The Financial Times recently examined how artificial intelligence systems are reshaping the insurance industry, with companies deploying advanced models to process claims, detect fraud, and adjust policies at speeds previously unimaginable. This shift brings both efficiency gains and fresh questions about fairness, data privacy, and the future role of human underwriters. Insurers that once relied on teams of adjusters poring over paper forms now feed thousands of documents into neural networks trained to spot patterns invisible to the human eye.

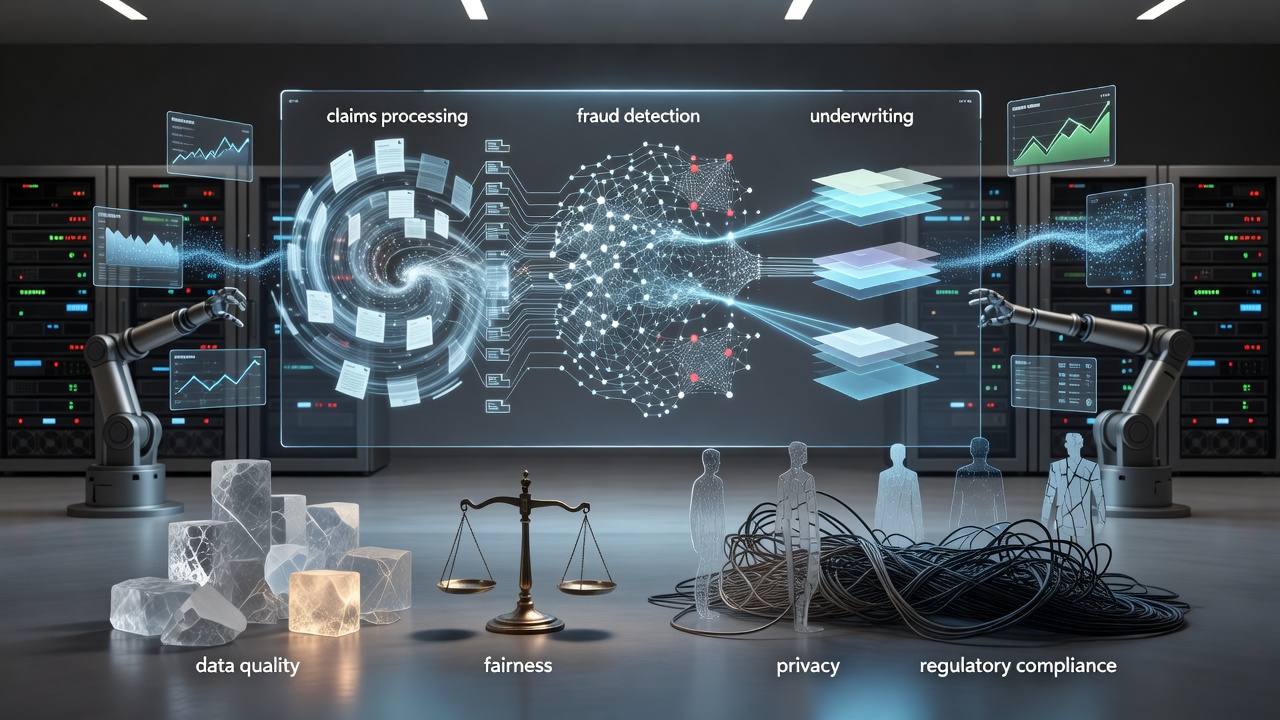

Traditional claims handling involved multiple steps of verification, manual data entry, and sequential approvals. An average auto accident claim could take weeks to settle, while complex property damage cases stretched into months. Insurers maintained large staffs specifically for these tasks, with each employee handling a limited number of files per day. The arrival of machine learning changed that equation dramatically. Algorithms now extract information from police reports, medical records, repair estimates, and even social media posts within seconds. According to the Financial Times article, several major carriers report processing simple claims in under thirty seconds when all required documentation appears in digital format.

Fraud detection represents one of the clearest areas of progress. Insurance fraud costs the industry tens of billions annually across markets. Human investigators previously depended on experience and intuition to flag suspicious patterns, such as multiple claims from the same address or suspiciously timed policy changes. Modern systems analyze thousands of variables simultaneously. They cross-reference claimant histories against public records, weather data, traffic camera footage, and even the linguistic patterns in submitted statements. When a model assigns a high probability score to potential deception, human specialists review the case with enriched context rather than starting from scratch.

This approach does not eliminate human involvement but redirects it toward higher-value activities. Adjusters spend less time on routine verification and more time negotiating settlements, visiting accident scenes, or consulting with policyholders facing unusual circumstances. The technology handles volume while people manage nuance. Yet this division of labor creates new demands. Staff members must learn to interpret AI recommendations, challenge model outputs when they appear flawed, and explain decisions to customers who want to understand why their claim received a particular assessment.

Data quality determines how well these systems perform. Insurers with decades of digitized records hold distinct advantages over newer market entrants. Historical claims files provide the training material that teaches models what normal behavior looks like and what deviations warrant attention. However, older records often contain inconsistencies, incomplete fields, or outdated terminology. Cleaning and standardizing this information requires substantial investment before algorithms can draw reliable conclusions. Companies that cut corners on data preparation frequently discover their models produce biased or inconsistent results that create regulatory headaches.

