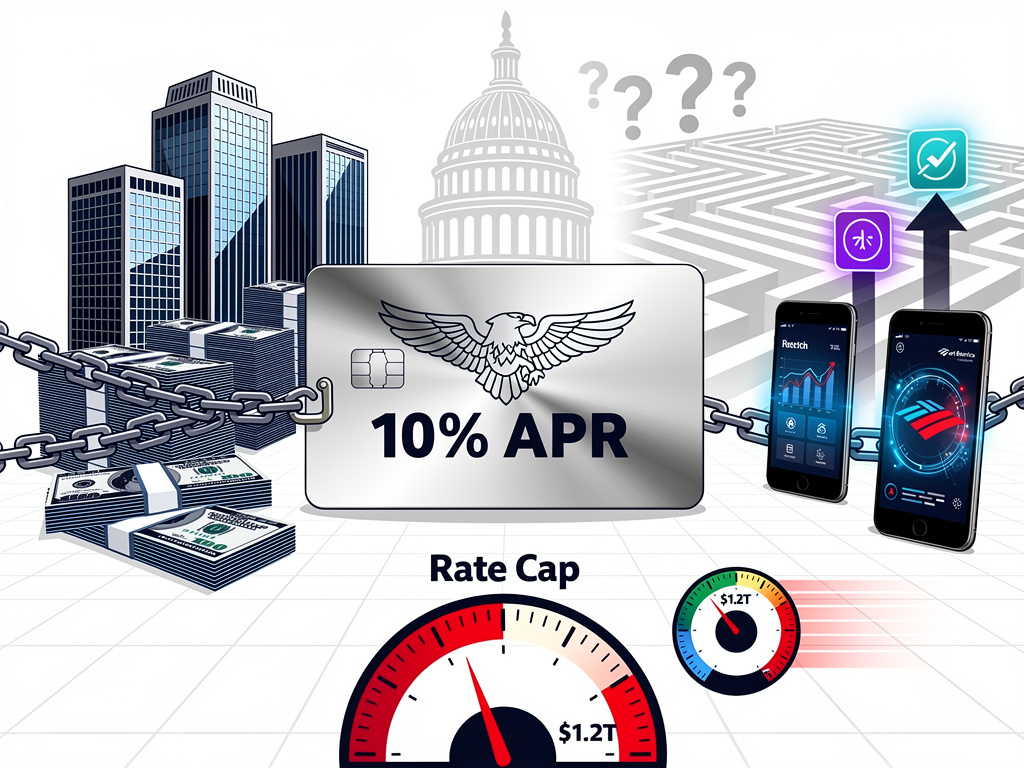

Bank of America Corp. is contemplating a new credit card capped at 10% interest, a direct response to President Donald Trump’s aggressive push for lower borrowing costs amid soaring consumer debt. Sources familiar with the bank’s internal discussions reveal that executives are exploring this no-frills product as a way to align with Trump’s directive, even as the industry warns of dire consequences for credit access. The move comes after Trump, in a January 9 Truth Social post, demanded a one-year 10% cap on credit card rates effective January 20, accusing issuers of ripping off Americans with rates up to 30%.

America’s credit card balances hit $1.2 trillion in the third quarter of 2025, up nearly 6% from a year earlier, per the Federal Reserve Bank of New York. Average APRs hover around 21%, far above the proposed ceiling, prompting Bank of America to consider options despite CEO Brian Moynihan’s public reservations. “If you actually make this a policy, it can re-allocate credit,” Moynihan cautioned in a Bloomberg TV interview, highlighting fears that subprime borrowers could lose access entirely.

Trump’s Directive Ignites Industry Firestorm

Trump doubled down at the World Economic Forum in Davos, urging Congress to enact the cap legislatively after his initial social media salvo lacked enforcement details. Shares of major issuers plunged: Capital One and Synchrony Financial dropped 6% and 8%, while American Express, Visa, and Mastercard fell over 2%, as reported by BBC News. JPMorgan Chase CEO Jamie Dimon labeled it an “economic disaster,” echoing concerns from five banking trade groups that a cap would drive consumers to unregulated, costlier alternatives.

