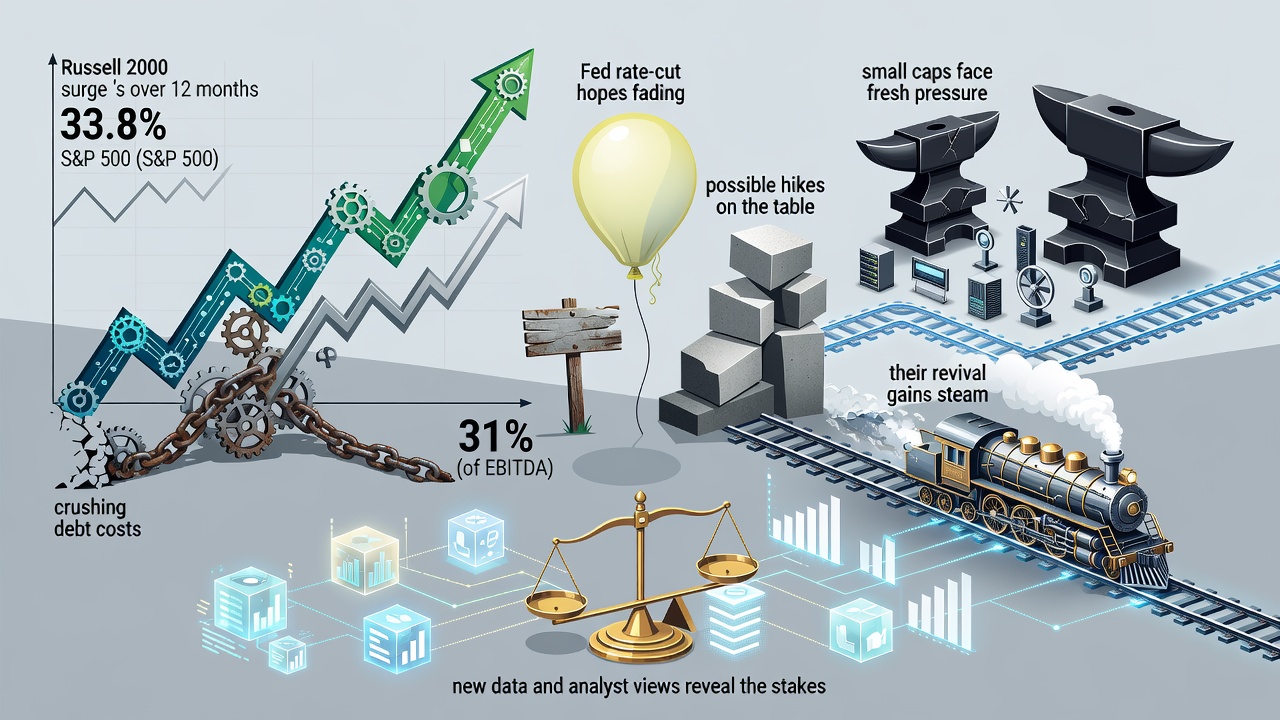

The Russell 2000 has roared ahead. Up 33.8% over the past 12 months. That beats the S&P 500’s 20% gain by a wide margin. Bull markets thrive on such breadth. Yet this surge carries an uneasy tension. Small companies shoulder far heavier debt loads than their larger peers. High borrowing costs should have crushed them. Somehow, they haven’t. Not yet.

Interest expense now devours 31% of EBITDA among Russell 2000 constituents. Double the level from 2020. Nearly 30% of that debt floats with short-term rates. Compare that to the S&P 500, where interest eats just 6.7% of EBITDA and floating-rate exposure sits near 7%. More than 40% of small-cap firms remain unprofitable. Only about 6% of large caps do. These gaps explain why many analysts predicted small caps would lag until the Federal Reserve eased policy. The rally defied those forecasts anyway. But the ground may be shifting.

Fed Policy Tightens Its Grip on Smaller Borrowers

Data compiled by Bloomberg and Apollo Global Management paints a stark picture. The figures come straight from a Yahoo Finance analysis published today. Small firms lack the cash buffers, credit ratings and capital-market access that let giants absorb rate pain. When the Fed held rates elevated to fight inflation, investors braced for weakness in the small-cap arena. Economic growth stayed resilient. Inflation cooled more slowly than hoped. Rate-cut expectations that dominated 2025 have now faded sharply.

