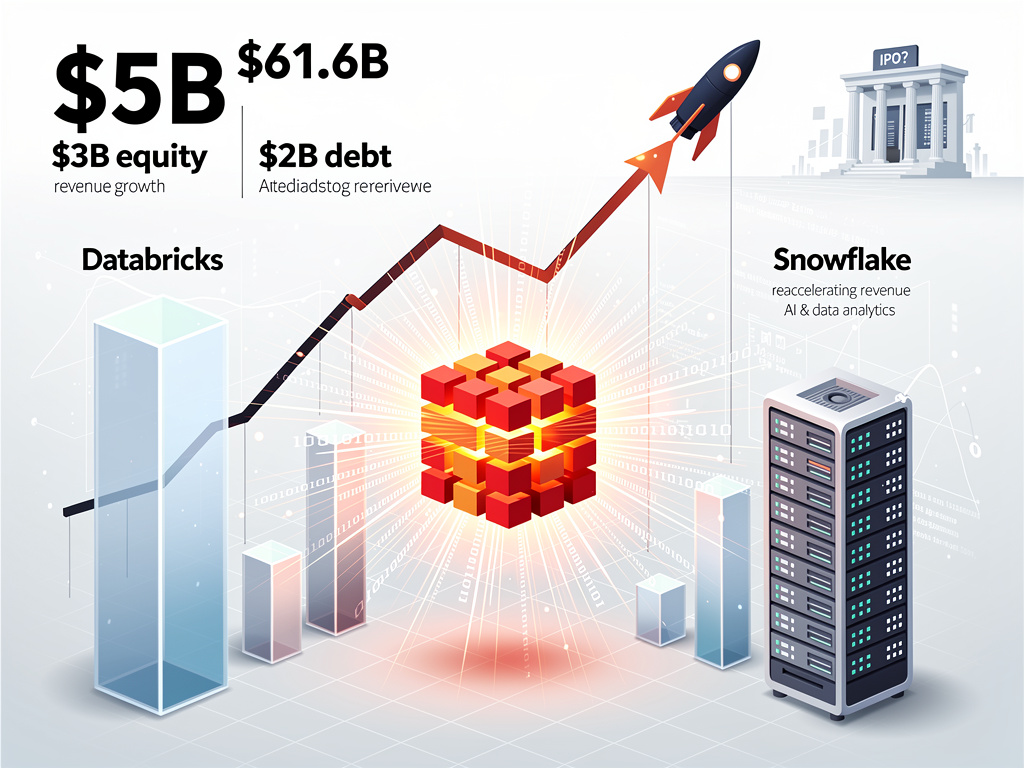

In the annals of private technology financing, few rounds have carried the sheer gravitational force of what Databricks just pulled off. The San Francisco-based data analytics and artificial intelligence company has completed a $5 billion funding round—one of the largest private capital raises in recent memory—combining $3 billion in equity with $2 billion in debt. The deal values the company at $61.6 billion and arrives at a moment when enterprise demand for AI infrastructure is accelerating at a pace that has surprised even the most bullish observers.

The round, first reported by CNBC, represents not just a financing event but a strategic inflection point for a company that has increasingly positioned itself as the backbone of enterprise AI adoption. With revenue growth reportedly reaccelerating, Databricks is sending a clear message to competitors, potential public market investors, and the broader technology industry: it intends to be the dominant platform upon which companies build their AI futures.

A Capital Structure Built for Aggression

The $5 billion raise is notable not only for its size but for its composition. By structuring the deal as $3 billion in equity and $2 billion in debt, Databricks has given itself extraordinary financial flexibility while limiting equity dilution for existing shareholders—a move that signals sophisticated financial engineering typically associated with companies on the cusp of going public. The debt component, in particular, suggests confidence in the company’s cash flow trajectory and its ability to service obligations from operating revenue rather than relying solely on future equity raises.

The equity portion of the round attracted a roster of institutional investors that reads like a who’s who of growth-stage technology finance. While Databricks has not disclosed the complete list of participants in this latest tranche, the company’s cap table already includes marquee names such as Andreessen Horowitz, T. Rowe Price, Tiger Global Management, and the venture arms of major cloud providers. The willingness of these investors to continue writing checks at a $61.6 billion valuation—up substantially from the company’s previous $43 billion valuation in a 2023 round—speaks volumes about the trajectory they see ahead.

Revenue Growth That Defies Late-Stage Gravity

Perhaps the most compelling element of the Databricks story right now is the reacceleration of its revenue growth. For a company of its scale, maintaining—let alone increasing—the pace of top-line expansion is exceedingly rare. According to reporting by CNBC, Databricks has seen its revenue growth rate speed up, a dynamic that stands in stark contrast to many late-stage private companies that have seen growth moderate as they approach the public markets. The company’s annualized revenue run rate is believed to have surpassed $3 billion, with some estimates placing it closer to $3.5 billion based on recent trajectory.

This acceleration is being driven by several converging forces. Enterprise customers are dramatically expanding their spending on data infrastructure as they rush to deploy generative AI applications, build large language model pipelines, and unify their data architectures. Databricks’ lakehouse platform—which combines elements of data lakes and data warehouses into a single architecture—has become the preferred foundation for organizations that want to avoid vendor lock-in while maintaining the flexibility to run diverse AI workloads. The company’s open-source roots, particularly its stewardship of Apache Spark and its development of the Delta Lake storage layer, have given it credibility with technical buyers that proprietary competitors struggle to match.

