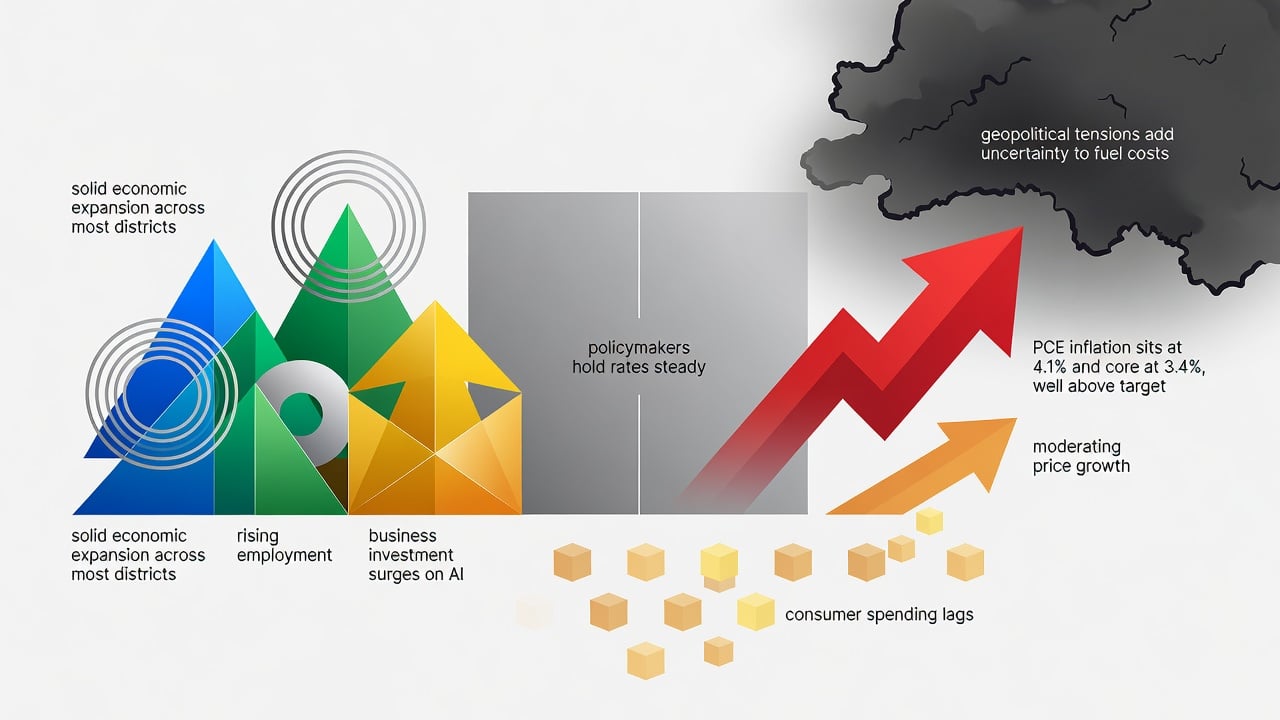

The Federal Reserve painted a picture of modest progress this week. Economic activity picked up across most of the country. Yet inflation refused to fade away completely. The central bank’s Beige Book, released on July 15, captured a U.S. economy that keeps moving forward. But the path remains uneven.

Eleven of the 12 Fed districts reported slight to moderate growth from late May through early July. One district stayed flat. Employment rose in several areas without igniting big wage pressures. Prices increased modestly everywhere. And in every single district, that price growth held steady or slowed from the prior period. Short sentences. Clear signals. Policymakers now head into their late-July meeting with fresh, if imperfect, data in hand.

“Contacts generally expected the economy to continue to expand in the coming months, but several districts noted elevated uncertainty in the outlook for fuel costs,” the Fed said in the report. The data was gathered on or before July 6. That timing matters. It came before a fresh flare-up in Middle East tensions pushed oil prices higher again. Reuters highlighted how those renewed hostilities have reignited worries just as a brief lull had offered some relief.

But the expansion shows real breadth. Manufacturing gained support from orders tied to data centers, machinery and defense. Consumers traded down to cheaper options in many places. Agriculture weakened. And the FIFA World Cup gave a temporary lift to hospitality and retail in host cities from Boston to the West Coast. Bars in Greater Boston even reported a noticeable jump in beer sales thanks to the tournament. Facts like these add texture. They remind readers that national numbers often hide regional stories.