Regulatory bodies have taken notice of these developments. Insurance commissioners in multiple jurisdictions now require transparency around automated decision systems. They want to know which factors influence claim approvals and whether protected characteristics indirectly affect outcomes through proxy variables. European regulators under the GDPR framework emphasize the right to explanation, meaning customers can request meaningful information about how an algorithm reached its conclusion. Meeting these standards forces insurers to maintain detailed documentation of model architecture, training data sources, and performance metrics across different demographic segments.

Privacy considerations add another layer of complexity. To improve accuracy, some systems incorporate external data sources ranging from credit reports to satellite imagery of damaged properties. Each additional data stream increases both the power of the model and the risk of unintended data exposure. Customers increasingly question whether their driving habits, social connections, or online behavior should influence something as fundamental as insurance pricing. Insurers must balance competitive pressure to adopt sophisticated analytics against the need to maintain public trust.

Several carriers have adopted a hybrid model that combines rule-based systems with machine learning. Fixed rules handle straightforward compliance requirements while neural networks tackle pattern recognition in unstructured data. This combination allows companies to maintain regulatory guardrails while still benefiting from the flexibility of learned models. When the neural network suggests an unusual outcome, the rule system can trigger additional human review automatically. The approach reduces the black box problem that worries both executives and oversight agencies.

Customer experience has improved in measurable ways. Mobile applications now let policyholders submit photos of vehicle damage that algorithms assess immediately. Preliminary estimates appear on screen within moments, giving drivers clear expectations about repair costs and timelines. Chatbots handle initial intake questions, routing complicated cases to live agents equipped with AI-generated summaries of relevant policy details and comparable claims. These tools do not replace personal interaction during stressful events, but they reduce friction in the administrative portions of the claims process.

Underwriting departments have also transformed. Rather than depending solely on applicant questionnaires, companies now supplement information with third-party data and predictive models. A life insurance applicant might receive questions tailored to risk factors identified through analysis of similar profiles. Property insurers can assess flood risk using hyperlocal weather patterns and elevation data far more precisely than broad postal code averages allowed. The result is more individualized pricing that better matches actual exposure, though it raises concerns about whether certain groups face systematically higher premiums due to correlations in the training data.

The competitive dynamics of the industry are shifting as well. Technology-focused startups challenge established players by building entirely digital operations from the ground up. These newcomers avoid the legacy data problems that slow down larger firms, yet they lack the volume of historical claims needed to train sophisticated models. Traditional insurers respond by creating internal innovation units or acquiring promising technology companies. The Financial Times noted that acquisition activity in insurance technology has accelerated, with larger carriers seeking both talent and intellectual property that can accelerate their digital transformation.

Implementation challenges remain significant. Many insurance companies operate on decades-old core systems that resist integration with modern analytics platforms. Replacing these mainframes involves massive capital expenditure and operational risk. Some organizations choose to build translation layers that extract data from legacy databases and feed it into cloud-based AI services. While this strategy allows quicker deployment, it can introduce latency and additional points of failure. The most successful adopters appear to combine strong technology leadership with realistic assessment of their existing infrastructure constraints.

Talent shortages compound these technical hurdles. Data scientists who understand both machine learning and insurance principles command premium compensation. Universities have expanded relevant programs, but the supply of qualified candidates lags behind demand. Companies address this gap through partnerships with academic institutions, internal training initiatives, and creative recruiting that looks beyond traditional insurance backgrounds. A former physicist or computational biologist might bring fresh perspectives to problems that career insurance professionals view through a narrower lens.

Ethical questions surface regularly as these systems mature. If an algorithm consistently denies claims from certain neighborhoods, does that reflect genuine risk differences or embedded societal biases in the training data? How should companies handle situations where model confidence is low but human expertise is also limited? What responsibility does an insurer bear when an automated system makes a serious error that affects a policyholder’s financial security? Industry associations have begun developing voluntary standards for responsible AI use, but regulatory frameworks vary widely across regions.

Looking forward, the integration of artificial intelligence into insurance appears likely to deepen rather than plateau. Generative models may soon draft policy language tailored to individual circumstances or create customized risk management recommendations based on a company’s operational profile. Computer vision systems will analyze drone footage of storm damage with increasing precision. Natural language processing tools will extract insights from medical literature to inform life and health underwriting decisions. Each advance carries potential benefits for consumers through faster service and more accurate pricing, alongside risks that require ongoing attention from both industry participants and public oversight bodies.

The human element persists even as technology advances. Insurance fundamentally involves trust between policyholder and provider. When accidents occur or disasters strike, people want more than an algorithm’s output. They seek empathy, clear communication, and confidence that their claim receives fair consideration. Companies that view AI as a tool to enhance rather than replace these qualities position themselves best for long-term success. Those who focus exclusively on cost reduction through automation may find that efficiency gains come at the expense of customer loyalty and regulatory goodwill.

The transformation underway reflects broader patterns across multiple sectors where artificial intelligence augments professional judgment rather than rendering it obsolete. Insurance occupies a particularly interesting position because its products deal directly with financial protection during vulnerable moments. How the industry balances technological capability with human accountability will influence not only its own future but also public perception of automated decision-making in other important areas of life. The coming years will reveal which organizations manage this balance most effectively while delivering genuine value to the people they serve.