Stocks face fresh danger. Bank of America sees it clearly. A widening gap between individual company price swings and overall market calm mirrors conditions right before the dot-com collapse two decades ago. The signal flashed again this month. And it comes as investors pull money from overheated artificial intelligence plays toward other sectors.

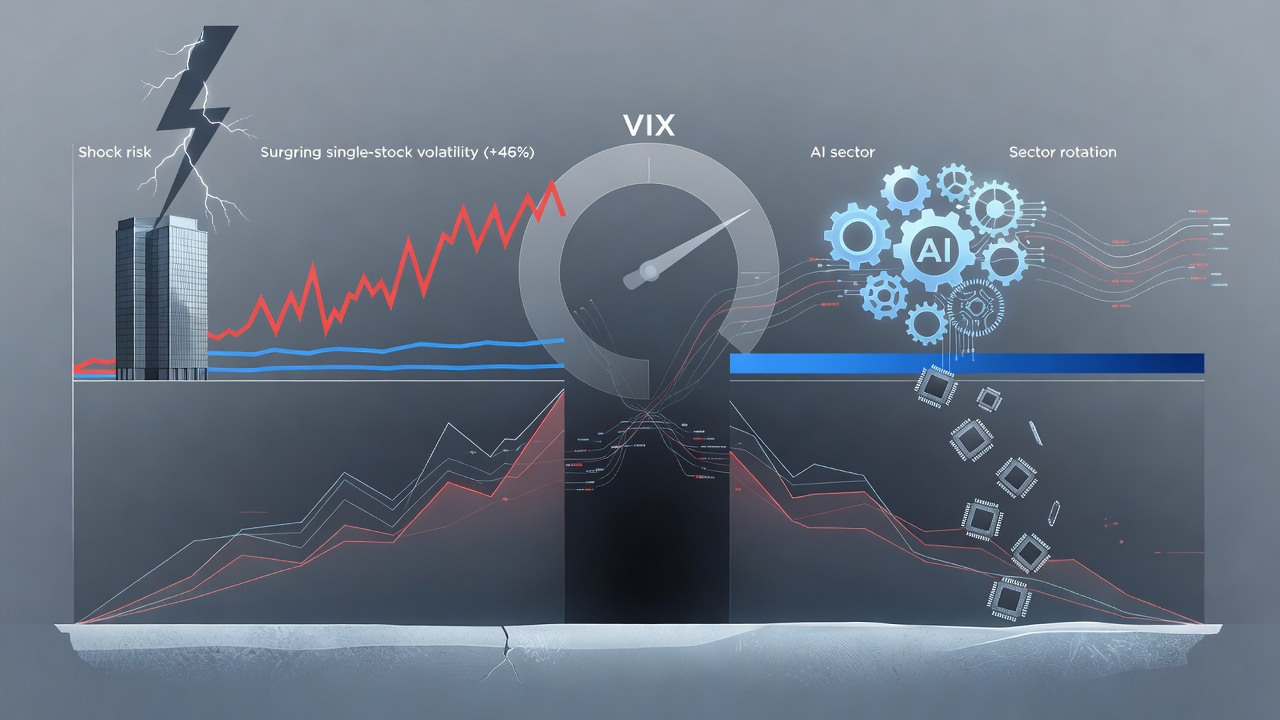

The S&P 500 Constituent Volatility Index, known as VIXEQ, sat near 50 in early July. That marked a 46 percent jump for the year. Meanwhile the broader VIX held around 16, up only 13 percent. This historic divergence has reached levels last seen in the final stages of the dot-com bubble. Bank of America’s global equity derivatives team put it bluntly. “Stock vs index vol near Dotcom extreme… shock risk is real,” they wrote in a note reviewed by Business Insider.

Index volatility stays muted even as single stocks whip around. The mismatch could grow larger. It might even top dot-com extremes if stock valuations keep climbing into rarefied air. That warning lands at a tricky moment. Markets now enter the historically weaker stretch from May through October.

