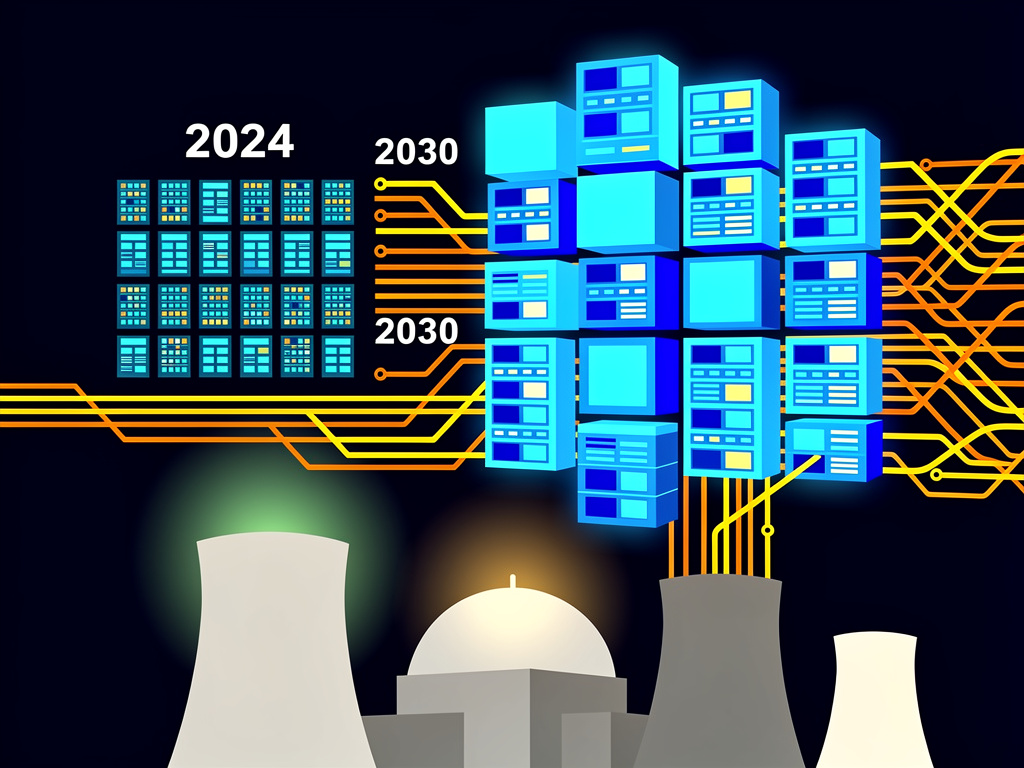

Data center electricity use hit roughly 415 terawatt-hours in 2024. That figure represented about 1.5 percent of global electricity consumption. But growth rates tell a sharper story. Demand from these facilities has climbed at 12 percent annually over recent years. The pace outruns overall electricity growth by a factor of four. Projections from the International Energy Agency show consumption doubling to around 945 TWh by 2030. AI-optimized servers drive much of the surge. Their electricity needs could quadruple in that span.

Tech executives once spoke of efficiency gains. Reality has delivered the opposite. Training ever-larger models and serving millions of queries demands constant computation. A single ChatGPT query uses several times the energy of a traditional web search. Scale that across billions of interactions. The aggregate effect strains grids already facing electrification pressures from vehicles and industry. But this pressure has also sparked fresh thinking on power sources.

Big Tech companies have turned to an old technology with renewed urgency. Nuclear power offers steady baseload output without carbon emissions. It matches the always-on requirements of data centers better than intermittent renewables alone. Microsoft struck a deal with Constellation Energy to restart a unit at the Three Mile Island plant in Pennsylvania. The agreement aims to supply carbon-free electricity for its operations starting later this decade. Google committed capital to multiple advanced nuclear projects through Elementl Power. Each site targets at least 600 megawatts. Amazon bought a data center campus next to a nuclear station. These moves mark a shift from past hesitation.

The Goldman Sachs research team examined the numbers closely. It estimates 85 to 90 gigawatts of new nuclear capacity will be required to cover all expected data center demand growth by 2030 relative to 2023 levels. That equates to dozens of large reactors. Or hundreds of smaller modular designs. Natural gas and renewables will fill gaps in the near term. Construction timelines for nuclear plants stretch long. Yet the financial case has improved. Tech firms can sign long-term purchase agreements that de-risk projects for utilities.

