London dealers once stocked mostly familiar European and Japanese nameplates. That picture has shifted fast. Last year Chinese-built vehicles accounted for roughly 285,000 new registrations in the UK, a leap from just 384 units recorded back in 2015. The surge shows no sign of slowing in 2026.

BYD nearly doubled its British sales in the first half of this year to more than 37,000 cars. Chery Group brands including Omoda and Jaecoo posted even sharper gains. In May alone Chery moved 11,100 vehicles across its three marques while BYD shifted 5,200. MG, owned by China’s SAIC, grew 13 percent to nearly 7,500 units that month. Leapmotor and Geely, barely visible a year earlier, suddenly registered 900 and 1,100 cars respectively.

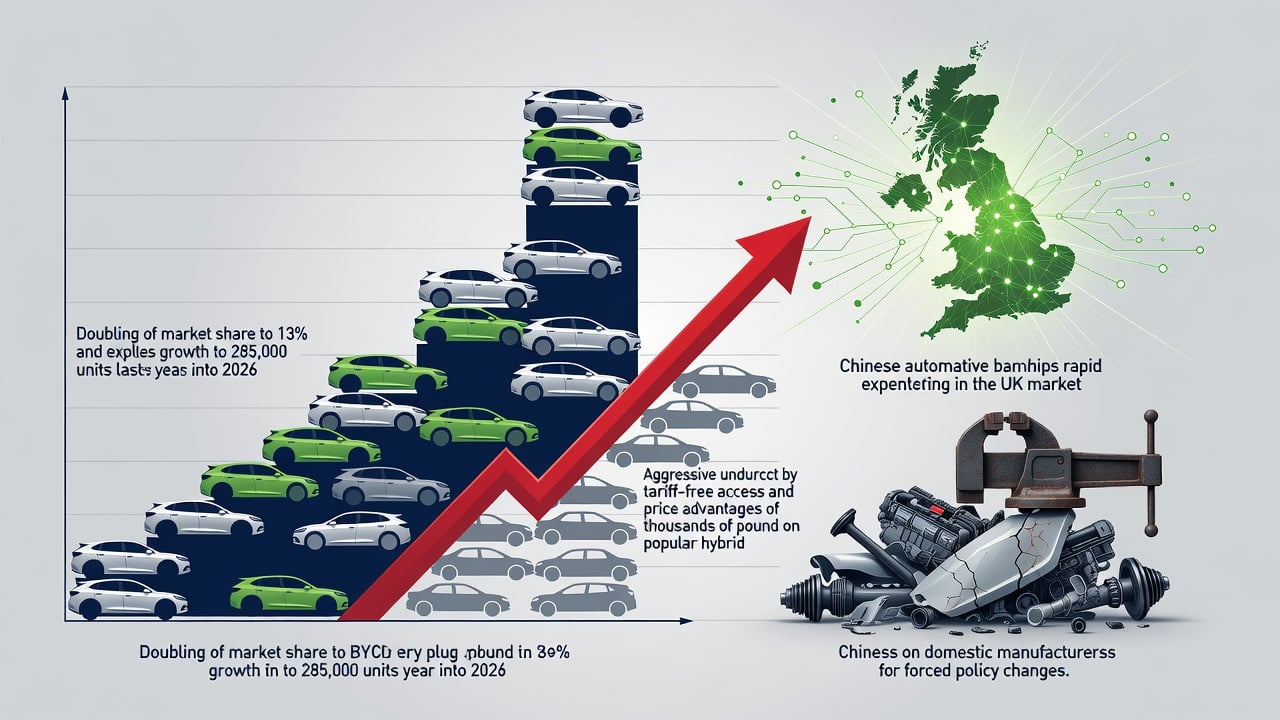

Overall the UK new-car market climbed 7 percent in May to 160,662 registrations, its strongest performance for the month since before the pandemic. Battery-electric vehicles claimed more than 27 percent of that total. Chinese brands now command about 13 percent of all new-car sales in Britain, double their share from the previous year. Some months they have taken as much as one-fifth of the market.

The explanation sits in plain view. Britain never followed the European Union’s decision to impose tariffs of up to 35.3 percent on Chinese battery-electric vehicles. Nor has it moved against plug-in hybrids. The United States went further with 100 percent duties. Canada capped imports. The UK left its doors open. That single policy difference redirected export flows that might otherwise have faced heavy penalties across the Channel.

Will Roberts, head of automotive at Benchmark, put it directly. “It becomes an excellent size market that’s progressing well towards electrification and is in demand for some cheaper vehicles with that void to fill.” His observation captures the commercial logic at work. A Volkswagen Tiguan plug-in hybrid lists for around £43,000 in Britain. The comparable BYD Seal U undercuts it by nearly £10,000 while offering more standard equipment. Buyers notice.

At a Geely dealership in Maidstone the value equation feels obvious. Shoppers compare specifications, glance at the sticker price, and drive out in cars that would have cost thousands more from traditional marques. The pattern repeats nationwide. Chinese automakers arrived with attractive designs, generous feature lists, and aggressive pricing. European incumbents suddenly looked expensive.

