Power shortages loom. Data center operators scramble for megawatts. And the artificial intelligence boom shows no signs of slowing.

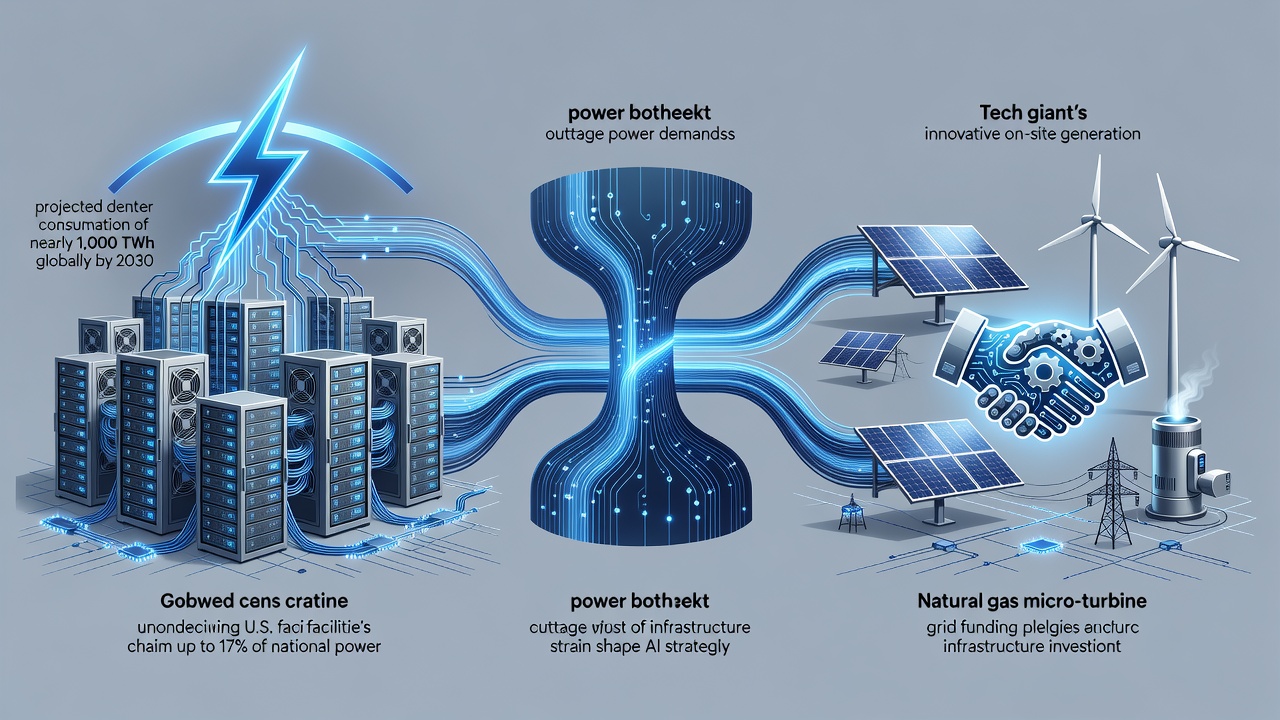

Global electricity use by data centers stood at roughly 415 terawatt-hours in 2024. That figure represented about 1.5% of worldwide consumption. Yet projections point to a near-doubling by 2030. The International Energy Agency forecasts 945 TWh under its base case. Accelerated AI adoption could push numbers higher still.

Numbers like these grab attention. They force utilities, governments and tech giants to confront hard limits on generation and transmission. Short sentences underscore the urgency. Longer ones reveal the complexity that follows.

Accelerated servers, those packed with GPUs for training and inference, drive much of the surge. Their electricity demand grows 30% annually in the IEA’s outlook. Conventional servers expand far more slowly at 9%. The result? Almost half the net increase in data center consumption comes from AI-specific hardware.

In the United States the pressure feels most acute. The country accounts for 45% of global data center electricity today. Domestic demand there could rise 130% by 2030. Lawrence Berkeley National Laboratory projects U.S. data centers consuming between 325 and 580 TWh by 2028. That range spans 6.7% to 12% of total national electricity.

The Numbers Don’t Lie

Gartner expects worldwide data center electricity consumption to hit 565 TWh in 2026. That’s a 26% jump from 447 TWh the prior year. Power demand measured in gigawatts climbs even faster, reaching 132 GW. These figures come from a Gartner report released in June 2026.

