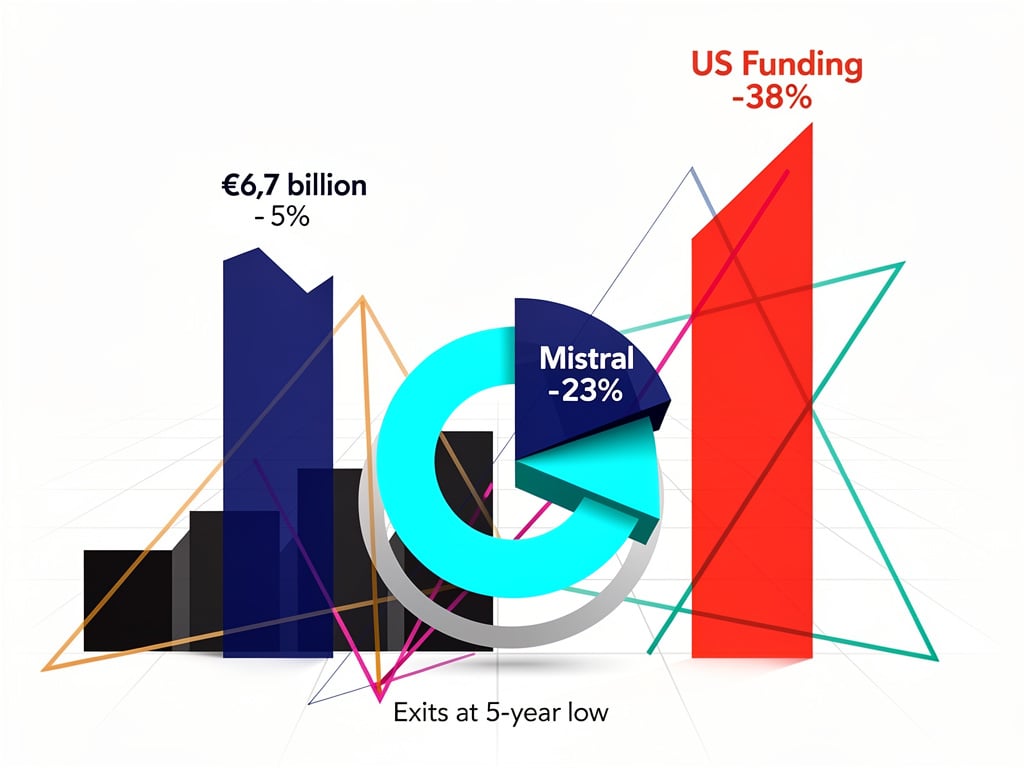

French startups raised €6.7 billion in 2025. That figure marked a 5 percent drop from the year before. Deal volume fell even more sharply, down 21 percent to 411 rounds. Meanwhile the US saw funding jump 38 percent and Europe overall climbed 12 percent. One company explained much of the gap. Mistral alone took 25 percent of all French capital raised that year.

The numbers come from a detailed analysis by Alexandre Dewez, partner at venture firm 20VC. His report, published on Substack, runs nearly 100 slides. It lays bare a scene that minted its first decacorn yet struggles to produce breadth. AI powered 43 percent of total funding, up from 27 percent. It claimed 23 percent of rounds, nearly double the prior share. Remove Mistral and the rest of the market looks stalled.

But. This concentration tells only part of the story. France produced several large early bets on foundation models. H closed a €212 million seed. Genesis raised €97 million. Gradium took €64 million and Bioptimus €32 million. Such rounds signal confidence in homegrown talent. They also highlight how capital now flows toward a narrow set of bets on frontier systems.

France lacks clear category winners in the segments that matter most commercially. The Next Web notes that the UK boasts ElevenLabs in voice synthesis. Sweden has Lovable in coding tools. Germany counts Parloa for customer service and n8n for automation. Mistral differentiates mainly through its European roots. Companies seeking sovereign alternatives choose it. Technical leadership against OpenAI, Anthropic and the Chinese labs remains elusive. The firm lost its early open-source advantage. Multimodal competition demands capital and compute that US and Chinese players command in far greater supply.

One standout broke the pattern. Pennylane crossed €100 million in annual recurring revenue. Growth hit 130 percent year over year. The company raised twice in 2025 at valuations of €2 billion and then €3.9 billion. It moved beyond accounting software into full ERP and neobanking services aimed at French small and midsize firms. Operations now extend into Germany. Such execution at scale remains rare.

Defense technology emerged as the second-fastest area of expansion. European defense startups pulled in $1.6 billion in 2025, a 148 percent increase. In France 18 companies raised €228 million, up 25 percent. Harmattan became the country’s first defense unicorn with a $200 million Series B led by Dassault Aviation. The firm develops autonomy and mission systems for aircraft. President Emmanuel Macron hailed the deal as progress toward strategic autonomy. Geopolitical tensions, the war in Ukraine and shifting security alliances drive the surge. Germany captured the largest share of European defense capital. France carved a niche in AI-enabled military platforms.