Semiconductor shares drove much of the split. The iShares Semiconductor ETF climbed 83 percent this year yet dropped 12 percent from its late-June high. Investors rotated out of chip names to lock in gains and hunt better opportunities elsewhere. Correlations between semiconductors and other megacap technology companies or software firms have fallen to record lows. But the rotation itself signals caution. Heavy concentration in a handful of AI leaders propped up broader indexes for months.

Stifel analysts highlighted similar risks in their own recent research. They observed that periods when the gap between single-stock and index volatility narrows have often come right before sharp market declines. The pattern holds across multiple cycles. This time the stakes feel elevated because so much market value rests on expectations for artificial intelligence payoffs that remain years away.

Recent market action bears this out. On July 10, a Bloomberg report detailed how the S&P 500’s narrow leadership by the so-called Magnificent Seven has begun to fracture. Tech giants still dominate index returns, yet breadth has deteriorated. Bloomberg noted that equal-weighted indexes underperformed cap-weighted ones by the widest margin in years during the second quarter.

Conversations on X reflect the same tension. One trader posted on July 12 that current gains rest on continued heavy investment in a few AI names. “Once the heavy investment stops, it’s going to be worse than the dot com bubble bursting,” the user @CVREToken warned. Another account mapped out sector flows on July 5, showing outflows from AI and semiconductors into industrials, financials, energy and healthcare. The post from @AiGlitchPark described elevated volatility in the Nasdaq-100 tied directly to upcoming tech earnings.

These observations line up with data from the CBOE. Its June report first flagged the record spread between the VIXEQ and the VIX. Single-stock realized volatility now sits at extremes not witnessed since the months preceding the 2000 crash. Bank of America analysts argue the divergence could widen more if price action alone does not cool valuations.

History offers little comfort. During the dot-com peak, similar volatility patterns preceded a brutal unwind that erased trillions in market value. Technology stocks led the decline. This cycle, artificial intelligence hype replaced internet euphoria. Capital expenditure plans by big tech firms on data centers and chips have reached hundreds of billions of dollars. Yet actual revenue from transformative AI applications still lags those forecasts.

Portfolio managers have started to adjust. Some trimmed positions in Nvidia, Broadcom and other chip leaders while adding to financials and traditional industrials. The move echoes late-1999 behavior when investors fled pure internet plays for more established businesses. But the speed of the current rotation caught many by surprise. Liquidity in smaller names remains thin. That raises the odds of sharp price moves if selling accelerates.

Federal Reserve policy adds another layer. With inflation still sticky and labor markets cooling but not collapsing, officials have held rates steady. Markets price in only modest cuts later this year. That environment favors companies with strong cash flows over speculative growth stories. It also increases pressure on highly valued AI stocks that trade at multiples far above the broader market.

Analysts at JPMorgan flagged related risks in a separate June report covered by Business Insider. They pointed to surging capital spending by the Magnificent Seven as another parallel to the dot-com era. When that spending slows, the support for related suppliers could vanish quickly.

Seasonality compounds the concern. The next several months historically deliver weaker equity returns. Volatility tends to rise. If single-stock swings stay elevated while index measures remain suppressed, the eventual convergence could prove painful. Bank of America’s team sees that convergence as a real threat rather than a remote possibility.

Market participants disagree on timing. Optimists argue artificial intelligence represents a genuine productivity breakthrough that justifies current prices. Skeptics counter that adoption curves move slower than expected and returns on investment may disappoint. Both sides watch the same volatility metrics. The divergence itself has become the story.

So far this month, the S&P 500 has traded in a tight range. Technology shares show mixed performance. Some megacaps rebound while semiconductors stay under pressure. Dispersion across the index remains high. That condition rarely lasts without consequence.

Investors would do well to monitor the VIXEQ closely in coming weeks. Any sustained move above recent highs would reinforce the Bank of America warning. At the same time, improving breadth in non-tech sectors could ease some pressure. The balance between these forces will decide whether the shock materializes or remains just a risk on the horizon.

One thing seems clear. The market’s dependence on a narrow group of AI winners has created fragility. When that concentration breaks, the adjustment may not be gentle. History rhymes. This time the verse centers on machine learning instead of web browsers. The tune sounds familiar all the same.