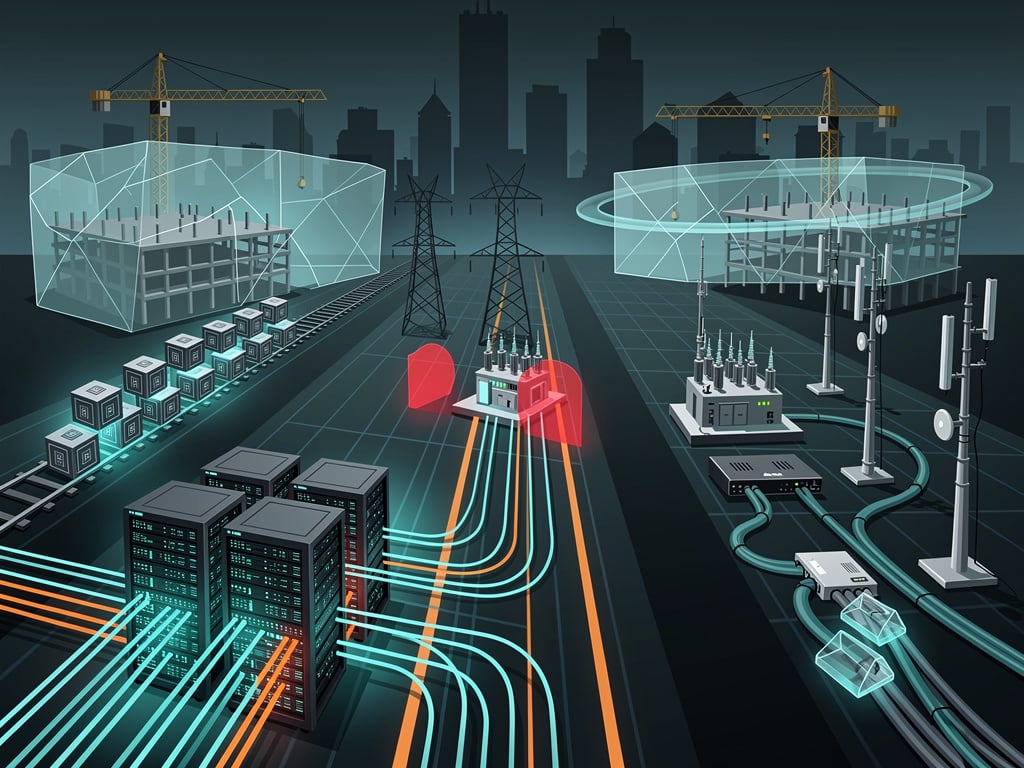

The hyperscalers have committed hundreds of billions. Facilities rise at a startling clip. Yet the promise of artificial intelligence keeps slamming into physical limits that no amount of capital seems able to bulldoze quickly enough. Power shortages. Interconnection queues stretching years. Networks that cannot shuttle data at the speeds demanded by sprawling training clusters and latency-sensitive inference workloads.

Two data centers a week will not close the gap. The infrastructure conversation has shifted. Hardware shortages that plagued the sector in 2022 have given way to something more stubborn. The grid itself now dictates timelines.

By the end of this year the top five hyperscalers will have poured roughly $600 billion into AI infrastructure. TechRadar reports that more than 3,000 data centers operate across the United States with another 1,500 in development. Some estimates suggest two new facilities come online weekly. The pace looks impressive on paper. Reality tells a different story.

Mahesh Krishnaswamy, founder and CEO of Taara, puts it plainly. Building this infrastructure without adequate connectivity resembles constructing cities without roads. Training clusters must exchange enormous volumes of data. Inference workloads spread across edge sites, regional hubs and cloud platforms. None of it functions smoothly when the networks lag. “The networks built to move data simply aren’t keeping pace with the compute being built to generate it,” he writes.

Compute alone solves nothing. Those expensive GPUs depreciate fast. In some cases they lose up to 90 percent of value inside 48 months. Organizations feel intense pressure to extract maximum output immediately. That requires constant, high-speed data flows. When connections falter, racks sit idle. Expensive paperweights.

But connectivity forms only one side of the obstacle. Power has become the dominant choke point. A May analysis from TechInvestments.io delivered sobering numbers. Sightline Climate tracked 12 gigawatts of U.S. data center capacity announced for 2026 across 140 projects. Only 5 gigawatts sit under construction. Eleven gigawatts remain announced with zero physical progress despite typical 12-to-18-month build cycles. Twenty-five percent of projects disclose no power strategy whatsoever.