Goldman Sachs sees U.S. data center power demand more than doubling from 31 GW in 2025 to 66 GW in 2027. The bank’s commodities team laid out the forecast in May. Such growth outpaces nearly every other sector. Electric vehicles and electrification matter. They don’t match the speed of AI infrastructure buildout.

But. Efficiency gains once masked rising server counts. No longer. Density has exploded. A single rack can now draw 50 to 100 kilowatts. Some facilities approach 1 GW total load. Grids strain under the weight. Local operators report peak-hour risks and cost spikes reaching 1,000% in certain markets, according to recent discussions on X.

Tech companies respond with bold moves. OpenAI pledged to cover higher electricity prices and fund grid upgrades for its Stargate data centers. The $500 billion project, backed by Oracle and SoftBank, aims to avoid burdening local ratepayers. Reuters first reported details of the “Stargate Community” plan in January 2026. Microsoft offered similar commitments. President Trump praised both efforts.

Some operators bypass the grid entirely. Natural-gas turbines rise beside new facilities in West Texas as part of Stargate. xAI deploys them at its Colossus sites in Memphis. Fuel cells power more than a dozen other campuses. The Wall Street Journal detailed this emerging energy Wild West last October.

Sam Altman invests personally too. The OpenAI chief backed Exowatt, a startup developing solar-plus-storage solutions tailored for data centers. That 2024 deal, covered by the Journal, signaled early recognition of the power bottleneck.

Recent analysis sharpens the picture. A June 2026 Reuters story highlighted U.S. power consumption setting records in 2025 and climbing further in 2026 and 2027. AI-driven data centers and electrification share blame. The Energy Information Administration authored the outlook.

EPRI raised its own estimates in February. Data centers could claim 9% to 17% of U.S. electricity by 2030. That’s more than double earlier projections. Virginia stands out. Its data center share might reach 39% to 57% in the state. The Electric Power Research Institute release underscored how the past 18 months accelerated timelines.

Training one frontier model could soon require 5 GW. Anthropic offered that assessment. The company also projected the U.S. AI sector needing 50 GW of new capacity by 2028. Context helps. That equals twice New York City’s peak demand.

Inference adds another layer. Queries seem small. Sam Altman once pegged an average ChatGPT interaction at 0.34 watt-hours. Scale changes everything. Millions of users generate meaningful load. A Wall Street Journal investigation from 2025 traced the full journey from laptop prompt to GPU cluster. The numbers surprised even insiders.

Carbon implications draw equal concern. Training a single large model can emit hundreds of tons of CO2. Inference runs continuously. Hyperscalers chase renewables yet procurement lags demand. Amazon and Google face criticism for slipping net-zero targets. Recent X posts from industry observers highlight the growing gap between pledges and reality.

Regulatory responses vary. Japan eyes replacing aging nuclear reactors to meet AI needs. The country’s METI proposed up to 14 new units by the 2050s. European nations weigh similar options. In the U.S. permitting bottlenecks slow transmission projects. Data center developers now treat power, land, water and approvals as a single intertwined challenge.

Texas emerges as a clear winner. Its market share of U.S. data center capacity could hit 30% by 2028. ERCOT revised forecasts sharply upward. Other regions hesitate. Grid operators force cloud providers to fund upgrades or risk blackouts during peaks.

So the industry adapts. Some build their own generation. Others strike direct deals with nuclear operators for always-on power. Still more explore advanced cooling and chip efficiency to blunt demand growth. None expect the trajectory to flatten soon.

Financial markets reflect the stakes. Blackstone’s majority stake in Jersey Mike’s, acquired in 2024 at an $8 billion valuation, has little direct tie to AI. Yet the sandwich chain’s confidential IPO filing this spring, as reported by the Financial Times, illustrates how private equity eyes exits amid broader economic shifts. Capital flows toward energy infrastructure with equal fervor.

Projections differ in the details. IEA offers 945 TWh globally by 2030. Deloitte lands near 1,065 TWh. Goldman Sachs forecasts 160% growth in power demand. The spread reveals uncertainty around model sizes, utilization rates and efficiency breakthroughs. All scenarios, however, point upward. Sharply.

Utilities scramble to add capacity. Some regions face multi-year delays. Hyperscalers accelerate colocation and self-build strategies. The result is a fragmented market where location determines viability more than ever. Sites with existing transmission, water access and friendly regulators command premiums.

AI’s energy hunger won’t vanish. It will only grow as models enlarge and adoption spreads. Companies that solve the power equation gain lasting advantage. Those that don’t risk stalled roadmaps and disappointed investors. The coming years will test who prepared best for this new reality.