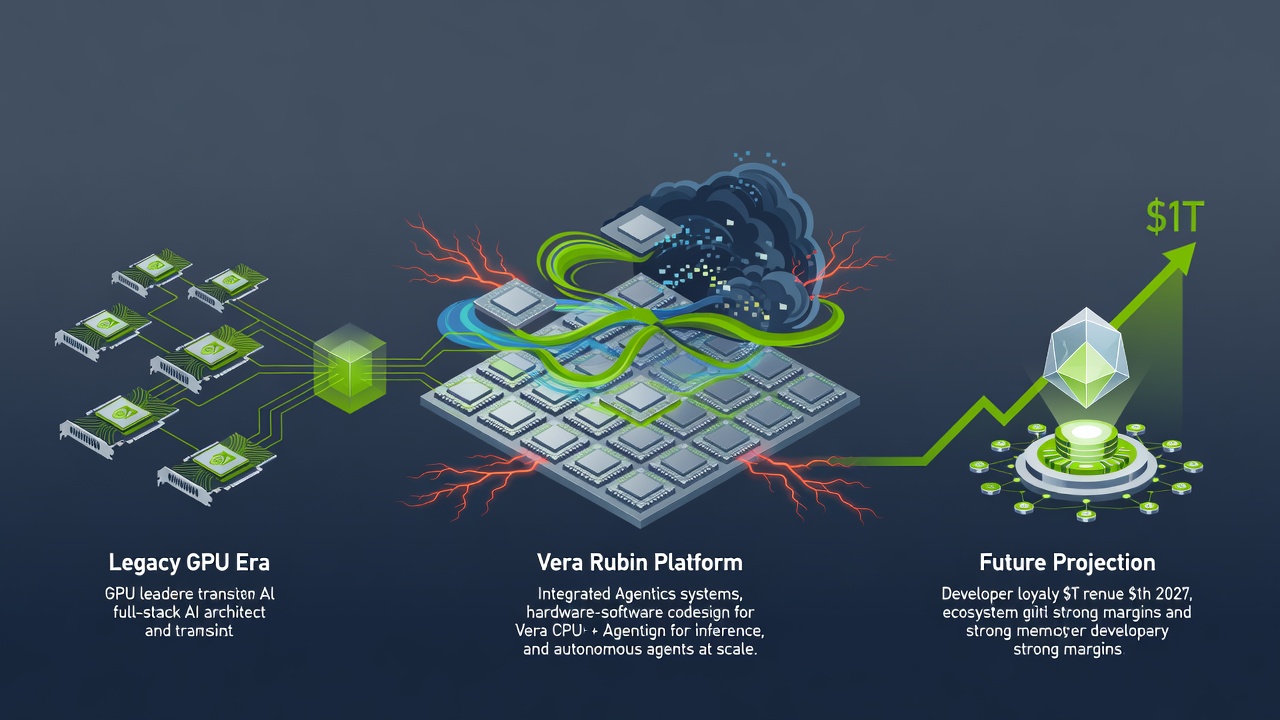

Nvidia stands at the center of the artificial intelligence buildout. Its latest moves signal a shift from dominant GPU supplier to architect of complete computing systems. The company no longer sells isolated accelerators. It delivers integrated platforms that span silicon, networking, storage, software and even simulation tools for entire data center complexes.

At GTC 2026 in March, CEO Jensen Huang unveiled the Vera Rubin platform. This full-stack system includes seven chips, five rack-scale configurations and one supercomputer. It targets the emerging demands of agentic AI. Systems that plan, reason and act across multiple steps. “When we think Vera Rubin, we think the entire system, vertically integrated, complete with software, extended end to end, optimized as one giant system,” Huang said, according to Nvidia’s official blog.

The platform builds directly on Blackwell. Yet it pivots toward inference and autonomous agents rather than pure training. Early claims point to up to 10 times lower token costs compared with prior generations. And a fourfold reduction in GPUs needed to train mixture-of-experts models. Such gains come from tight codesign across hardware layers and the CUDA software foundation that developers refuse to abandon.

Power, Memory and Supply Constraints Test the Stack

But the infrastructure picture isn’t all smooth acceleration. U.S. data center electricity demand could surge from 167 terawatt-hours to 376 TWh by 2030. Power infrastructure now represents a serious limit. High-bandwidth memory supply adds another choke point. SK Hynix’s recent $28 billion Nasdaq IPO and reports of production adjustments for Rubin underline how HBM, not just GPUs, dictates deployment speed.

Seeking Alpha contributor Yiannis Zourmpanos captured the tension in a July 18 analysis. “Although custom silicon adoption is accelerating, overwhelming AI demand, strong profitability, and nearly 50% consensus upside continue supporting the long-term thesis,” he wrote in Seeking Alpha. Nvidia trades near 23 times forward earnings. Analysts model fiscal 2027 revenue at $393 billion and fiscal 2028 near $559 billion. Those numbers assume the company keeps extending its advantage.

Challenges exist. Qualcomm’s $3.9 billion acquisition of a modular chip designer and OpenAI’s reported Jalapeño project hint at future pressure on the CUDA moat. Yet switching costs remain high. Developers have spent years optimizing for Nvidia’s libraries and compilers. A rival stack must match not only performance but an entire toolchain. So far, none has.

