Digital wallets once served as handy shortcuts on smartphones. Tap to pay at checkout. Store a few cards. Skip the fumbling for plastic. That convenience drew billions of users. Yet something deeper now unfolds beneath the surface.

These wallets no longer simply hold payment details. They sit at the center of decisions that determine which rail carries a transaction, how much it costs the merchant, how quickly funds settle and whether the purchase even clears. Radi El Haj, CEO and executive director of RS2, captured the change in a recent analysis. “The real shift in payments is not happening at the wallet layer,” he wrote. “It is happening much deeper in the stack, at the infrastructure layer that determines how transactions are routed, settled and priced across increasingly complex payment ecosystems.” (TechRadar)

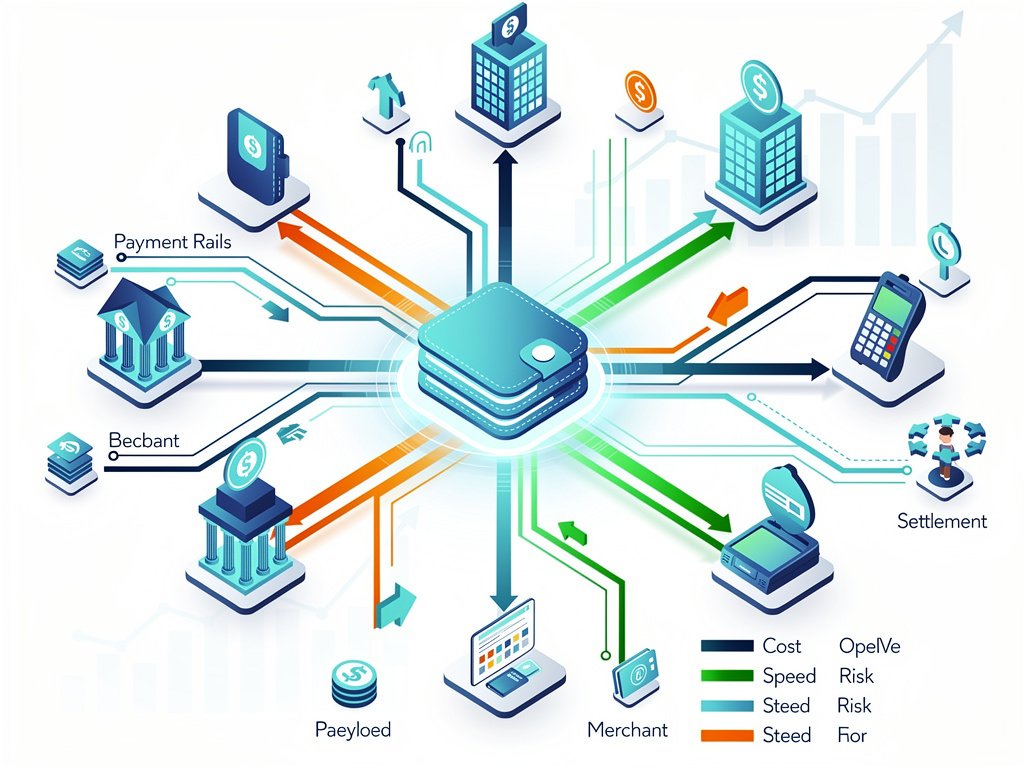

The transformation carries real stakes for banks, merchants and tech giants alike. A transaction that once followed a single card network now faces choices among account-to-account transfers, real-time rails, local schemes and traditional cards. Each option brings different costs, approval odds, settlement speeds and liquidity demands. The wallet evaluates those variables in real time. It doesn’t just initiate payment. It orchestrates it.

Numbers tell part of the story. Digital wallets are projected to surpass 5.2 billion users by the end of 2026. That figure equals more than 60 percent of the global population. They already drive 66 percent of e-commerce transaction value and 38 percent of point-of-sale payments value, according to Mastercard data. (Mastercard)

PYMNTS research from early 2026 shows wallets powering 35 percent of online transactions and 21 percent of in-store purchases across 11 countries that represent more than half of global GDP. Nearly two-thirds of recent U.S. cross-border payments flowed through digital wallets. (PYMNTS)

Those figures reflect adoption. The infrastructure shift runs quieter but proves more consequential. Card networks long provided consistency and broad acceptance. Now multiple rails coexist. Account-to-account moves promise lower fees and faster settlement yet introduce fragmentation. Real-time systems deliver immediate finality at the price of deeper integration. Local schemes boost success rates in specific markets. The wallet weighs those trade-offs.

“In a multi-rail world, the most important question is no longer ‘can a payment be made?’ but ‘how should this payment be routed?’” El Haj explained. Routing becomes a competitive edge. Decisions draw on context such as geography, transaction size, merchant type, historical approval rates and current liquidity needs. One purchase might route through a card network for its global reach. Another might favor an account-to-account path to cut costs. The consumer sees one tap. The backend runs calculations that once required separate systems.

