For decades, a handful of European metropolitan hubs — London, Frankfurt, Amsterdam, Paris, and Dublin — have served as the backbone of the continent’s digital infrastructure. Known collectively as the FLAP-D markets, these cities attracted the lion’s share of hyperscale data center investment, becoming the default homes for the servers that power everything from streaming video to financial trading platforms. But a convergence of power constraints, regulatory friction, and surging demand driven by artificial intelligence is now forcing the industry to redraw its map in dramatic fashion.

The signals are unmistakable. According to a report from TechRadar Pro, Europe’s traditional data center capitals are running out of room. Grid capacity in Amsterdam has been effectively frozen for new large-scale builds. Dublin faces moratoriums and intense public scrutiny over energy consumption. Frankfurt’s power allocation for new facilities is increasingly constrained. Even London, the continent’s largest market, is contending with lengthy grid connection timelines that can stretch beyond five years. The result is an industry in the midst of a geographic redistribution not seen since the cloud computing era began.

Power Scarcity Becomes the Defining Bottleneck

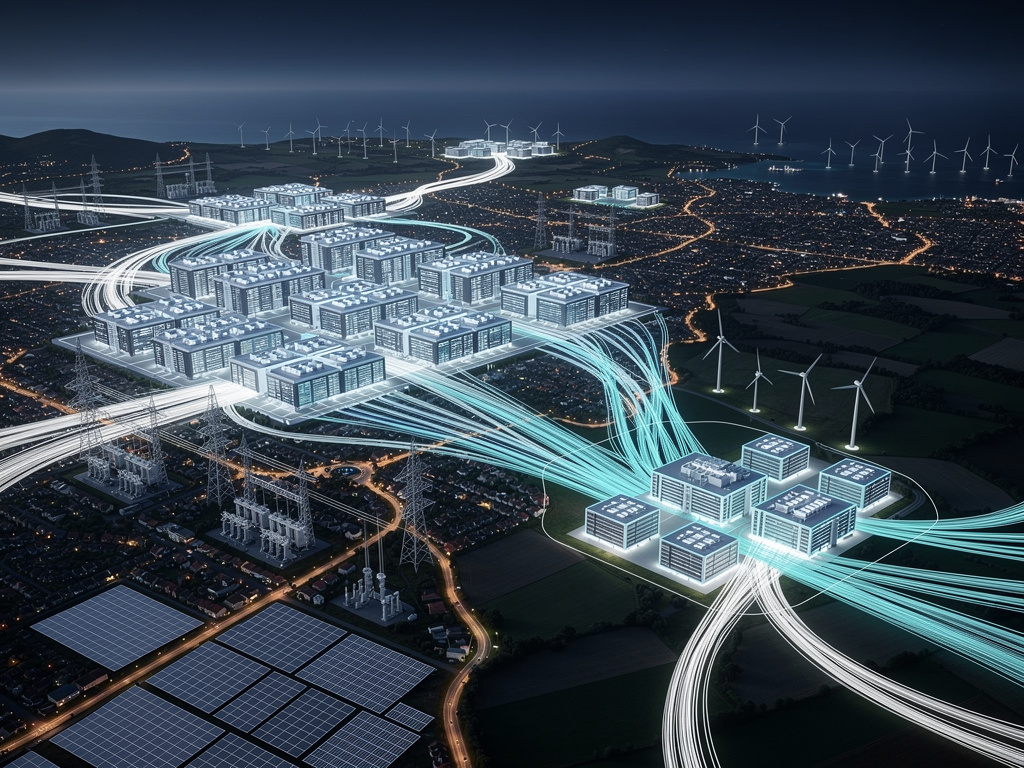

The core issue is electricity. Data centers are among the most power-hungry facilities on earth, and the rapid expansion of AI workloads — particularly the training and inference of large language models — has sent energy requirements soaring. A single AI-optimized rack can consume ten times the power of a traditional cloud computing rack. Multiply that across facilities designed to house tens of thousands of such racks, and the strain on national grids becomes acute.

In the Netherlands, the government imposed restrictions on new data center construction in the Amsterdam metropolitan area in 2022, citing concerns about energy consumption and grid stability. Those restrictions have not been meaningfully relaxed. Ireland, where data centers already consume roughly 21% of the nation’s total electricity, has faced repeated warnings from its grid operator, EirGrid, about the sustainability of continued expansion. As TechRadar Pro detailed, these constraints are not temporary hiccups but structural limitations that will define the next decade of European infrastructure planning.

The Rise of Europe’s Secondary Markets

With the traditional centers increasingly congested, capital is flowing toward secondary and tertiary European markets at an accelerating pace. Cities like Madrid, Milan, Warsaw, and the Nordics — particularly Stockholm and Helsinki — are emerging as serious contenders for large-scale data center development. These locations offer a combination of available land, more accessible power capacity, favorable climate conditions for cooling, and in many cases, a higher proportion of renewable energy in the grid mix.

