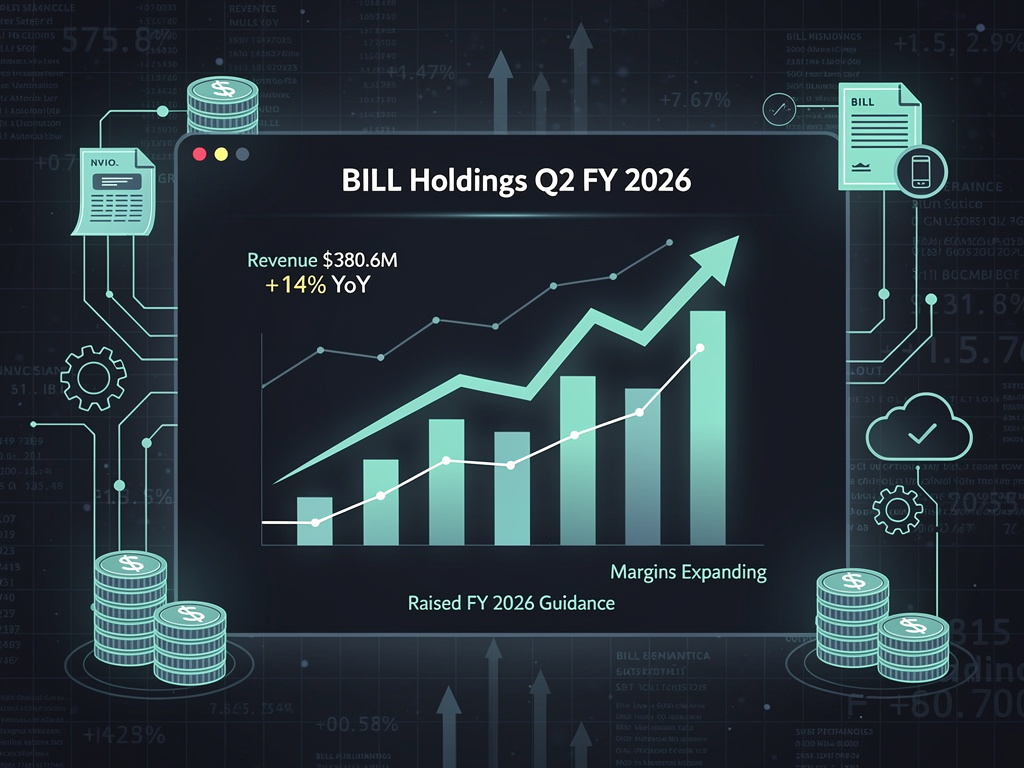

BILL Holdings Inc., the financial automation platform that has become a linchpin for small and midsize businesses managing their back-office operations, reported second-quarter fiscal year 2026 results that exceeded Wall Street expectations on virtually every metric. The San Jose, California-based company posted total revenue of $380.6 million, a 14% year-over-year increase, while delivering non-GAAP net income of $111.5 million — a performance that underscores the company’s successful pivot from a growth-at-all-costs model to one that marries expansion with profitability.

The results, announced via BusinessWire, paint a picture of a company that has found its stride in an increasingly competitive fintech sector. Core revenue, which encompasses subscription and transaction fees from the company’s flagship accounts payable and receivable platform, climbed 18% year-over-year to $283.5 million. Total payment volume processed through the platform reached $85.0 billion for the quarter, up 13% from the prior-year period. Perhaps most notably, the company served approximately 481,800 businesses using its solutions, a figure that reflects the platform’s deepening penetration into the SMB market.

A CEO’s Vision for the Next Phase of Growth

BILL’s founder and CEO, René Lacerte, struck an optimistic tone in his commentary accompanying the results. “We are off to a great start to the second half of our fiscal year. Our results reflect continued momentum across our platform as we deliver innovation that simplifies financial operations for SMBs,” Lacerte said, as quoted in the company’s earnings release on BusinessWire. “Our AI-powered platform is transforming how businesses manage their financial operations, and we are excited about the opportunities ahead.”

The emphasis on artificial intelligence is not mere corporate boilerplate. BILL has been systematically embedding AI capabilities across its platform, from intelligent invoice processing and payment routing to fraud detection and cash flow forecasting. The company’s investments in these areas appear to be paying dividends, both in terms of customer retention and in driving higher transaction volumes per user. The 18% growth in core revenue outpaced the 13% growth in total payment volume, suggesting that the company is successfully extracting more value per dollar processed — a key indicator of pricing power and product stickiness.

Profitability Metrics Signal a Maturing Business Model

The profitability story at BILL is becoming increasingly compelling for institutional investors. Non-GAAP gross profit for the second quarter came in at $326.7 million, representing an 85.9% gross margin — a figure that would be the envy of most enterprise software companies, let alone a fintech firm that processes tens of billions in payment volume. Non-GAAP income from operations reached $83.3 million, yielding an operating margin of 21.9%, up from 16.3% in the year-ago quarter. This 560-basis-point expansion in operating margin demonstrates the significant operating leverage inherent in BILL’s platform model.

On a GAAP basis, the company reported net income of $34.8 million, or $0.37 per diluted share, compared to a net loss of $7.7 million, or a loss of $0.08 per share, in the second quarter of fiscal year 2025. The swing from GAAP loss to GAAP profitability is a milestone that many high-growth software companies struggle to achieve, and it positions BILL favorably among investors who have grown weary of unprofitable technology firms. Non-GAAP net income per diluted share came in at $1.15, a robust figure that reflects the company’s disciplined approach to stock-based compensation and other non-cash expenses.

