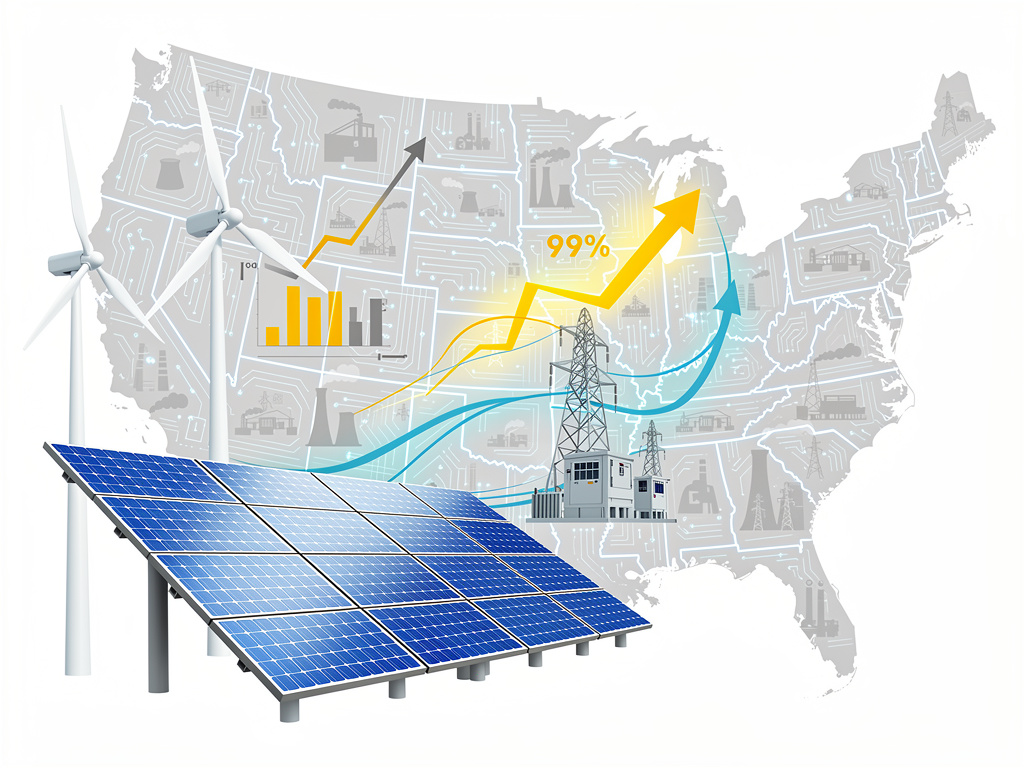

The United States energy sector has reached an inflection point that few analysts predicted even a decade ago. According to data from the Federal Energy Regulatory Commission, renewable energy sources will account for 99% of all new electricity generating capacity added to the American grid in 2026, marking what industry experts describe as a fundamental restructuring of the nation’s power infrastructure.

This near-total dominance of clean energy in new capacity additions represents a dramatic acceleration from previous years and signals that the transition away from fossil fuel generation has moved beyond policy aspirations into market reality. Slashdot reported that solar power alone will contribute 76.9 gigawatts of new capacity, while wind energy will add another 15.2 gigawatts, with battery storage systems providing an additional 33.8 gigawatts to support grid stability.

The numbers tell a story of economic forces overwhelming political headwinds. Even as debates over climate policy continue in Washington, utility companies and independent power producers have voted with their capital expenditures, choosing renewable installations over traditional generation at ratios that would have seemed fantastical during the previous decade. Natural gas, which once represented the bridge fuel to a cleaner energy future, will account for merely 1% of new capacity additions this year, with a paltry 1.1 gigawatts of new plants coming online.

The Economics Driving the Green Surge

The shift toward renewable dominance stems primarily from fundamental economics rather than regulatory mandates. Solar panel costs have plummeted approximately 90% since 2010, while wind turbine efficiency has improved dramatically through technological advances in blade design and tower height. Battery storage costs have followed a similar trajectory, dropping roughly 80% over the past decade, making it economically viable to pair intermittent renewable sources with storage systems that can dispatch power when the sun isn’t shining or wind isn’t blowing.

Corporate power purchase agreements have emerged as a critical financing mechanism driving this transformation. Technology giants including Amazon, Google, and Microsoft have committed to purchasing massive quantities of renewable energy to power their data centers, providing developers with the long-term revenue certainty needed to secure project financing. These agreements have effectively created a parallel market for clean energy that operates independently of traditional utility procurement processes.

The investment community has responded accordingly. Major financial institutions have redirected capital flows away from fossil fuel projects, citing both climate risks and superior returns available in the renewable sector. This reallocation of capital has created a self-reinforcing cycle where renewable projects can access cheaper financing than their fossil fuel competitors, further widening the economic advantage that clean energy enjoys in head-to-head competition.

Grid Integration Challenges and Solutions

The rapid expansion of variable renewable energy sources has forced grid operators to fundamentally rethink how they manage electricity supply and demand. Traditional power systems were designed around large, centralized fossil fuel and nuclear plants that could adjust output to match consumption patterns. The new grid must accommodate thousands of distributed solar installations and wind farms whose output fluctuates based on weather conditions beyond human control.