Markets once penciled in several reductions for 2026. Recent signals point elsewhere. Some traders now assign meaningful odds to steady policy or even hikes if price pressures reaccelerate. New Chair Kevin Warsh stressed price stability at the June meeting, according to a U.S. Bank report from June. The median projection from officials called for one to two rate increases this year. The committee appeared divided. That uncertainty weighs heaviest on companies already stretched by floating-rate obligations.

But small caps have outperformed in 2026 so far. The Morningstar US Small Cap Market Index beat the broad market by more than three percentage points in the first half, per a Morningstar update from three days ago. Leadership broadened. Earnings recovery gained traction. Credit spreads stayed narrow. Banks eased lending caution after the worst of the rate-hike cycle passed. Those tailwinds helped the Russell 2000 build on gains even as policy expectations hardened. Momentum feels real. Fragile, too.

Chip Skinner of Royce Investment Partners expressed constructive views on small-cap growth stocks heading into this year. He pointed to accommodative fiscal and monetary policies plus onshoring initiatives. The comments appear in a Royce report from late 2025 that still resonates. Accelerated earnings growth forecasts for 2026 offered further support. Recent Fed cuts provided relief. Additional catalysts such as capex cycles, tariff adjustments and reshoring activity could amplify the lift. Yet those assumptions rested on continued easing. Today’s outlook looks less certain.

RiverFront Investment Group analysts highlighted that higher short-term rates had dragged on small-cap earnings since 2022. Their September 2025 analysis argued a dovish policy shift would deliver a clear tailwind. Small caps historically deliver stronger long-term returns when rates fall. The firm’s Price Matters framework showed small caps trading 23.4% below trend while large caps sat 37% above. Value alone does not guarantee outperformance. Earnings growth must follow. Early green shoots appeared last year. Persistent high rates could trample them.

Recent X discussions reflect the shift in sentiment. One trader noted markets now price in 80% odds of zero cuts in 2026 while small-cap floating-rate debt accumulates. Another highlighted how rate-cut expectations had fueled the rally until inflation data complicated the picture. Posts from the past week capture real-time anxiety. The relationship between Fed policy and small-cap performance appears to have weakened temporarily. Confidence in earnings recovery explains some of the decoupling. That confidence faces a test if borrowing costs stay sticky.

Smaller businesses depend more on bank loans and short-term financing. When the Fed began cutting toward the end of 2025, even though policy remained restrictive overall, markets sensed the peak pressure had passed. Volatility cooled. Lending conditions improved gradually. The Russell 2000 responded with vigor. Its one-year gain now exceeds 30% in some measures, according to a Small Cap Informer review posted five days ago. The S&P SmallCap 600 mirrored that strength. Outperformance versus large caps held firm through the first half of 2026. The index sits at elevated levels but still reflects a leadership rotation many had awaited for years.

The risks remain concrete. Over 40% of Russell 2000 companies post losses. Floating-rate exposure leaves them exposed to any reversal in rate-cut bets. A single hike or prolonged pause could lift interest expense further. Profit margins would compress. Valuations already reflect optimism about easing. Any disappointment might trigger sharp reversals. Large caps, with stronger balance sheets and more fixed-rate debt, would likely weather the storm with less drama. Market breadth could narrow again. The broadening that cheered investors might prove short-lived.

Analysts at Franklin Templeton and Royce flagged onshoring, infrastructure spending and AI-related projects as supportive themes for small-cap suppliers. Those secular forces endure. They do not erase the cyclical pressure from monetary policy. Fiscal spending tied to industrial policy offers another buffer. Yet monetary conditions set the immediate tone for borrowing costs. Investors watch the Fed’s next moves with heightened focus. Inflation readings, labor data and energy prices will shape the path. So will communication from Warsh and colleagues.

Small-cap stocks still appear slightly undervalued on Morningstar’s metrics at the end of June. Volatility stays a constant companion. Concerns about potential rate hikes this year keep many on edge. Selective stock picking becomes critical. Companies with economic moats, improving profitability and limited floating-rate debt stand a better chance. Those providing components for AI infrastructure or benefiting from reshoring may find structural demand that offsets higher financing costs. The rest face tougher arithmetic.

The revival arrived against heavy odds. Small firms posted stronger returns despite the highest interest burden in years. That resilience deserves credit. It also raises the stakes. If the Fed holds firm or tightens further, the squeeze could intensify. Profits would suffer. Momentum might stall. The broadening bull market that many waited years to see would lose its foundation. Investors who piled into small caps on hopes of easier policy now confront a narrower window. The data, the debt loads and the policy signals all point to caution. The rally’s next chapter depends on forces beyond corporate control. The Federal Reserve holds the pen.