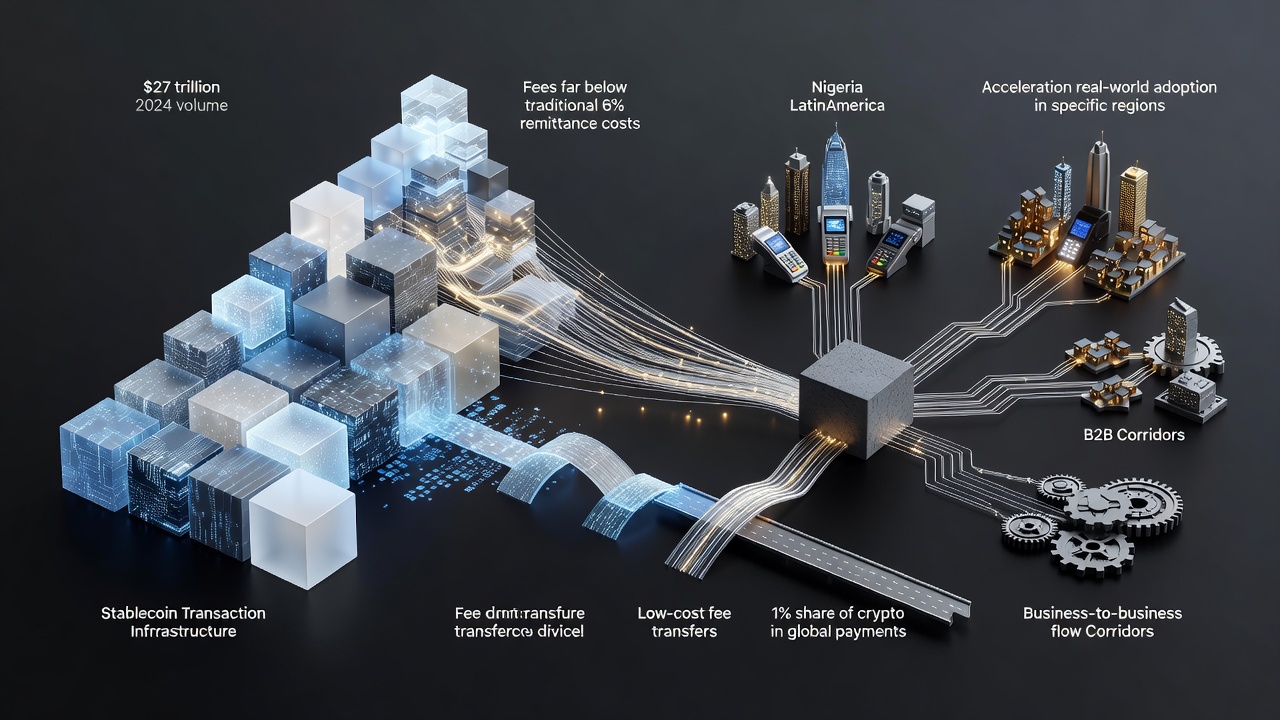

Volumes tell a stark story. Stablecoins processed more than $27 trillion in transfers in 2024. Some estimates put 2025 figures above $32 trillion. That already tops combined Visa and Mastercard transaction volumes. Yet their share of total global payments hovers near 1 percent. The gap between raw activity and mainstream penetration remains wide. But the momentum builds.

Costs Drive Adoption Faster Than Hype

Traditional cross-border remittances carry heavy burdens. The global average fee hit 6.36 percent in the third quarter of 2025, according to World Bank data. Banks charged nearly 15 percent in some cases. Compare that to blockchain networks. Solana transfers often run below 1 percent. Ripple settles in three to five seconds. Conventional wires take one to five days.

GlobalData forecasts a 58 percent rise in EU cross-border payments between 2023 and 2028. E-commerce, remote work and migration fuel the demand. Over half of global consumers already use international real-time payments. Fifty-seven percent of e-commerce shoppers made cross-border purchases last year. Transaction activity in that segment grew 43 percent annually. Yahoo Finance laid out these pressures clearly.

And the numbers keep climbing. Stablecoin supply expanded from $5 billion to more than $300 billion in five years. Payment volumes reached roughly $390 billion annually in 2025. B2B flows made up about 60 percent of that total. Monthly B2B stablecoin payments jumped from under $100 million in early 2023 to more than $6 billion by mid-2025. Fireblocks compiled those figures from McKinsey and Artemis Analytics reports.

Nigeria offers a vivid case. The country received about $59 billion in crypto inflows from July 2023 to June 2024. That accounted for roughly 60 percent of sub-Saharan Africa’s stablecoin volume. Households and small businesses turn to dollar-pegged tokens for speed and a hedge against naira volatility. Remittances there cost an average 9 percent. Stablecoins deliver near-instant movement through mobile wallets. “What began as a niche crypto use has grown into a significant payments route,” the IMF observed in its analysis. Reuters reported the details in June 2026.

But adoption faces friction. Hidden costs exist. Users must set up wallets, acquire crypto and manage without traditional safeguards. Regulatory pushback appears in key markets. Brazil’s central bank moved to restrict stablecoin settlement in cross-border payments for certain providers. Officials there also discuss expanding taxes on virtual-asset transfers to close perceived loopholes. Latin America still leads in several corridors. Local-currency stablecoins and direct bank integrations drive real volume in Brazil, Mexico and Colombia.

Institutions watch closely. Visa tests pre-funded stablecoins on its network to speed settlements without locking up capital for days. Mastercard explores blockchain rails. Banks form partnerships with payments firms to test tokenized deposits and stablecoin flows. The Bank for International Settlements runs prototypes that tokenize reserves and commercial deposits. Early results suggest faster reconciliation and fewer intermediaries.

Remittance specialists take notice too. MoneyGram and others experiment with crypto rails. The crypto-powered remittances market stood at $4.8 billion in 2025. Projections show it reaching $28.6 billion by 2034 at a 22 percent compound annual growth rate. Stablecoins now dominate many emerging-market flows because they remove currency risk and cut fees below 1.5 percent in efficient setups.

Challenges persist. Oversight worries mount when flows bypass formal banking. Illicit finance risks draw regulator attention. Volatility in non-stable assets deters conservative users. Yet the infrastructure improves. Attestations verify reserves. Multiple blockchains offer redundancy. Liquidity pools deepen in high-volume corridors.

So the trajectory sharpens. Demand for faster, cheaper transfers will not fade. E-commerce, gig workers and migrant families generate steady pressure. Traditional systems improve with real-time rails. They still carry legacy costs and delays. Crypto options deliver immediacy today. Their transaction counts grow. Enterprise pilots multiply. Consumer apps spread in Africa, Southeast Asia and Latin America.

One percent of global flows still leaves enormous headroom. If stablecoins capture even a modest slice of the $900-billion-plus annual remittance market, the absolute numbers turn material. Banks that ignore the shift risk disintermediation. Fintechs that integrate both worlds stand to gain. The data no longer supports viewing this as experimental. It functions as parallel infrastructure. And it expands. Quietly. Relentlessly.