China’s electric vehicle industry, long heralded as the vanguard of global automotive transformation, faces a moment of reckoning as BYD Company Limited reported its weakest sales performance in nearly two years. The development marks a pivotal shift in market dynamics that industry analysts warn could reshape competitive positioning across the world’s largest automotive market.

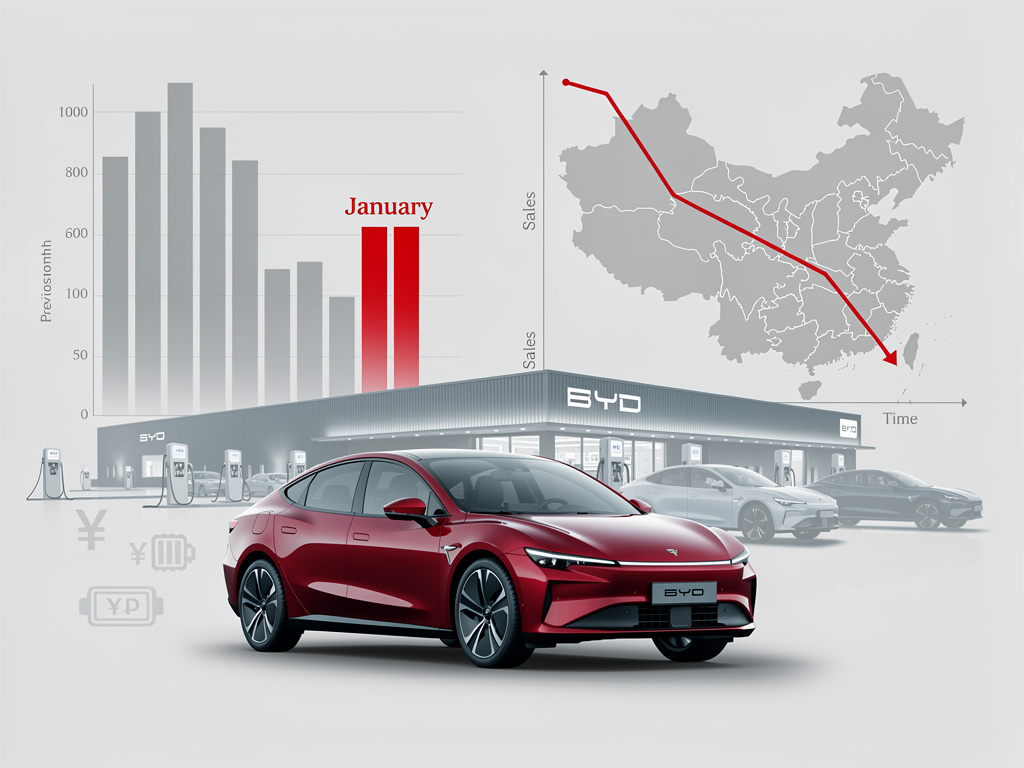

According to CNBC, BYD’s January sales figures revealed a significant contraction, with deliveries falling to levels not seen since early 2024. The Shenzhen-based automaker, which has consistently challenged Tesla’s global dominance, sold approximately 201,000 vehicles in January, representing a 32% decline from December’s figures and a concerning year-over-year decrease that has sent ripples through investor communities and supply chain partners alike.

The sales deterioration extends beyond typical seasonal fluctuations that characterize the Chinese automotive market. Industry observers point to a confluence of factors including macroeconomic headwinds, shifting consumer sentiment, and an increasingly saturated domestic market where price competition has eroded profit margins across virtually all segments. BYD’s struggle comes despite the company’s aggressive expansion into international markets and its diversified product portfolio spanning both battery electric vehicles and plug-in hybrids.

Market Saturation and Consumer Hesitation Create Perfect Storm

The broader Chinese electric vehicle sector experienced parallel challenges throughout the first month of 2026, with aggregate sales data indicating a systemic slowdown rather than company-specific difficulties. Multiple manufacturers reported declining deliveries, suggesting that fundamental market conditions have shifted from the explosive growth trajectory that characterized the previous five years. The China Passenger Car Association’s preliminary data indicates that overall new energy vehicle sales, which include both pure electric and plug-in hybrid models, contracted by approximately 18% in January compared to the previous month.

Consumer behavior patterns reveal growing caution among potential buyers, influenced by economic uncertainty and concerns about residual values of electric vehicles in an increasingly crowded marketplace. The proliferation of new models and brands has paradoxically created decision paralysis among consumers, while aggressive price cuts initiated by established players have conditioned buyers to anticipate further discounts, delaying purchase decisions indefinitely. This psychological shift represents a fundamental challenge to the growth assumptions that have underpinned industry expansion plans and government policy frameworks.

Government Policy Recalibration Adds Regulatory Uncertainty

Beijing’s evolving approach to electric vehicle subsidies and incentives has introduced additional complexity into market dynamics. While the central government remains committed to electrification goals, the gradual phase-out of direct consumer subsidies has removed a significant demand stimulus that previously masked underlying market vulnerabilities. Local governments, facing fiscal constraints, have similarly reduced or eliminated regional incentive programs that once provided substantial purchase support.

The regulatory environment has simultaneously tightened around safety standards and quality requirements, increasing compliance costs for manufacturers while potentially slowing new model introductions. These policy adjustments reflect government concerns about industry overcapacity and the financial sustainability of the electric vehicle ecosystem, including charging infrastructure operators and battery recycling facilities. Industry participants privately acknowledge that the era of policy-driven growth has concluded, necessitating fundamental business model adaptations focused on organic demand generation and operational efficiency.