Inflation tells a more complicated tale. The July 2026 Monetary Policy Report showed total PCE prices rising 4.1 percent over the 12 months through May. Core PCE, which strips out food and energy, stood at 3.4 percent. Both figures sit well above the Fed’s 2 percent target. And they mark an acceleration from earlier readings. The report noted that real GDP expanded at a 2.1 percent annualized rate in the first quarter. Business fixed investment surged 11.1 percent in that period, fueled heavily by artificial-intelligence infrastructure. Household consumption, by contrast, grew a more modest 1.3 percent. The gap between corporate spending and consumer demand stands out. It points to an economy increasingly driven by capital investment rather than everyday purchases. Federal Reserve laid out those figures in detail.

Half the policymakers at the Fed’s June meeting projected at least one interest-rate increase by the end of 2026. They cited persistent price pressures. Chair Kevin Warsh has stayed quiet on his personal outlook for rates. He has, however, repeatedly stressed the bank’s commitment to restoring price stability. “The Committee has noted that economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East,” the Monetary Policy Report stated. Productivity growth remains strong. Job gains have matched workforce expansion. The unemployment rate held near 4.2 percent in June. Private payrolls strengthened to about 100,000 per month in the second quarter. Yet non-labor costs keep climbing. Energy, transportation and raw materials drove those increases in services, construction and factories. Some businesses tied the pressures directly to tariffs or the Middle East situation.

Labor markets offer their own mixed read. Five districts saw modest to solid job gains. Seven reported little or no change. “Some employers in Memphis reported that they have not increased wages over the past three months despite rising employee requests for raises,” the St. Louis Fed noted, according to the Beige Book. In Minneapolis, elevated gasoline prices squeezed worker budgets. Job seekers faced fewer openings overall. Certain roles, such as nursing assistants or customer-service representatives, still offered better odds. The report suggested the labor market itself is not feeding inflation. That assessment aligns with comments from several Fed officials in recent weeks.

Consumer behavior reflects caution. Price sensitivity rose in a few districts. People opted for lower-cost goods and services. Retail sales varied. Housing activity stayed soft. And while credit remained available for larger firms, smaller businesses and households faced tighter conditions. These details matter for investors watching borrowing costs. They also matter for companies planning inventories or expansions. The Beige Book draws from conversations with actual business contacts. Its qualitative nature complements the hard data in the Monetary Policy Report.

Markets reacted with restraint to the releases. Treasury yields edged higher on renewed oil concerns. Equity indexes showed volatility but held gains in technology sectors tied to the AI boom. No one expects dramatic policy shifts at the upcoming meeting. The federal funds rate has sat at 3.5 percent to 3.75 percent all year. Warsh and his colleagues appear content to watch how events unfold. A preliminary U.S.-Iran peace agreement had cooled energy prices in June. That helped soften some inflation readings. Then hostilities resumed. Oil climbed back. Uncertainty returned. Several districts flagged that exact dynamic in their outlooks.

Longer term, the Fed sees productivity and capital spending as supports for growth. Labor supply remains constrained by demographics and lower immigration. Wage growth has stayed solid, around 3.4 percent in recent employment-cost data, yet productivity gains have helped keep unit labor costs in check. Inflation expectations among households ticked higher in the short term. Longer-term measures stayed anchored near 2 percent. The Monetary Policy Report highlighted new task forces examining inflation drivers, communications and the balance sheet. Those efforts signal the central bank is not standing still.

And the picture keeps evolving. Recent data from the Cleveland Fed’s inflation nowcasting tool showed mixed monthly changes for July. Producer prices fell unexpectedly in June before the latest oil spike. Cleveland Fed updates those estimates daily. On social media, analysts noted the Beige Book’s steady tone. “The Fed’s Beige Book showed the US economy improving overall, with steady job growth and inflation easing a bit,” one observer posted on X. Others pointed to persistent cost pressures in energy and transport. Real-time sentiment often amplifies official releases. It rarely replaces them.

So what comes next? Contacts across districts anticipate continued, if unspectacular, expansion. They watch fuel costs closely. Builders in the Cleveland district even expressed hope that reduced uncertainty around Middle East conflicts could bring more bidding opportunities. Tariffs remain a background factor in input costs. The combination of geopolitical risks, policy uncertainty and divergent spending patterns creates a complex environment for decision makers. The Fed will weigh all of it. Rate hikes remain on the table for some members. Patience defines the current stance.

Investors, executives and policymakers alike will parse every new data point. The latest reports do not resolve the tension between solid growth and above-target inflation. They do, however, confirm the economy’s resilience. Business investment in high-tech areas provides a floor. Consumer caution and energy volatility introduce drag. Mixed signals, yes. But not paralysis. The expansion continues. Price pressures linger. And the Federal Reserve stays focused on its dual mandate. The months ahead promise more of the same delicate balancing act.