Cash Generation and Balance Sheet Strength

Free cash flow for the quarter was $117.2 million, a 44% increase from $81.3 million in the prior-year period, according to the company’s earnings release. Non-GAAP free cash flow reached $128.3 million, representing a non-GAAP free cash flow margin of 33.7%. This level of cash generation provides BILL with significant strategic flexibility, whether for organic investment, acquisitions, or shareholder returns. The company ended the quarter with $1.8 billion in total short-term investments and funds held for customers, providing a substantial liquidity cushion.

The company’s capital allocation strategy has included an aggressive share repurchase program. During the second quarter, BILL repurchased approximately 2.3 million shares of its common stock for $175.0 million at an average price of approximately $76.05 per share. As of December 31, 2025, approximately $266.3 million remained available under the company’s existing $500 million share repurchase authorization. This buyback activity signals management’s confidence in the stock’s intrinsic value and serves to offset dilution from equity-based compensation — a persistent concern among fintech investors.

Revenue Composition Reveals Strategic Diversification

A closer examination of BILL’s revenue composition reveals a business that is becoming more diversified and resilient. Subscription revenue for the quarter was $70.7 million, up 6% year-over-year, reflecting steady growth in the company’s recurring software fees. Transaction revenue reached $212.8 million, a 22% increase, driven by higher payment volumes and improved monetization of the company’s payment rails. Float revenue, which is derived from interest earned on funds held on behalf of customers, contributed $54.7 million, down 4% from the prior year as interest rate dynamics shifted.

The relative decline in float revenue is worth noting. As the Federal Reserve has begun to adjust its monetary policy stance, the yield on customer funds has moderated. However, the 4% decline in float revenue was more than offset by the 22% surge in transaction revenue, demonstrating that BILL’s core business model is not overly dependent on the interest rate environment. This is a critical distinction for investors who may have worried that a significant portion of BILL’s earnings power was a byproduct of the elevated rate cycle rather than fundamental business performance.

Guidance Raises the Bar for the Second Half

Management’s forward guidance further bolstered investor confidence. For the third quarter of fiscal year 2026, BILL expects total revenue in the range of $381.5 million to $386.5 million, representing year-over-year growth of approximately 10% to 12% at the midpoint. Non-GAAP income from operations is expected to be between $71.0 million and $76.0 million. For the full fiscal year 2026, the company raised its revenue guidance to a range of $1.510 billion to $1.520 billion, up from prior guidance of $1.485 billion to $1.510 billion. Full-year non-GAAP operating income guidance was also raised to a range of $305.0 million to $315.0 million, up from the prior range of $280.0 million to $300.0 million.

The guidance raise is particularly significant because it comes against a backdrop of macroeconomic uncertainty that has weighed on many technology companies. Small and midsize businesses, which form BILL’s core customer base, have faced headwinds ranging from persistent inflation to tightening credit conditions. Yet BILL’s results suggest that its value proposition — automating tedious, error-prone financial workflows — becomes more compelling, not less, during periods of economic stress. When businesses are under pressure to do more with less, the case for automating accounts payable, accounts receivable, and expense management becomes self-evident.

The Competitive Dynamics Shaping BILL’s Future

BILL operates in a market that is both enormous and fiercely contested. The company competes with legacy accounting software providers, emerging fintech startups, and increasingly, with large financial institutions that are building their own digital payment and automation capabilities for business customers. Intuit, which owns QuickBooks, remains a formidable competitor, as do companies like Brex, Ramp, and Corpay, each of which has carved out a niche in the broader SMB financial services arena.

What distinguishes BILL is the breadth of its platform. The company’s ecosystem encompasses accounts payable automation through its core BILL platform, accounts receivable and invoicing through BILL Accounts Receivable, expense management through BILL Spend & Expense (formerly Divvy), and a comprehensive set of payment capabilities including ACH, virtual card, cross-border payments, and check. This integrated approach creates switching costs that are difficult for competitors to overcome, as businesses that adopt multiple BILL products become deeply embedded in the platform’s workflow.

AI Integration and the Road Ahead

The company’s investment in artificial intelligence represents what may be its most important strategic initiative. BILL has been deploying machine learning models to automate invoice coding, detect anomalies in payment patterns, and provide predictive insights into cash flow. These capabilities not only improve the user experience but also create a data flywheel: as more transactions flow through the platform, the AI models become more accurate, which in turn attracts more users and transactions. CEO Lacerte’s emphasis on AI-powered innovation in his quarterly commentary, as reported by BusinessWire, reflects a recognition that the next wave of competitive differentiation in fintech will be driven by intelligent automation rather than simple digitization.

The company’s approximately 481,800 business customers represent a fraction of the millions of SMBs in the United States alone, suggesting a long runway for growth. With a platform that is generating robust free cash flow, expanding margins, and demonstrating consistent revenue growth, BILL Holdings appears well-positioned to capitalize on the secular shift toward digital financial operations. For investors and industry observers alike, the second quarter results represent not just a strong earnings print, but evidence that BILL has successfully navigated the transition from high-growth disruptor to a sustainable, profitable platform company — without sacrificing its ambition to transform how businesses manage their money.