International Expansion Strategy Faces Mounting Obstacles

BYD’s international ambitions, conceived as a strategic hedge against domestic market saturation, encounter increasingly formidable barriers across key target markets. European Union investigations into Chinese electric vehicle subsidies have culminated in provisional tariffs that significantly impact pricing competitiveness, while political resistance to Chinese automotive imports has intensified across multiple jurisdictions. The company’s planned manufacturing facilities in Thailand, Brazil, and Hungary represent attempts to circumvent trade barriers through localized production, but these investments require substantial capital commitments with uncertain return timelines.

North American market access remains particularly challenging, with geopolitical tensions and national security concerns effectively precluding direct vehicle sales in the United States despite BYD’s technological capabilities and cost advantages. The company’s focus on markets in Southeast Asia, Latin America, and select European countries reflects pragmatic recognition of these constraints, though these regions collectively represent smaller addressable markets with lower average transaction values compared to developed Western economies.

Supply Chain Pressures and Raw Material Volatility

The electric vehicle supply chain confronts persistent challenges related to raw material availability and price volatility, particularly for critical battery components including lithium, cobalt, and nickel. While recent months have seen some stabilization in commodity prices following the extreme spikes of 2022 and 2023, structural supply constraints remain evident as global electrification accelerates across transportation and energy storage applications. BYD’s vertical integration strategy, including its proprietary battery production through subsidiary FinDreams, provides some insulation from supply chain disruptions but cannot fully eliminate exposure to underlying commodity market dynamics.

Battery technology evolution introduces additional complexity, with solid-state and alternative chemistry developments potentially rendering current manufacturing investments obsolete within shortened timeframes. Industry participants face difficult capital allocation decisions balancing continued investment in lithium-ion production capacity against emerging technologies that promise superior performance characteristics but remain unproven at commercial scale. This technological uncertainty compounds financial pressures created by declining vehicle prices and compressed margins.

Competitive Dynamics Intensify Across All Segments

The Chinese electric vehicle market’s maturation has precipitated brutal competition across price points and vehicle categories, with more than 100 brands actively competing for consumer attention. Traditional automotive manufacturers including Volkswagen, General Motors, and Toyota have accelerated their electrification efforts in China, leveraging established dealer networks and brand recognition to recapture market share lost to domestic specialists. Meanwhile, technology companies including Xiaomi and Huawei have entered the automotive sector, bringing software expertise and ecosystem integration capabilities that appeal to digitally-native consumers.

This competitive intensity has triggered multiple price wars throughout 2025, with successive rounds of discounting eroding profitability across the industry. BYD, despite its scale advantages and vertical integration, has not remained immune to margin pressure, with average selling prices declining even as raw material costs stabilize. The company’s strategy of maintaining market share through competitive pricing reflects management’s assessment that volume leadership remains essential for long-term viability, even at the expense of near-term profitability.

Infrastructure Gaps Continue Limiting Adoption

Despite substantial investment in charging infrastructure, significant gaps persist in network coverage and reliability, particularly in lower-tier cities and rural areas where electric vehicle adoption remains nascent. Range anxiety continues influencing purchase decisions, especially for consumers lacking dedicated home charging capabilities. The uneven distribution of charging stations creates geographic pockets where electric vehicle ownership remains impractical, limiting addressable market expansion beyond major metropolitan areas.

Charging network operators face challenging unit economics, with utilization rates often insufficient to justify infrastructure investments without continued government support. The proliferation of incompatible charging standards and payment systems further complicates user experience, creating friction that advantages traditional internal combustion vehicles. Resolution of these infrastructure challenges requires coordinated action among automakers, energy companies, and government entities, with timeline uncertainty affecting consumer adoption trajectories.

Financial Markets Reassess Growth Assumptions

Investor sentiment toward Chinese electric vehicle manufacturers has cooled considerably as sales growth decelerated and profitability concerns intensified. BYD’s stock price has experienced significant volatility, with valuation multiples contracting from peak levels as analysts revise downward their growth projections and question the sustainability of current business models. The repricing extends across the sector, affecting both established manufacturers and newer entrants, with capital markets demonstrating increased skepticism toward companies lacking clear paths to profitability.

This reassessment reflects broader concerns about the Chinese economy’s growth trajectory and consumer spending capacity amid property sector challenges and employment uncertainty. The automotive sector’s sensitivity to macroeconomic conditions amplifies these concerns, with electric vehicles particularly vulnerable given their higher average transaction prices relative to comparable internal combustion models. Financial market discipline may ultimately prove beneficial by forcing industry consolidation and eliminating overcapacity, though the adjustment process promises to be painful for stakeholders across the value chain.

Strategic Implications for Global Automotive Industry

The Chinese electric vehicle market’s deceleration carries profound implications for global automotive strategy and investment priorities. Western manufacturers that have committed substantial resources to electrification based partly on Chinese market growth assumptions must now recalibrate their plans and potentially adjust production capacity allocations. The experience demonstrates that electric vehicle adoption trajectories remain uncertain and highly dependent on policy support, infrastructure availability, and consumer acceptance factors that vary significantly across markets.

For policymakers in Europe and North America, China’s experience offers cautionary lessons about the challenges of managing automotive industry transitions and the risks of overcapacity creation through aggressive industrial policy. The delicate balance between supporting domestic industry development and avoiding unsustainable market distortions remains elusive, with optimal policy frameworks likely varying based on specific national circumstances and competitive positions. As the global automotive industry navigates its most significant transformation in generations, China’s electric vehicle market evolution will continue providing critical insights into the opportunities and pitfalls that lie ahead for all participants in this fundamental industrial restructuring.