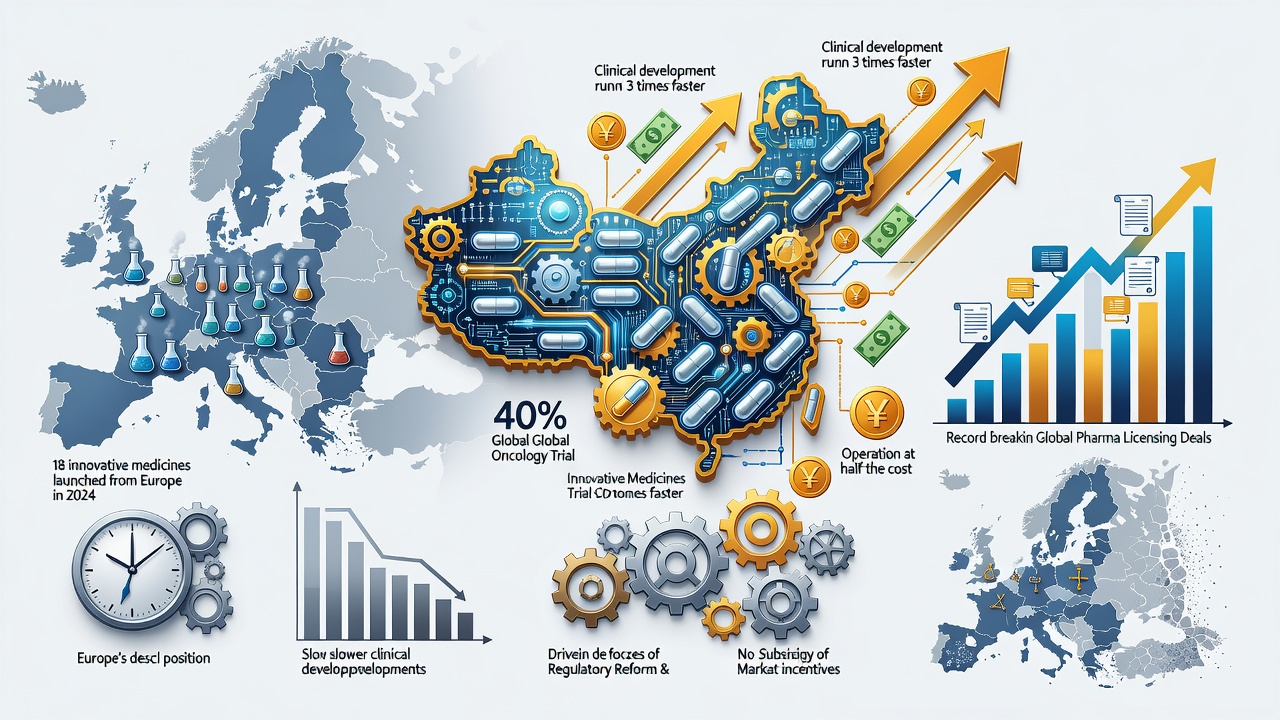

Alexandre de Germay delivered the message with striking clarity. Speaking at an industry gathering in Brussels this June, the Pfizer chief international commercial officer declared that China has moved ahead of Europe in pharmaceutical innovation and drug development. The numbers he cited painted a picture of rapid ascent. In 2024, 28 of 81 innovative medicines launched worldwide originated from China. Europe contributed just 18. And today, 40% of all oncology clinical studies globally take place in China.

De Germay didn’t stop at the headlines. He noted that clinical development runs three times faster in China. Costs sit at roughly half those seen in Europe. “The volume of innovation that is coming out of biotech in China is just amazing,” he said, according to a Reuters report. “We have to compete with the U.S., but we also have to compete with China. The threat of China is reality.”

His remarks, delivered to European pharmaceutical leaders, carried weight. They arrived amid mounting evidence that the balance of power in global drug discovery has shifted. Once viewed primarily as a market for Western medicines or a source of generics, China now generates original science at scale. Its biotechs file novel candidates. They run trials at speed. They strike licensing deals worth billions with the same companies that once dismissed them.