Small modular reactors have drawn particular interest. These factory-built units promise faster deployment and flexible sizing. The pipeline of conditional agreements between data center operators and SMR developers expanded from 25 gigawatts at the end of 2024 to 45 gigawatts today. That acceleration signals confidence. Kairos Power agreed to deliver power from seven such reactors to Google data centers. The first unit is slated for Tennessee around 2030. Oklo and other startups court partnerships with hyperscalers and even chipmakers like NVIDIA. Recent investor sentiment on X frames some of these firms as “AI power stocks.”

Challenges remain substantial. Regulatory approvals move slowly in many markets. Supply chains for specialized components lag. Public opposition lingers near proposed sites. One Meta plan for a nuclear-powered facility in Pennsylvania ran into trouble over protected bee habitats. Such environmental hurdles highlight the trade-offs. France offers a different model. Its heavy reliance on nuclear already provides stable low-carbon power. Data center operator Data4 signed a 12-year contract with state-owned EDF for direct access to reactor output at production-linked pricing. The arrangement shields against wholesale market swings.

In the United States the picture mixes revival and extension. The Palisades plant in Michigan restarted operations last year after regulatory clearance. NextEra Energy eyes similar restarts. These efforts buy time while new builds advance. By one analysis nuclear could supply around 10 percent of AI-related power demand in the U.S. over time. Kate Hardin, executive director of Deloitte’s Research Center for Energy and Industrials, put it plainly. “We see nuclear over time – not tomorrow, but over time – helping to meet this window that we’re trying to close.”

The International Energy Agency updated its outlook in April 2026. Electricity demand from data centers jumped 17 percent in 2025. AI-focused facilities grew even faster. Capital spending by five large technology companies exceeded $400 billion that year. It is set to rise another 75 percent in 2026. Renewables and nuclear together are forecast to provide nearly 60 percent of data center electricity by 2030. That share stood at 35 percent recently. Natural gas still dominates in the interim. Coal use may decline in absolute terms later as cleaner options scale.

Regional disparities add complexity. Ireland’s data centers already consumed 17 percent of national electricity in 2022. The share could reach 32 percent by 2026 with continued AI penetration. The U.S. saw data centers account for more than 4 percent of total electricity in 2023. Some forecasts place that between 6.7 and 12 percent by 2028. Peak demand growth could add the equivalent of 15 New York Cities to the grid by 2030. Utilities report bidding wars for sites with available power. Bruce Flatt, CEO of Brookfield Asset Management, voiced a common concern among infrastructure investors. “I’m worried about data center demand, that’s why baseload nuclear is super super important.”

Yet the story contains another thread. AI is not only an energy consumer. It is becoming an energy maker. The technology helps optimize grid operations, improve renewable forecasting, and accelerate design of better batteries and reactors. Some analysts argue that efficiency improvements in chips and algorithms could temper the worst projections. Historical patterns show computing efficiency has doubled roughly every two years. Whether that pace holds against exponential model growth is the open bet.

Executives at the hyperscalers emphasize prioritization. Bobby Hollis, vice president of energy at Microsoft, said the company puts “energy and power first” when siting new facilities. Capital expenditure plans from Microsoft, Alphabet, Amazon and Meta exceeded $300 billion in 2025 as they race to secure capacity. Clustering data centers near power sources or building onsite generation has gained favor. A few forward-looking proposals even explore orbital data centers powered by constant solar flux. SpaceX, Google and Blue Origin concepts remain early stage. Technical and cost barriers are formidable. They underscore how far the industry will go to chase reliable supply.

By 2035 global electricity demand could rise more than 10,000 terawatt-hours. That matches current consumption across all advanced economies. Data centers and AI will claim a meaningful slice. In the U.S. AI-driven processing alone may exceed the combined electricity use of aluminum, steel, cement and chemical industries by decade’s end. The numbers sound abstract until viewed against real infrastructure limits. Transmission lines, transformer availability and permitting backlogs constrain expansion. Nuclear projects that once seemed uneconomic now attract serious capital.

The Financial Times first highlighted many of these tensions in its reporting on AI infrastructure. Subsequent coverage across outlets has refined the picture with fresh data. A Reuters examination last December detailed the battle to secure supply. It noted SMR developers will likely miss the most immediate demand surge. TerraPower, backed by Bill Gates, collaborates with Sabey Data Centers on potential deployments in the Rockies and Texas. Momentum builds even if timelines stretch.

So the industry finds itself in a race against its own success. AI adoption accelerates. Power hunger follows. Utilities, regulators and technologists scramble for answers that balance reliability, cost and emissions. Nuclear stands as one pillar. Renewables, storage, demand flexibility and efficiency gains supply the others. No single solution carries the full load. But without urgent progress on all fronts, growth ambitions could hit a hard ceiling. The coming years will test whether innovation in energy can match the pace set by innovation in intelligence.