The Nordic countries have been especially aggressive in positioning themselves as alternatives. Sweden and Finland benefit from abundant hydroelectric and wind power, cool climates that reduce cooling costs, and governments that have actively courted data center operators with favorable tax regimes and streamlined permitting. Norway, too, has entered the conversation, with its vast surplus of renewable hydroelectric power making it an attractive destination for energy-intensive AI workloads. Recent reporting indicates that Microsoft, Google, and several colocation providers have expanded their Nordic footprints significantly over the past 18 months.

Southern Europe Makes Its Bid

Spain has emerged as one of the most surprising beneficiaries of the redistribution. Madrid, in particular, has attracted billions of euros in committed data center investment. The country offers relatively affordable land on the outskirts of major cities, improving connectivity through new subsea cable landings, and a government eager to position Spain as a digital infrastructure hub. According to industry analysts, Spain’s data center capacity is expected to more than double by 2027, a growth rate that far outpaces the mature FLAP-D markets.

Italy and Greece are also drawing attention. Milan has long been a regional connectivity hub, and new investment is flowing into purpose-built campuses on its periphery. Greece, buoyed by new subsea cable projects connecting Southern Europe to the Middle East and North Africa, is positioning itself as a crossroads for data traffic between continents. These developments suggest that the European data center market is becoming far more geographically distributed than at any point in its history.

AI Demand Is Rewriting the Rules of Site Selection

The artificial intelligence boom has fundamentally altered what data center operators and their hyperscale customers look for in a site. Traditional criteria — proximity to major population centers, low latency to end users, and access to dense fiber networks — remain important but are increasingly secondary to one overriding factor: the ability to secure large blocks of power quickly. AI training clusters require enormous, uninterrupted power supplies, and the operators building them are willing to go wherever that power is available.

This dynamic is pushing development into locations that would have been considered fringe markets just a few years ago. Rural areas with proximity to power generation assets — whether renewable or otherwise — are suddenly viable. In some cases, operators are negotiating directly with energy producers for dedicated power supplies, bypassing congested public grids entirely. The trend mirrors what has already occurred in the United States, where data center construction has surged in places like central Ohio, rural Virginia, and west Texas, driven almost entirely by power availability.

Regulatory and Political Pressures Add Complexity

The expansion into new markets is not without friction. Local communities in many European regions have pushed back against data center proposals, citing concerns about noise, water usage, visual impact, and the perception that these facilities create relatively few permanent jobs despite their enormous footprint. In the Netherlands, public opposition was a significant factor in the government’s decision to restrict new builds. Similar resistance has emerged in parts of Ireland, Germany, and increasingly in the Nordic countries as proposals grow larger.

Regulatory frameworks also vary significantly across Europe. Permitting timelines, environmental impact assessments, and energy allocation policies differ from country to country — and sometimes from municipality to municipality. Operators expanding into Southern or Eastern Europe must contend with less mature regulatory environments for data center development, which can introduce uncertainty and delay. The European Union’s Energy Efficiency Directive, which imposes new reporting and efficiency requirements on data centers, adds another layer of compliance that operators must factor into their planning.

The Infrastructure Investment Pipeline Is Enormous

Despite these challenges, the investment pipeline for European data centers remains staggering. Industry estimates suggest that more than €100 billion in data center investment is either committed or under consideration across Europe through 2030. Much of this capital is flowing from U.S. hyperscalers — Amazon Web Services, Microsoft Azure, and Google Cloud — as well as from sovereign wealth funds, private equity firms, and specialized infrastructure investors who view data centers as a generational asset class.

The scale of individual projects is also growing. Where a large European data center might once have been measured in tens of megawatts of IT load, new campuses are being designed for hundreds of megawatts, with some proposals exceeding one gigawatt — a threshold that would have been unthinkable outside the United States just three years ago. These mega-campus developments require not just power but also water for cooling, robust fiber connectivity, and large tracts of land, further limiting where they can realistically be built.

What the Redistribution Means for European Competitiveness

The geographic spreading of data center capacity carries significant implications for Europe’s broader digital competitiveness. A more distributed infrastructure base could improve resilience, reduce latency for underserved regions, and spread the economic benefits of digital infrastructure investment more evenly across the continent. Countries that successfully attract data center investment stand to gain not just construction jobs but also long-term operational roles, increased tax revenue, and improved digital connectivity that can attract further technology investment.

However, the redistribution also raises questions about coordination. Without a coherent pan-European strategy for energy allocation, grid development, and data center planning, there is a risk that the expansion becomes fragmented and inefficient. Some industry leaders have called for a more unified approach, arguing that Europe’s ability to compete with the United States and Asia in the AI era depends on its capacity to build infrastructure at scale and speed. As the traditional centers fill up and new markets absorb the overflow, the decisions made by governments, grid operators, and investors in the coming years will determine whether Europe can keep pace with the extraordinary demands of the AI age — or whether its digital ambitions will be constrained by the physical limits of its infrastructure.

The era of European data center concentration in a handful of Western capitals is drawing to a close. What replaces it will be messier, more distributed, and far more consequential for the continent’s economic future.