Citigroup Inc. is similarly weighing a 10% rate card, per people familiar with the matter cited in Bloomberg News. Fintech Bilt Rewards swiftly launched three cards at 10% APR for one year, targeting rent and mortgage payers, positioning itself ahead of traditional banks. Bank of America’s existing BankAmericard offers 0% introductory APR for 18 months, rising to 14.5%-24% thereafter, illustrating the gap between promo rates and ongoing costs.

Bank Strategies Amid Regulatory Fog

Executives remain puzzled over enforcement, with no executive order or law materializing post-January 20. TD Cowen analyst Jaret Seiberg noted, “We believe Treasury Secretary [Scott] Bessent understands how this could limit credit card lending and expose banks to risk,” anticipating pushback for a higher cap, as per CBS News. A Vanderbilt Policy Accelerator study counters industry doomsday scenarios, projecting $100 billion in annual consumer savings with minimal rewards disruption.

The proposal revives bipartisan efforts like Sens. Bernie Sanders and Josh Hawley’s stalled bill for a five-year 10% cap. House Speaker Mike Johnson flagged “negative secondary effects” for low-score borrowers, while National Economic Council director Kevin Hassett floated a “Trump card” for subprime users. Bank of America added 3.8 million card accounts in 2025, with credit cards comprising a key profit driver, per earnings data cited in Yahoo Finance.

Profit Pressures and Credit Rationing Risks

Analysts at Wells Fargo estimate a one-year cap could slash large bank pre-tax earnings 5%-18%, devastating pure-play issuers like Capital One. An Electronic Payments Coalition study warns of 175 million accounts—nearly 90%—closing, targeting scores below 740. “A 10% cap only works with ultra low defaults, which excludes most current cardholders,” observed Reddit’s r/Economics community, reflecting insider skepticism.

Bank of America CEO Moynihan stressed affordability commitments on earnings calls: “We’re all in for affordability,” but decried caps’ unintended consequences like stricter underwriting. Citigroup’s Jane Fraser warned of spending and growth impacts. Post-Fed rate cuts, average APRs dipped to 19.7% by December 2025 from 2024 peaks, per Bankrate via CBS News, yet still triple the proposed limit.

Political Maneuvering Shapes Banking Response

As Trump pivots to Congress, banks explore olive branches: no-rewards, low-limit cards at 10% for prime customers, akin to current offerings. Reuters sources indicate industry-administration talks for clarity, with lenders taking the directive seriously despite legal hurdles. Sen. Elizabeth Warren dismissed unilateral action as meaningless without legislation.

Credit card debt surged 60% in four years, per LendingTree, underscoring voter angst Trump targets ahead of midterms. NBC News notes unusual right-left unity, with Reps. Alexandria Ocasio-Cortez and Anna Paulina Luna backing a 10% cap bill. Bank of America and peers’ deliberations signal pragmatic navigation of Trump’s unpredictable policy pressure.

Long-Term Fallout for Consumers and Issuers

No major issuer complied by January 20, but targeted products could emerge, limited to elite borrowers. “10% of something is still better than 20-30% of nothing,” AFM Consulting’s Aaron McPherson told American Banker. KBW projects Citi hit hardest (10% 2026 earnings cut), followed by JPMorgan, Bank of America, and Wells Fargo.

Moelis & Co.’s Moshe Orenbuch envisions “less robust” features on 10% cards, preserving profitability. Consumer Federation of America’s Adam Rust affirmed, “A change like this cannot occur just by a tweet.” With $1.23 trillion in debt per Fed data, the standoff tests Wall Street’s leverage against populist demands, potentially reshaping lending dynamics.