Apple stands on the verge of upending the foldable smartphone market. One report forecasts its first folding handset will claim nearly a third of all flexible display orders next year. The numbers come from fresh analysis that shows the device driving a sharp recovery in panel shipments after years of uneven growth.

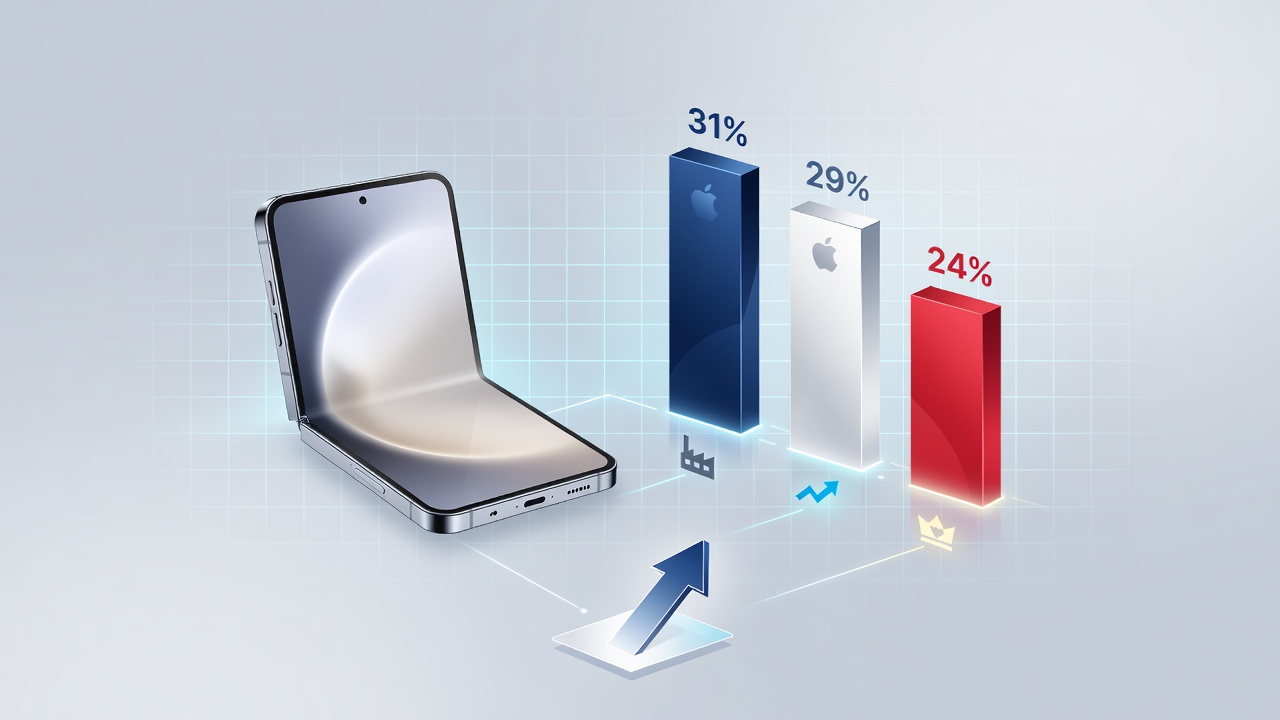

According to Counterpoint Research, global foldable smartphone screen shipments should hit roughly 27.5 million units in 2026. That marks a 24 percent jump from the prior year. Revenues could climb even faster, rising around 48 percent. The surge traces directly to Apple’s entry. Its iPhone Fold alone is expected to account for 29 percent of those display orders.

Samsung holds a narrow lead at 31 percent. Huawei follows with 24 percent. The split highlights how quickly the balance of power could tilt once Cupertino joins the fray. And the shift extends beyond volume. Apple’s presence pushes the entire category toward higher average selling prices. Book-style foldables now dominate over cheaper clamshells. Growth in this segment, one analyst observed, “is not entirely dependent on Apple.”

But Apple supplies a massive catalyst. Recent supply chain updates reinforce the momentum. 9to5Mac reported yesterday that Apple has raised its production target for the foldable device to around 10 million units. The figure sits higher than an earlier estimate of 7 million to 8 million. Suppliers received instructions to prepare components accordingly, even as the company eyes total iPhone output above 220 million units for the year.

Technical hurdles appear manageable. Hinge issues that once threatened delays have largely been resolved. Mass production is slated for later this year, with a launch window that could align with the iPhone 18 series in September 2026. Some voices still flag possible slips into early 2027. Yet the latest signals point to confidence. Samsung Display won exclusive rights to produce the OLED panels under a three-year deal. Initial orders reportedly reached about 3 million units before climbing. The partnership makes sense. Samsung Display’s share of the foldable panel market already rose to 22 percent in the first quarter of 2026, up from 15 percent a year earlier.

Contrast that with BOE. The Chinese supplier commanded 45 percent of shipments in the same period. Its position slipped from 52 percent the year before. Apple reportedly passed on BOE panels for both the iPhone 18 Pro and the foldable model. Quality and yield concerns drove the decision. The choice funnels more business to Samsung and underscores the premium focus Apple brings to the category.