US investors now shape French outcomes more than local ones. American funds participated in rounds that represented 55 percent of total capital deployed in 2025. Their money focused on AI, especially the foundation-model builders. At Series A only 30 percent of the top 20 rounds saw French leadership. Pan-European firms took 60 percent and US investors 10 percent. Where once Index Ventures, Accel and Balderton stood out as consistent cross-border leaders, at least 15 such funds now compete for French deals.

French venture capital sits in an awkward middle ground. Micro-funds handling €5 million to €35 million dominate pre-seed and seed. International players sweep in at Series A. Several established French funds face difficulty raising new vehicles. Those that succeed close smaller sizes than before. Talent drains away. Multiple founders split time between Paris and the Bay Area. Teams behind Poolside, Genesis, Zero Entropy and Anyshift operate across both cities. French firms including Founders Future, Frst and Hexa opened San Francisco offices. Entrepreneur First shut its Paris outpost in late 2025 to double down on the US program. Hundreds of entrepreneurs had moved through that accelerator since 2018.

Exits tell the most sobering tale. Liquidity reached €5.3 billion in 2025. That total fell 65 percent from the previous year and marked the lowest level in five years. Public markets stayed largely shut to European tech. Trade sales failed to compensate. Secondaries became the primary route to cash. VC-led and private-equity-led deals provided partial liquidity for early backers but rarely delivered the outsized returns that refill venture coffers. France counts 47 unicorns created over time. Roughly 36 of them, or 77 percent, likely remain above $1 billion valuation based on recent financing, revenue or hiring metrics. The other 11 have probably slipped below. The ecosystem still wrestles with scaling durable companies that endure.

Regulations add friction. Nearly 60 percent of European tech startups surveyed reported delays in product development due to rules, compared with 44 percent of small US firms. The EU AI Act imposes strict requirements for high-risk systems and transparency. Critics argue these standards slow local innovators while US competitors race ahead with fewer constraints. Some companies consider relocating operations outside Europe. Yet the rules also reflect a deliberate preference for caution and long-term societal benefit.

Cultural differences help explain the divergence. Europe does not trail in talent or core technology. European engineers rank among the world’s best. The gap lies in mindset. US teams optimize for speed. They ship fast, observe, adjust. Waste occurs but velocity compounds. European approaches favor value. Decisions stretch longer. Filters apply more rigorously through regulation and skepticism. One observer captured it sharply. “Europe isn’t behind technologically. The gap is cultural.” Speed counts as a cultural default in America. In Europe it remains a conscious choice.

AI magnifies these traits. It compresses cycles in the US. In Europe it can prolong deliberation. When code grows cheap, judgment and taste become the true differentiators. Enterprises seek transformation more than disruption. Measuring real value offers the best check against hype. France possesses nuclear-powered electricity at low cost, strong research institutions and supportive government programs such as French Tech 2030. These assets position the country to build specialized AI applications in health care, energy, logistics and defense.

Government initiatives carry weight. France committed €109 billion to AI, much of it private capital from partners in the United Arab Emirates aimed at data centers. The country leads Europe in developing AI models. Yet business adoption lags. Less than 10 percent of French enterprises used AI technology last year. Across Europe the figure varies widely. Romania sits at 3 percent. The gap between invention and implementation remains wide.

Recent deals suggest pockets of momentum. In March 2026 the French startup AMI, co-founded by former Meta chief AI scientist Yann LeCun, raised $1 billion. The round drew backing from Toyota, Nvidia and Samsung. AMI works on systems that understand the physical world in the manner of animals and humans rather than language-based chatbots. The company aims to produce universal intelligent systems inside five years. Such investment shows international confidence in French scientific depth.

Still the structural issues persist. Concentration in a few AI names crowds out broader development. Low exits limit recycling of capital and talent. Regulatory burden and slower decision cycles deter some founders. Yet the very traits that slow France could prove advantages in building trustworthy, enterprise-grade AI that lasts. Judgment matters when hype fades. Systems thinking separates durable products from flashy demos.

Dewez’s analysis does not offer simple fixes. It documents a maturing market that grew dependent on superstar bets while the middle thinned. Defense spending and targeted public programs provide tailwinds. Success will hinge on whether French companies can move from strong research to category-defining commercial products and whether local capital can regain ground against US and pan-European funds. The AI wave both exposed these weaknesses and offers the clearest path to address them. Concentration creates risk. Focused execution on vertical applications and sovereign systems could convert that risk into durable strength.

France holds real cards: talent, energy infrastructure, policy ambition. Realizing their value demands speeding select decisions without discarding the caution that distinguishes European approaches. The coming years will test whether the country can broaden its winner list beyond a handful of AI labs and defense specialists. The data shows the challenge clearly. The remedy sits within reach if execution matches the ambition.