The transformation traces back more than a decade. Regulatory reforms launched in 2015 slashed approval backlogs and aligned China with international standards. The National Medical Products Administration accelerated reviews. Clinical trial applications that once took months now clear in weeks. Yet the deeper force may have been market incentives. A 2016 overhaul of the National Reimbursement Drug List expanded access and rewards for innovative therapies. According to research from Stanford’s Asia Health Policy Program, this reform explains 43% of the post-2015 surge in oncology trials. Industrial subsidies such as those under Made in China 2025 played only a marginal role.

Data from the Stanford analysis underscore the scale. In 2010, China accounted for less than 8% of global clinical trials. By 2020 it had surpassed the United States in annual registered trial volume. The count reached over 5,000 trials per year by 2024, a 172% increase relative to the U.S. Importantly, the quality holds. Three separate measures of novelty — one based on mechanism of action, another on new molecular entities identified by artificial intelligence, and a third focused on Phase 3 trials against innovative benchmarks rather than placebos — all show gains of 49% to 123% compared with American activity. Out-licensing deals to multinational firms doubled. First-in-world regulatory approvals for Chinese-developed drugs rose 36%. New firm entry grew 27%. Domestic Chinese companies drove 88% of the post-2015 increase.

These trends appear in other recent assessments. A January 2026 analysis from ING Economics found Europe’s share of started clinical trials had nearly halved, falling from roughly 35% in 2009 to 20% in 2024. Its portion of global new drug approvals dropped from 20% in 2015 to 10% in 2024. China, meanwhile, surpassed Europe in approvals and continues to close the gap with the United States. Chinese pharmaceutical R&D spending grew at an average annual rate of 20.7% from 2010 to 2022, far outpacing the 5.5% recorded in the U.S. and 4.4% in the EU. Forecasts point to continued divergence. China’s R&D outlays are projected to expand at an 8% compound annual growth rate through 2030. The comparable figures sit at 5% for the U.S. and 4% for Europe.

Antibody therapeutics illustrate the advance. A November 2025 paper in Nature Reviews Drug Discovery documented how Chinese companies have flooded the clinic with sophisticated molecules — antibody-drug conjugates, bispecifics, multispecifics. The number of enhanced antibodies from Chinese sponsors entering studies since 2020 now exceeds the combined total from U.S. and European firms. Success rates appear higher too. Phase 1 assets originating in China show markedly better transition probabilities than their Western counterparts in some datasets.

Big Pharma has taken notice. Licensing volumes tell the story. Chinese biotechs generated a record $137.7 billion in out-licensing value in 2025, according to a February 2026 Reuters analysis. The pace has only accelerated into 2026. Pfizer itself paid a record $1.25 billion upfront to China’s 3SBio for a PD-1/VEGF bispecific cancer immunotherapy. Other deals have followed in oncology, metabolic disease and immunology. “Things are cheaper and faster,” one industry executive told The Wall Street Journal in an April 2026 feature on the shift.

The patient population helps explain the velocity. China offers dense concentrations of treatment-naive patients, particularly in oncology. Regulatory timelines have compressed dramatically. Median time from application to first-in-human approval fell from more than 500 days before 2015 to 87 days today. Trials that stretch two years in the West often wrap in nine months. These advantages compound. Faster enrollment. Quicker data readouts. Earlier decisions to advance or kill programs.

Yet challenges remain. Overcapacity plagues certain classes. More than 20 PD-1/PD-L1 inhibitors have won approval in China, creating intense domestic price pressure. Many assets still must prove themselves in global, multiregional trials to secure Western approvals and reimbursement. Quality concerns linger in some quarters. A recent survey of U.S. biotech leaders, reported by Reuters in June 2026, found that while China leads in clinical development speed and supply chain execution, the United States retains advantages in basic research quality and commercial reach. Most respondents nevertheless believe the U.S. lead will erode within a decade.

Europe faces a steeper climb. Its clinical trial infrastructure has eroded. Funding constraints bite. Regulatory complexity slows progress. The continent once claimed a robust share of early-phase innovation. That position has slipped. Several recent reports, including one from the European Federation of Pharmaceutical Industries and Associations, document declining participation in cell and gene therapy trials even as China’s involvement has surged. Without meaningful policy adjustments — faster approvals, better incentives, harmonized data standards — the gap may widen.