Huang himself projected at least $1 trillion in revenue between 2025 and 2027. “I now see at least $1 trillion in revenue from 2025 through 2027,” he stated at GTC, per the company’s recap. The forecast reflects explosive growth in inference workloads. Enterprises move beyond experimentation. They deploy agents that handle complex tasks at scale.

And the stack keeps expanding. The Vera CPU enters the market as a purpose-built processor for agentic workloads. It pairs with the new BlueField-4 STX storage architecture. Broad industry support for the latter suggests customers want coherent, high-performance data pipelines that don’t bottleneck GPU compute. Meta signed a major deal to deploy millions of Nvidia chips, including standalone CPUs and Vera Rubin rack systems. The agreement marks the first large-scale use of Grace CPUs independent of GPUs, according to a February report from CNBC.

Networking receives equal attention. New Kyber interconnects and Spectrum optical switches target both scale-up and scale-out. These elements matter because agentic systems generate massive context windows and frequent inter-chip communication. Traditional architectures falter here. Nvidia’s integrated designs aim to keep latency low and throughput high.

Even physical simulation enters the picture. The DSX AI Factory reference design and Omniverse DSX Blueprint let operators model entire facilities in software before breaking ground. DSX Air takes the concept further by simulating power, cooling and layout tradeoffs. Companies avoid expensive mistakes. They optimize for real-world constraints such as electricity availability and heat dissipation.

Look beyond the data center. Nvidia previewed the Vera Rubin Space Module for orbital computing. The concept targets geospatial intelligence, autonomous satellites and future space-based data centers. Performance claims suggest 25 times more AI compute for space-based inference versus earlier generations. Ambitious. Yet consistent with Huang’s long-term view that computation must expand everywhere demand exists.

Forbes columnist Tim Bajarin traced the strategy’s roots to a meeting roughly 15 years ago. Back then Huang spoke of “owning the stack.” He meant controlling hardware, infrastructure, software and applications rather than depending on partners at every layer. “Today, it has become a central principle across industries and within the investment community,” Bajarin observed in a July 10 piece for Forbes.

This cycle differs from previous technology waves. Advances occur simultaneously across energy, silicon, networking, models and applications. Value doesn’t concentrate in one spot. It spreads. Hyperscalers, enterprises, robotics firms and even national governments build on Nvidia’s foundation. Japan, for instance, collaborates on physical AI using Isaac, Metropolis and Jetson platforms. Partnerships accelerate adoption but also tighten Nvidia’s position at the center.

Software layers reinforce the hardware. NemoClaw provides policy enforcement, network guardrails and privacy controls for enterprise agents. OpenClaw offers an open-source base for personal agents. Nemotron models supply open-weight foundations that labs customize. The combination creates stickiness. Once an organization trains agents on these tools, migration costs rise sharply.

Competitors notice. SambaNova raised $1 billion at an $11 billion valuation to push custom inference chips and full systems. CoreWeave, backed by a $2 billion Nvidia investment, deploys Vera Rubin systems and boasts a massive backlog. Yet these players often complement rather than replace the dominant stack. They expand capacity. They don’t yet displace CUDA’s developer mindshare.

Recent X discussions highlight the shift toward ownership. One thread described a desktop workstation with eight Blackwell GPUs, 768 GB of GDDR7 memory and InfiniBand connectivity. The machine runs large models locally. No cloud queues. No per-token fees. Enterprises ponder how much infrastructure they want to control outright versus rent indefinitely.

Power remains the wildcard. Data centers already strain grids. New facilities require gigawatts. Utilities scramble. Governments weigh export controls on critical minerals and components. These factors could slow deployment timelines even as Nvidia ships product.

Still, demand appears insatiable. Cloud providers including AWS, Google Cloud, Microsoft and Oracle committed to early Vera Rubin instances. Production ramped quickly after initial announcements. Hyperscalers integrate the systems into their offerings. Enterprises gain access without building everything themselves.

Nvidia’s gross margins stay elevated. Free cash flow hit nearly $97 billion in a recent fiscal period. The balance sheet supports heavy R&D and strategic investments. Next on the roadmap sits the Feynman architecture. It will introduce the Rosa CPU, LP40 language processing unit and BlueField-5. Details remain limited. The preview alone signals confidence in multi-year leadership.

Industry insiders watch three metrics closely. First, real-world token economics on agentic workloads. Second, adoption speed of the Vera CPU outside traditional GPU clusters. Third, whether power and memory bottlenecks ease or intensify. Resolution of these questions will shape valuations across the entire supply chain.

For now Nvidia maintains its edge. The stack evolves faster than rivals can copy it. Codesign across every layer produces compounding returns. Developers stay loyal. Customers buy bigger systems. And the company positions itself to capture revenue at multiple points in the value chain.

That doesn’t eliminate risk. Custom silicon gains traction in specific cases. Energy constraints could cap growth. Yet the combination of technical momentum, financial strength and ecosystem lock-in suggests the current trajectory holds. Nvidia isn’t merely riding the AI wave. It’s shaping the infrastructure on which the next phase depends.