Domestic pressure inside China adds momentum. Sales at home dropped 26 percent in the first half of 2026. Exports jumped 72 percent according to the China Association of Automobile Manufacturers. Overcapacity that once threatened Chinese factories now finds an outlet in permissive markets like Britain. Geely stopped opening new plants and instead routes production through its Volvo facilities in Europe to skirt tariffs where they exist. The strategy absorbs excess capacity while keeping costs low.

Jon McNeill, a former executive at General Motors, watched the influx with clear eyes. Chinese automakers, he said, are entering Europe with cars that look attractive, carry attractive prices, and contain technology that blows away what many European manufacturers offer. The remark lands harder when sales data backs it up. In the first four months of 2026 Chinese brands delivered nearly 87,500 vehicles and captured 14.2 percent of UK registrations, eclipsing Japanese rivals in total volume.

April brought another milestone. Chinese-owned marques took more than a fifth of the entire new-car market that month. Their year-to-date share hovered near 20 percent. March registrations told the same story: Chinese brands tightened their grip and began squeezing established competitors. By the first quarter Chinese makers represented 11.12 percent of new vehicle registrations, up from 6.41 percent a year earlier. In EVs the penetration runs deeper. One analysis suggests Chinese brands now account for roughly one in three electric vehicles sold in Britain.

Tesla felt the shift. The American maker posted a 45 percent monthly sales increase in May yet its year-to-date figures rose only 3 percent. In February Tesla sales in the UK fell more than 45 percent year on year to 2,208 cars. BYD, meanwhile, has already overtaken Tesla globally with 2.26 million electric vehicles delivered in an earlier period. The competitive pressure is real and growing.

Yet the UK’s open-door policy may not survive indefinitely. As Chinese market share climbs, pressure mounts to align more closely with EU tariff rules. Industry groups and domestic manufacturers watch the numbers with concern. Britain’s own carmaking base, already strained, risks further erosion if the influx continues unchecked. For now the numbers tell their own story. Nearly 200,000 Chinese-brand cars changed hands in the UK during 2025, double the volume from the prior year. Early 2026 data points to another substantial increase.

Consumers appear unfazed by the provenance. They want lower running costs, modern technology, and competitive finance deals. Chinese makers deliver on all three. Many models come with long warranties, over-the-air updates, and advanced driver-assistance systems as standard. Traditional dealers scramble to match the packages.

The SMMT, Britain’s Society of Motor Manufacturers and Traders, records the monthly tallies. Its May report showed Ford’s Puma still leading overall sales, but Jaecoo’s 7 cracked the top five with 3,027 registrations. The presence of Chinese nameplates in such company would have seemed improbable only a few years ago. Today it looks routine.

Analysts debate how long the tariff advantage will last. European politicians continue to press for protective measures. Britain’s government faces a balancing act: keep electric-vehicle adoption affordable for drivers or shield local jobs and manufacturing investment. The choice grows sharper as Chinese volume expands.

Geely’s approach illustrates the sophistication behind the surge. By leveraging existing European plants through its Volvo ownership, the company sidesteps some trade barriers while still delivering competitively priced vehicles. Other Chinese groups pursue similar hybrid manufacturing strategies. The result blurs lines between “Chinese” and “European” production in ways regulators struggle to untangle.

Recent coverage highlights the speed of change. The Guardian reported that Chinese manufacturers drove much of May’s post-Covid sales peak. The Car Expert documented how BYD and Chery squeezed rivals in March. Even earlier data from The Next Web traced the tariff gap’s decisive role in redirecting shipments away from protected markets.

Industry veterans recall previous waves of import competition. Japanese brands arrived in the 1970s and 1980s with reliable, fuel-efficient cars. South Korean makers followed with strong value propositions. The Chinese wave carries larger scale, faster technological progress, and explicit state support at home. Its impact on the broader European auto sector already shows in underused plants and shifting investment plans.

British buyers, for their part, keep voting with their wallets. They fill showrooms, compare specs on phones, and sign contracts for vehicles that undercut rivals by thousands of pounds. The math works. The cars arrive equipped. Service networks expand to meet demand. What began as a niche experiment now reshapes the mainstream market.

Questions remain about long-term reliability, resale values, and the geopolitical risks of heavy dependence on any single supply chain. Those concerns surface in boardrooms and policy discussions but have not yet slowed the registrations. Data from the first half of 2026 suggests momentum continues to build. Chinese brands could approach 20 percent of the full-year UK market if current trends hold.

The story extends beyond simple market share. It reflects a global industry in flux. Overcapacity in China meets pent-up demand for affordable electrification in Britain. The absence of tariffs acts as a catalyst. European manufacturers respond with their own cost-cutting and technology upgrades, yet the price gap persists in many segments.

So the inflow continues. Dealers adapt. Consumers benefit from choice and lower prices. Policymakers weigh trade-offs. And the numbers keep climbing, month after month, model after model. The British car market of 2026 looks markedly different from the one that existed a decade ago. Chinese marques no longer sit on the periphery. They occupy the center of the sales charts and the center of the strategic conversation.