The United States has begun to respond. The FDA launched Operation TrialBlazer to accelerate early-stage research and simplify trial designs. Pfizer’s own data show that at least 20% of patients in its late-stage oncology studies now come from the U.S., a figure executives hope to grow. Still, the momentum in Asia is hard to ignore. A July 2025 Bloomberg feature described Chinese biotech’s advance as “ferocious,” eclipsing Europe and narrowing the distance to American leadership in both volume and sophistication.

What does this mean for patients and investors? More innovation from a broader set of sources should accelerate new therapies for cancer, autoimmune disorders, metabolic disease and rare conditions. Bispecific antibodies. Novel ADCs. Dual and triple agonists in obesity and diabetes. Some of the most promising molecules in these categories now carry Chinese origins. Global licensing ensures they reach patients faster than if they remained domestic-only assets.

Supply chain questions loom larger. Geopolitical tensions have already prompted scrutiny. The Pentagon’s addition of WuXi AppTec to a list of companies with alleged military ties in June 2026 sent ripples through contract development and manufacturing organizations. U.S. lawmakers continue to debate measures that could restrict reliance on Chinese-made active pharmaceutical ingredients. Yet the innovation pipeline flows both ways. Western firms need Chinese science. Chinese firms need Western capital, regulatory expertise and commercial infrastructure.

The shift did not happen overnight. It built on policy changes, entrepreneurial energy, scientific talent returning from abroad and a vast domestic market that rewards novelty. The 2015 regulatory overhaul removed a massive backlog and introduced priority review pathways. Alignment with International Council for Harmonisation guidelines gave global regulators confidence in Chinese-generated data. Companies such as Akeso, Innovent, Legend Biotech and BeiGene moved from fast followers to originators of first-in-class molecules. Ivonescimab, a PD-1/VEGF bispecific from Akeso, posted impressive progression-free survival data against Merck’s Keytruda in a Chinese lung cancer study. Mazdutide, a dual agonist from Innovent, secured approval in China as a potential first-in-class therapy for weight management and diabetes.

These examples are no longer outliers. A 2025 Nature Reviews Drug Discovery article tracking the decade from 2015 to 2024 described a “decade of innovation” in which Chinese sponsors transformed from bit players to major contributors. The pipeline now spans oncology, immunology, neurology and cardiometabolic disease. Artificial intelligence tools accelerate target identification and molecule design. High-throughput screening platforms operate at volumes once unimaginable outside a few Western hubs.

For European pharmaceutical executives, the Pfizer warning lands as both diagnosis and call to action. The continent retains strengths in basic science, particularly in academic centers in Germany, the U.K., Switzerland and Scandinavia. It boasts deep expertise in complex chemistry and advanced manufacturing. But those advantages erode if promising candidates never reach the clinic or if trials migrate elsewhere. Several industry groups have urged reforms to the EU Clinical Trials Regulation, faster reimbursement decisions and increased public-private funding for early development.

The data continue to accumulate. Recent analyses from Novotech and other contract research organizations show China initiating more than 1,250 novel drug candidates in 2024, surpassing the EU and approaching U.S. levels. Oncology remains the dominant focus, but diversification is underway. The volume of first-in-human studies continues to climb. So does the number of Chinese sponsors running trials in the U.S. and Europe to generate data acceptable to the FDA and EMA.

So the competitive landscape has changed. What was once a story of catch-up has become one of leadership in selected domains. China’s rise does not guarantee dominance. Regulatory hurdles abroad, quality standardization, intellectual property enforcement and geopolitical risk all impose limits. But the trajectory is clear. Innovation now flows from East to West as well as the reverse. Pfizer’s de Germay put it plainly. The threat is reality. Companies that fail to engage with the new reality risk falling behind. Patients, meanwhile, stand to gain from a broader and faster pipeline of new medicines. The question is no longer whether China matters in global drug innovation. It is how the rest of the world will adapt to a landscape it now helps define.