Battery storage systems have emerged as the critical technology enabling this transition. The 33.8 gigawatts of storage capacity being added in 2026 will provide grid operators with unprecedented flexibility to absorb excess renewable generation during periods of high production and release that stored energy during peak demand periods. California has led the nation in demonstrating how large-scale battery installations can replace the role traditionally played by natural gas peaker plants, which utilities fired up during periods of high demand.

Advanced forecasting technologies have also proven essential to managing grids with high renewable penetration. Machine learning algorithms can now predict solar and wind output with remarkable accuracy days in advance, allowing grid operators to plan for variability and coordinate resources across wider geographic areas. Regional transmission organizations have expanded their footprints and enhanced their real-time coordination capabilities, enabling them to balance supply and demand across larger territories where weather patterns and demand fluctuations tend to average out.

Regional Variations in the Transition

While the national statistics show overwhelming renewable dominance, significant regional variations persist based on resource availability, existing infrastructure, and state policies. Texas leads the nation in both wind and solar installations, leveraging its abundant land, strong wind resources, and competitive wholesale electricity market structure. The state’s grid operator, ERCOT, has successfully integrated massive quantities of renewable energy despite operating independently from the broader national grid system.

The Southeast has lagged behind other regions in renewable deployment, hampered by regulated utility structures that provide less incentive for rapid transformation and lower average electricity prices that make new generation investments harder to justify economically. However, even traditionally conservative utilities in states like Georgia and Florida have announced ambitious solar expansion plans, recognizing that customer demand and economic fundamentals now favor clean energy even in markets where policy support remains limited.

The Midwest has emerged as a wind power powerhouse, with states like Iowa now generating more than half their electricity from wind turbines. The region’s strong and consistent wind resources, combined with extensive agricultural land available for turbine installation, have created ideal conditions for wind development. Farmers have embraced wind energy as a supplemental income source that allows them to continue agricultural operations while leasing small portions of their land for turbine foundations.

Manufacturing and Supply Chain Implications

The explosive growth in renewable installations has created both opportunities and challenges for domestic manufacturing. While the United States has succeeded in building a robust solar installation industry, the majority of solar panels continue to be manufactured overseas, primarily in Asia. This supply chain concentration has raised concerns about economic security and the ability to capture the full economic benefits of the clean energy transition.

Wind turbine manufacturing presents a more balanced picture, with several major facilities operating in the United States producing towers, blades, and nacelles for the domestic market. The sheer physical size of wind turbine components creates natural advantages for domestic production, as transportation costs for massive blades and tower sections favor factories located relatively close to installation sites. Battery manufacturing has also seen significant domestic investment, with multiple gigafactories under construction to serve both the electric vehicle and grid storage markets.

The Biden administration’s Inflation Reduction Act included substantial tax incentives designed to encourage domestic manufacturing of clean energy components. These provisions have begun to show results, with companies announcing plans for new solar panel factories and battery component facilities. However, building competitive domestic supply chains requires time and sustained policy support to overcome the cost advantages that established Asian manufacturers enjoy through economies of scale and integrated supply chains.

Employment and Workforce Development

The renewable energy boom has created hundreds of thousands of jobs in construction, manufacturing, and ongoing operations and maintenance. Solar installers and wind turbine technicians have become among the fastest-growing occupations in the American economy, with demand far outstripping the supply of trained workers in many markets. Community colleges and technical schools have rushed to develop training programs, but workforce development has struggled to keep pace with industry growth.

The transition has created economic challenges for communities historically dependent on fossil fuel industries. Coal mining regions have seen continued employment declines, and natural gas production areas face an uncertain long-term outlook as new power plant construction has essentially ceased. While renewable energy creates jobs, they often emerge in different locations than the fossil fuel jobs being displaced, creating geographic winners and losers that policy makers have struggled to address effectively.

Labor unions have played an increasingly important role in shaping the clean energy transition, pushing for prevailing wage requirements and apprenticeship programs that ensure renewable energy jobs provide middle-class incomes and career pathways. The Inflation Reduction Act included provisions that tie tax credit values to wage standards and apprenticeship utilization, effectively requiring developers to meet union-backed labor standards to receive full financial benefits.

Looking Beyond 2026

Industry analysts project that renewable energy’s dominance of new capacity additions will continue and likely intensify in coming years. The combination of improving technology, falling costs, and growing corporate and consumer demand for clean energy has created momentum that appears resistant to potential policy changes. Even scenarios involving reduced federal support for renewables suggest that market forces alone would sustain high levels of clean energy deployment.

The focus is already shifting from whether renewable energy will dominate new additions to how quickly existing fossil fuel plants will retire and what mix of technologies will provide the firm, dispatchable power needed to maintain grid reliability during extended periods of low renewable output. Nuclear energy advocates argue that advanced reactor designs could play this role, while others point to long-duration energy storage, enhanced geothermal systems, or green hydrogen as the technologies that will complete the transition to a fully decarbonized grid.

What remains clear is that 2026 represents not an aberration but rather a glimpse of the energy system’s future trajectory. The United States is in the midst of the most significant transformation of its electricity infrastructure since the original grid buildout in the early twentieth century, and renewable energy has emerged as the dominant force shaping that transformation.