The Snowflake Rivalry Intensifies

No discussion of Databricks’ trajectory is complete without examining its increasingly fierce competition with Snowflake, the publicly traded cloud data platform. The two companies have been on a collision course for years, with each expanding into the other’s traditional stronghold. Snowflake, which went public in 2020 in one of the largest software IPOs in history, has been pushing deeper into AI and machine learning workloads. Databricks, meanwhile, has been building out its SQL analytics capabilities to compete directly with Snowflake’s core data warehousing business.

The rivalry has taken on new dimensions as generative AI has reshaped enterprise priorities. Databricks’ acquisition of MosaicML in 2023 for $1.3 billion gave it proprietary model-training capabilities that Snowflake has been scrambling to match. The company has also invested heavily in its Unity Catalog governance layer and its Mosaic AI suite, which allows enterprises to build, deploy, and monitor AI models within the Databricks environment. These moves have positioned Databricks as more than a data platform—it is increasingly an end-to-end AI development environment, a distinction that resonates powerfully with chief data officers and AI leads at Fortune 500 companies.

The IPO Question Looms Large

With $5 billion in fresh capital, Databricks has effectively removed any near-term financial pressure to go public. Yet paradoxically, the round may actually bring an IPO closer rather than push it further away. The debt component of the financing, in particular, is the kind of capital structure optimization that companies typically undertake in the 12 to 24 months preceding a public listing. By demonstrating that it can access debt markets at scale, Databricks has shown public market investors that it possesses the financial maturity and predictability they demand.

CEO Ali Ghodsi has been characteristically measured in his public comments about IPO timing, declining to commit to a specific date while acknowledging that the company is building the organizational infrastructure necessary for life as a public company. Databricks has been hiring seasoned public-company executives, investing in financial reporting systems, and cultivating relationships with the institutional investors who would anchor an eventual offering. The $61.6 billion valuation established in this round will serve as a critical benchmark—and a source of pressure—when the company eventually prices its shares on a public exchange.

What $5 Billion Buys in the AI Arms Race

The deployment of this capital will be watched closely by industry observers. Databricks has signaled that the funds will be used for a combination of product development, strategic acquisitions, and international expansion. The AI infrastructure market is evolving at a blistering pace, and the company faces the dual challenge of defending its existing position while pushing into adjacent markets. Investments in model serving, real-time data processing, and industry-specific AI solutions are all likely priorities.

Acquisitions could play a particularly significant role. The MosaicML deal demonstrated Databricks’ willingness to make bold moves to fill capability gaps, and the current market environment—in which many AI startups are well-funded but struggling to find sustainable business models—presents a target-rich environment. Companies specializing in data quality, AI observability, vector databases, and domain-specific model development could all be on Databricks’ radar. The $2 billion debt facility, which preserves equity for potential stock-based acquisition currency, gives the company additional flexibility to pursue these opportunities.

Enterprise AI Spending Shows No Signs of Slowing

The broader context for Databricks’ raise is an enterprise technology market that is undergoing a once-in-a-generation transformation. Chief information officers across industries are reallocating budgets toward AI infrastructure at an unprecedented rate, often at the expense of legacy software categories. According to multiple industry surveys, AI-related spending is expected to grow at compound annual rates exceeding 30% through the end of the decade—a tailwind that benefits platform companies like Databricks disproportionately.

This spending surge is not merely aspirational. Enterprises are deploying AI in production at increasing scale, moving beyond proof-of-concept experiments to mission-critical applications in areas such as fraud detection, supply chain optimization, customer personalization, and drug discovery. Each of these use cases requires robust data infrastructure—the ingestion, transformation, governance, and serving of data at scale—which is precisely what Databricks provides. The company’s consumption-based pricing model means that as customers run more workloads, Databricks’ revenue grows in lockstep, creating a powerful flywheel effect.

A Private Giant Casting a Public Shadow

At $61.6 billion, Databricks is now one of the most valuable private companies in the world, rivaling the market capitalizations of many publicly traded enterprise software firms. Its valuation exceeds that of companies like Palantir, Datadog, and Confluent—all of which are publicly traded and subject to the rigorous scrutiny of quarterly earnings cycles. This creates an unusual dynamic in which a private company is effectively setting competitive benchmarks for an entire sector of the public markets.

For employees holding Databricks equity, the round provides both validation and liquidity. The company has conducted secondary share sales in conjunction with previous funding rounds, allowing early employees and investors to realize partial returns. The $61.6 billion valuation establishes a new floor for these transactions and further cements the company’s status as one of the most coveted employers in enterprise technology. In a market where top AI talent commands extraordinary compensation packages, the ability to offer equity in a company valued at this level is a formidable recruiting advantage.

As Databricks enters this next chapter with $5 billion in fresh ammunition, the stakes could not be higher—for the company, for its competitors, and for the thousands of enterprises betting their AI strategies on its platform. The question is no longer whether Databricks will go public, but whether it can sustain the velocity that has made it one of the defining companies of the AI era. If the reacceleration in revenue growth is any indication, the answer may already be clear.