Settlement patterns change too. What was once a predictable batch process in the back office turns strategic. Instant settlement improves cash flow yet demands different treasury management than delayed reconciliation. Merchants and their payment service providers must track varying liquidity impacts across rails. The wallet’s orchestration layer absorbs some of that complexity. It doesn’t eliminate risk. It redistributes it with greater precision.

Economics follow the same logic. Card transactions carry higher fees but strong acceptance. Alternative rails reduce merchant costs yet vary in reliability. Dynamic optimization across those options opens new margin opportunities. Success hinges less on raw processing power and more on intelligent decision engines that balance conversion rates against expense and risk. Wallets that master this layer gain an edge that consumers rarely notice but merchants feel in their margins.

Trust management evolves alongside routing. Traditional card systems embed fraud protections, chargeback rights and liability shifts. Newer rails require comparable safeguards to reach scale. Authentication, policy enforcement and real-time fraud signals now influence routing decisions before the transaction commits. The infrastructure itself becomes the control point. Biometric checks, tokenization and device-bound credentials strengthen that foundation.

Visa outlined related shifts in its predictions for 2026. The share of its e-commerce transactions using manual guest checkout fell from nearly half in 2019 to 16 percent in 2025. Among the company’s top 25 e-commerce sellers that figure sits in the low single digits. Single-click buy buttons powered by digital wallets replace cumbersome form entry. Fewer abandoned carts result. Fraud rates drop. Tokenization plays a central role. Visa has issued more than 16 billion tokens. (Visa)

Yet the wallet’s expanding role raises fresh questions. Who controls the customer relationship when the wallet decides the rail? Banks that issue cards watch their visibility diminish as tokenized credentials and wallet-stored identities take precedence. Merchants gain from lower costs and higher conversion but depend more heavily on the wallet providers’ rules and algorithms. Tech companies such as Apple and Google sit at the center of mobile wallets on their platforms. Their guidelines shape what functions merchants and banks can offer inside those wallets.

Suman Rausaria, vice president at Mastercard, described wallets moving beyond payments. “Wallets are evolving into super-apps, integrating identity, loyalty and embedded finance, transforming transactions into a value-rich customer journey,” he said. For consumers the wallet becomes daily infrastructure for ride-sharing, food delivery and shopping. For merchants multi-wallet acceptance and embedded flows reduce friction and support loyalty. (Mastercard)

Todd Pollak, chief revenue officer at Marqeta, struck a similar note on choice. “Digital wallets aren’t about locking consumers into one payment method,” he told PYMNTS. “They’re about giving people choice.” The wallet acts as gateway rather than destination. Users switch between stored cards, bank accounts or balances without friction. That flexibility accelerates adoption across age groups. Millennials, Gen X, baby boomers and Gen Z all turn to wallets for cross-border transfers at comparable rates in recent U.S. data. (PYMNTS)

Global patterns vary. Asia-Pacific markets embraced wallets earliest and deepest. WeChat Pay and Alipay handle the majority of in-store payments in parts of China. Europe advances through regulatory pushes for digital identity wallets. The United States sees younger consumers drive the shift from cards. Global Payments reported in March 2026 that digital wallets represent the top online payment method for 39 percent of Americans aged 18 to 24 and 41 percent of those 25 to 34. Direct card use online is forecast to decline from 49 percent in 2025 to 43 percent by 2030. (Global Payments)

Payment orchestration platforms already position themselves for this world. They connect multiple rails, apply routing logic and surface intelligence to merchants. The most sophisticated versions embed risk signals directly into the decision flow. A transaction with elevated fraud indicators might route to a rail with stronger authentication even if it carries higher cost. The wallet becomes the point where consumer intent, merchant needs and infrastructure realities converge.

Challenges remain. Fragmentation across rails can confuse smaller merchants who lack the technical resources to optimize. Regulatory differences by region add complexity. Data privacy rules limit how much information flows into routing algorithms. And the very power concentrated in a few wallet providers invites scrutiny from antitrust authorities and banking regulators.

Still the direction looks clear. Wallets have crossed from convenience tools into core payment infrastructure. The interface consumers touch stays simple. The decisions behind it grow more sophisticated. One tap now triggers layers of analysis that balance cost, speed, risk and liquidity in ways that would have required teams of treasury specialists a decade ago.

El Haj put it plainly. “In reality, the future of digital wallets will be defined far less by what users see on screen and far more by how intelligently payments are orchestrated behind the scenes.” That orchestration already shapes billions of transactions daily. It will determine which companies thrive as payments move further into multi-rail complexity.

Merchants who integrate deeply with wallet providers stand to gain from higher approval rates and lower costs. Banks that partner on embedded finance and identity features can maintain relevance inside the wallet rather than compete against it. Tech platforms that refine their orchestration capabilities extend their reach into financial services without issuing credit themselves.

The humble digital wallet no longer feels humble. It decides. It routes. It protects. And in doing so it quietly becomes the gatekeeper for purchases large and small around the world.