Design details have trickled out steadily. The device is expected to unfold to a 7.8-inch inner display with a 5.5-inch cover screen. Thickness could land near 9.5 millimeters when open and roughly 4.5 millimeters when closed. A nearly invisible crease ranks high on the priority list. Durability and screen quality should surpass current rivals, according to people familiar with the plans. Pricing starts above $2,000. That premium tag matches the book’s positioning as a halo product rather than a mass-market play.

Market researchers see broader effects. IDC projected last year that the worldwide foldable smartphone market would expand 30 percent in 2026, boosted by Apple’s arrival. The forecast assumed shipments nearly doubling in some segments. Apple’s volume target of 10 million units would represent a meaningful slice of that growth, especially if early demand exceeds conservative estimates.

Yet risks remain. Memory shortages plague the industry. Apple has asked suppliers to stockpile parts from the iPhone 17 line for the next generation. Chinese vendors such as Xiaomi, Oppo and Vivo slashed their own production plans below 100 million units each because of component constraints. Apple, with its scale and negotiating strength, secured reservations for 80 million smartphones tied to its new models in the second half of 2026. The contrast shows how the company can weather supply crunches that hobble others.

Tri-fold designs face steeper barriers. Devices like Huawei’s Mate XT and Samsung’s Galaxy Z TriFold suffer from yield problems and added complexity. They won’t move to mass market soon. The industry instead doubles down on proven book-style formats. Apple’s version arrives late to this race. Samsung has sold foldables since 2019. Huawei built strong share in China. Still, neither matched Apple’s brand power or its ability to define a new standard.

Software groundwork already appears in iOS 27. Features point to support for larger canvases, resizable windows, landscape apps and improved multitasking. These additions suggest the foldable iPhone will feel native rather than like an afterthought. No Face ID under the display has surfaced in some rumors, though details stay fluid. The absence of certain components could help control costs or improve reliability in the flexible form.

Analysts debate the exact impact. One forum commenter noted that even 29 percent of the foldable segment might equal only half a percent of the total smartphone market. Foldables made up about 1.6 percent of shipments in 2025. The comparison puts Apple’s move in perspective. It won’t transform overnight. But it could accelerate adoption. Once consumers experience a polished foldable with the iPhone’s software and services, demand may broaden faster than expected.

Recent reporting adds texture. Forbes highlighted in June that while Samsung produces the screens, hinge refinements remain a focus. Production caution shows in the initial 3 million unit run, mirroring Samsung’s own Galaxy Z Fold volumes. CNET noted eight days ago that a September 2026 debut looks increasingly likely, though some forecasts still allow for December or early 2027. Mark Gurman of Bloomberg has repeatedly said the project stays on track.

Ming-Chi Kuo, the analyst known for accurate supply chain predictions, signaled production could begin in 2026 for a later-year release. His earlier calls pointed to a crease-free design by the end of that year. The consensus has tightened around fall 2026. Apple’s history of premium execution suggests it will wait until the hardware meets its standards. No rush to market simply to claim first-mover status.

The bigger picture involves more than one phone. Apple plans at least five new iPhone models from late 2026 into early 2027. These include the foldable, a new slim iPhone Air, updated Pro variants and the base iPhone 18. The expanded lineup reflects ambition at a time when overall smartphone growth remains modest. Success with the foldable could open doors to other flexible devices, perhaps even a folding iPad down the line. For now the focus stays on proving the concept in the handset arena.

Competitors watch closely. Samsung must defend its lead while possibly adjusting prices or features. Huawei will lean on its domestic strength. Chinese panel makers like BOE face pressure to improve yields if they want future Apple business. The entire supply chain feels the ripple. Orders for higher-end materials and components will rise. That lifts revenues for key suppliers even as it squeezes smaller players.

Price sensitivity could limit uptake. At $2,000 or more, the iPhone Fold targets affluent buyers and early adopters. Volume depends on whether those buyers see enough daily value in the folding design. Productivity gains from the larger screen, better multitasking and iOS integration may convince them. Battery life, crease visibility and long-term durability will decide repeat purchases.

Data from the first quarter already shows the market evolving. Book-style devices gained share as consumers moved upmarket. Clamshell models, once popular for their compact size, lost ground. Apple’s emphasis on a premium book-style product aligns with this trend. It avoids the lower end entirely. The strategy mirrors how the company entered the smartwatch and wireless earbud categories: start at the top, set the standard, then expand.

Supply chain reports from Nikkei Asia yesterday confirmed the raised 10 million unit target and noted that hinge challenges have been mostly overcome. The publication also detailed Apple’s efforts to maintain iPhone shipment forecasts despite component shortages. Its bargaining power allows it to lock in parts that competitors cannot secure. This advantage could prove decisive if memory prices stay elevated.

Industry insiders expect the iPhone Fold to outperform initial Samsung foldable sales in its debut year. The brand loyalty, ecosystem lock-in and marketing muscle give Apple an edge no rival matches. Whether that translates to 29 percent of display orders depends on execution. The numbers from Counterpoint assume strong supplier performance and healthy demand. Early indications support that view.

So the stage is set. A single device could lift an entire category. Panel makers gear up. Software teams refine the experience. Consumers wait to see if the wait was worth it. Apple’s foldable bet carries risk, but the potential reward is a new flagship category that extends its dominance in premium smartphones for years ahead.