A viral assessment captured the mood. “A 5-year backlog on grid transformers just killed half of America’s 2026 AI data centers.” Lead times tell the tale. Before 2020 a high-voltage transformer took 24 to 30 months. Today the wait stretches to five years. Electrical equipment represents less than 10 percent of total project cost yet accounts for 100 percent of the bottleneck. High-voltage transformers, switchgear and grid-tie batteries dominate the constraint list.

Executives have noticed. GE Vernova described current lead times as directionally around three years with many 2030 slots already sold and only 10 gigawatts remaining cumulatively for 2029 and 2030. HSBC analysts called high-voltage substations the key bottleneck with 3-to-5-year waits, a driver behind the rise of build-your-own-power models. One Barclays note highlighted Oracle’s pivot with Bloom Energy to a fully islanded microgrid for its Jupiter project.

The numbers grow more daunting when viewed through a wider lens. Goldman Sachs Research forecasts data center power demand will climb 50 percent by 2027 and as much as 165 percent by decade’s end. A Goldman Sachs report underscores the transmission bottleneck. Utilities cannot expand capacity fast enough because of permitting delays, supply chain issues and the sheer time required to build new lines.

Deloitte’s 2025 AI Infrastructure Survey, released in June 2025, painted a stark picture after polling 120 U.S. executives split between data center operators and power companies. Seventy-two percent rated power and grid capacity as very or extremely challenging. Seventy-nine percent expect AI to drive higher power demand through 2035. Some interconnection requests face seven-year waits. Ninety-five percent of projects in generation queues consist of renewables and storage. Baseload generation contracts while peak demand from always-on AI clusters spikes.

One executive summary from the survey noted that a single large AI data center can consume as much electricity as a city of hundreds of thousands of homes. Campuses reaching 5 gigawatts have entered early planning. Demand could hit 123 gigawatts by 2035, more than 30 times the 4 gigawatts recorded in 2024.

But the grid cannot absorb that load on current schedules. Lawrence Berkeley National Laboratory data shows interconnection queues hold more than 2,300 gigawatts of generation and storage proposals, exceeding total U.S. installed capacity. Only 13 percent of requests filed between 2000 and 2019 had reached commercial operation by late 2024. Seventy-seven percent were withdrawn.

Recent coverage reinforces the trend. A Data Center Knowledge article from April 2026 declared power the single biggest gating item for development, ahead of capital or land. The Department of Energy estimates another 100 gigawatts of peak capacity needed by 2030 with data centers driving half that figure. Morgan Stanley Research in February 2026 projected U.S. data center demand could reach 74 gigawatts by 2028 against a 49-gigawatt shortfall in available power access.

Construction statistics reflect the pressure. CBRE data showed U.S. data center capacity under construction dipped to 5.99 gigawatts at the end of 2025 from 6.35 gigawatts a year earlier. Nearly half of projects slated for 2026 face delays or cancellation according to analysts cited in multiple reports. The bottleneck has migrated decisively from chips to substations.

And still the investment rolls forward. Hyperscalers explore nuclear restarts, small modular reactors, fuel cells and direct contracts with generators. Some pursue behind-the-meter generation to bypass queues. Others turn to alternatives for connectivity.

Krishnaswamy argues traditional fiber cannot scale fast enough. The U.S. has deployed 159 million miles of fiber yet needs another 213 million to meet AI requirements. Deployment takes years. AI demand shifts in months. His company promotes wireless optical communication. Narrow beams of light create point-to-point links that deploy in hours rather than years. The technology sidesteps digging, permitting and the geographic constraints that slow cable expansion.

Whether such solutions arrive at commercial scale remains uncertain. What looks clear is the mismatch in timelines. Data centers can be erected in 18 to 24 months. Securing firm power delivery often takes five to seven years or longer. Transformers cannot be conjured faster. Transmission lines face regulatory reviews that stretch a decade.

So the industry adapts. Some projects pivot to regions with surplus capacity. Others accept higher costs for on-site generation. A few quietly cancel or defer ambitions. Executives quoted across reports emphasize that time to power now separates leaders from followers.

The AI buildout continues. Billions flow into chips, racks and facilities. Yet the supporting systems, the grid that feeds them and the networks that link them, refuse to accelerate on command. Those systems determine which investments deliver returns and which become stranded assets.

Observers once fixated on GPU availability. Attention has pivoted. Power availability, interconnection reality and data movement capacity now set the ceiling. Building two data centers a week changes the skyline. It does not automatically unlock the performance hyperscalers sold to investors and customers.

The coming years will test how creatively the sector can bridge these gaps. Some bets will pay off. Others will illuminate the difference between announced ambition and operational reality. The infrastructure race has entered its harder half. Compute was the easy part.