% for the year.

2026 Outlook Signals Profit Rebound

Looking ahead, GM projects net income of $10.3 billion to $11.7 billion in 2026, with adjusted EBIT of $13 billion to $15 billion and EPS of $11 to $13, surpassing consensus estimates around $11.73. Adjusted automotive free cash flow is eyed at $9 billion to $11 billion, supporting $10 billion to $12 billion in capital spending, including battery joint ventures. Headwinds include $3 billion to $4 billion in tariffs, $1 billion to $1.5 billion in commodities and FX, and onshoring costs, offset partly by $1 billion to $1.5 billion EV loss improvements and regulatory credits, according to Yahoo Finance.

Barra highlighted in the press release, “For several years now, GM’s strong brands and winning vehicles, as well as our technology-driven services and operating discipline, have delivered consistently strong cash generation.” This framework underpins the capital allocation shift toward shareholders, even as EV capacity adjustments respond to demand declines and policy changes eliminating consumer incentives.

EV Strategy Pivot Amid Policy Shifts

The massive Q4 charges stem from realigning EV investments, including a pre-announced $7.1 billion hit, plus smaller items like $357 million in legal settlements over OnStar and airbags, $133 million for the Cruise unit wind-down, and headquarters relocation costs. U.S. sales for Q4 dipped 6.9% to 703,000 vehicles, though full-year volume rose 5.5% to 2.853 million, crowning GM the top U.S. seller, as noted by CNBC’s coverage in its earnings article.

GM’s EV unit is expected to narrow losses significantly in 2026, aided by emissions credit savings of $550 million to $750 million. Barra has aligned the strategy with evolving U.S. policies, noting opportunities for onshoring to match customer preferences for internal combustion engines and hybrids. This flexibility positions GM to navigate tariff exposures estimated at $3.1 billion for 2025, with offsets boosting prior guidance.

Investor Reactions and Market Context

On X, CNBC autos reporter Michael Wayland highlighted the earnings beat and announcements, drawing quick attention from investors. Posts from accounts like SpecialSitsNews underscored the $6 billion buyback and dividend bump as signs of confidence in the $13 billion to $15 billion EBIT target. GM stock gained 4.51% intraday, reflecting optimism over capital returns despite the GAAP loss.

Analysts view the moves favorably, with the repurchase adding to prior programs that slashed share count meaningfully. As rivals grapple with similar EV demand softness, GM’s balanced portfolio—spanning trucks, SUVs, and select EVs—provides a buffer. Capital spending remains focused on profitability drivers like Super Cruise expansion and core ICE refreshes.

Strategic Capital Discipline

GM Financial contributed $609 million in adjusted EBT for Q4, down slightly year-over-year. ROIC-adjusted held at 19.3%, signaling efficient asset use. The board’s actions affirm a sustainable model: invest in growth, fortify the balance sheet, then distribute excess cash. With 2026 guidance implying 8-10% North American margins, GM eyes a return to pre-charge profitability peaks.

This earnings package positions General Motors as a cash flow machine in a volatile auto sector, prioritizing shareholders amid EV recalibrations and trade tensions. The $6 billion buyback, paired with the dividend lift, could drive further per-share accretion, appealing to value-oriented investors.