AT&T just overhauled its consumer wireless lineup, and the changes matter more than a typical carrier rebrand. The new structure—Value Plus, Extra, and Premium 2—replaces the existing Value Plus, Unlimited, and Premium tiers. It’s a recalibration of what each price point gets you, and for some customers, it’s a meaningful downgrade disguised as simplification.

The details first surfaced through internal documents reported by Android Authority, which obtained information about the restructured plans ahead of a broader public rollout. Here’s what’s changing and why wireless industry professionals should pay attention.

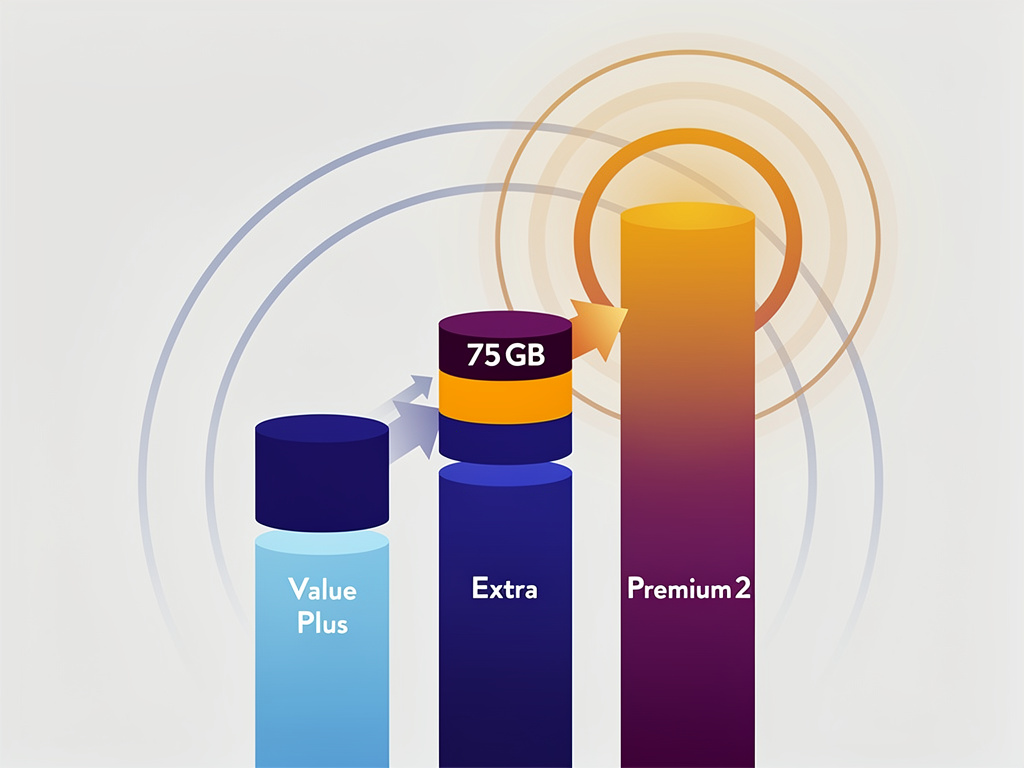

What the New Tiers Actually Offer

The entry-level Value Plus plan stays largely the same in name but sees adjustments. It remains AT&T’s budget option, designed for customers who want unlimited talk, text, and data without the premium extras. No hotspot. No streaming perks. The baseline.

The middle tier is where things get interesting. AT&T is renaming its current “Unlimited” plan to “Extra,” and it comes with notable feature shifts. According to Android Authority’s reporting, Extra includes 75 GB of prioritized data before potential deprioritization, 30 GB of hotspot data, and access to some streaming benefits. That middle tier is clearly positioned to absorb the bulk of AT&T’s subscriber base—customers who want more than bare-bones service but don’t need everything.

Then there’s Premium 2, the top-end plan replacing the current Premium tier. It reportedly offers truly unlimited prioritized data, 60 GB of hotspot, and the full spread of AT&T’s entertainment partnerships. Think bundled subscriptions and international roaming perks.

But the real story isn’t the top or bottom. It’s the middle.

The Strategic Squeeze on Mid-Tier Customers

AT&T’s move mirrors a broader pattern across all three major U.S. carriers: compress the middle tier’s value just enough to push subscribers toward the premium plan. T-Mobile did this with its Go5G restructuring. Verizon did it with myPlan. Now AT&T is playing the same hand.

By capping prioritized data at 75 GB on Extra—down from what some existing Unlimited plan holders currently enjoy—AT&T creates a friction point. Most users won’t hit 75 GB in a billing cycle. But power users, families sharing data-heavy habits, and anyone tethering regularly will feel the squeeze. And that’s precisely the point. The upgrade path to Premium 2 becomes the obvious answer.

It’s a classic carrier playbook move. Not predatory, exactly. But deliberate.

For existing customers, the transition raises questions about grandfathered plans. AT&T has historically allowed legacy plan holders to keep their terms, but new device financing deals and promotional pricing often require switching to current plans. That soft pressure tends to accelerate migration over time.

Industry analysts have noted that carrier ARPU (average revenue per user) growth has become the key metric Wall Street watches, especially as subscriber growth plateaus in a saturated U.S. market. Restructuring plan tiers is one of the most effective tools carriers have to nudge ARPU upward without raising sticker prices outright. The math is straightforward: if even 10-15% of mid-tier subscribers upgrade, the revenue impact is significant across AT&T’s roughly 70 million postpaid phone subscribers.

So what should professionals in the wireless space actually take away from this?

First, plan naming conventions are becoming more transparent across the industry. “Value,” “Extra,” and “Premium” are self-explanatory in a way that “Unlimited” never was—because every carrier’s “unlimited” plan came with limits. The shift toward honest labeling is a competitive response to years of consumer confusion and FTC scrutiny over misleading unlimited claims.

Second, hotspot data allocation is emerging as the key differentiator between tiers. Not prioritized data caps. Not streaming bundles. Hotspot. As remote work persists and tablet usage grows, the ability to tether devices carries real utility value. AT&T clearly understands this, which is why the gap between 30 GB (Extra) and 60 GB (Premium 2) is so pronounced.

Third, the entertainment bundling war continues to escalate. AT&T’s premium tier reportedly includes enhanced streaming partnerships, though specific services weren’t fully detailed in the leaked documents. This follows Verizon’s aggressive Netflix and Max bundling and T-Mobile’s partnerships with Apple TV+ and other platforms.

What Comes Next

AT&T hasn’t officially announced the public launch date for these restructured plans, though Android Authority’s reporting suggests the rollout is imminent. Expect marketing to emphasize simplicity and choice—the same framing every carrier uses when reshuffling tiers.

For enterprise and MVNO partners, the plan changes could ripple into wholesale agreements and reseller structures. Any shift in AT&T’s retail pricing architecture tends to cascade.

The bottom line: AT&T isn’t reinventing wireless pricing. It’s optimizing it. The new tiers are designed to clarify options for consumers while quietly engineering higher revenue per line. A familiar strategy, executed with precision. Whether customers see through it depends on how carefully they read the fine print—something carriers have always counted on them not doing.